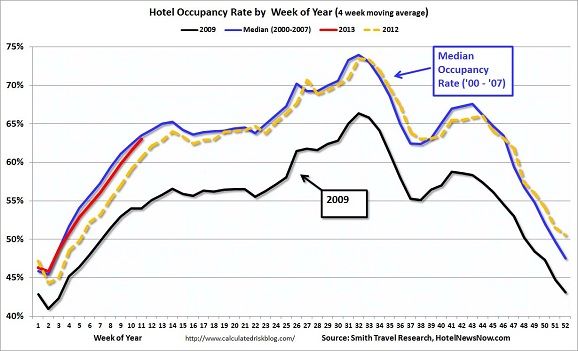

Here’s a chart from the Calculated Risk blog that shows the 2000-2007 average hotel occupancy rates by week in blue.

Then the yellow dashed line shows what those occupancy rates were in 2012. Back to normal levels! The red line shows things so far in 2013, even better than 2012.

So hotels are running full, a sharp contrast from the black line which illustrates the bottom falling out of hotel occupancy in 2009 during the Great Recession.

Nationwide occupancy is up year-over-year by 1.4% to 66.6% and average daily room rates up 4.5% to $112.05.

Put simply, hotel chains believe they don’t have to offer big rebates (nearly as valuable points) in order to put heads in beds.

This is why I am pretty much abandoning any hotel loyalty programs going forward(currently Hyatt Diamond / Hilton Gold). More often than not, independent hotels and smaller chains offer a superior property to major hotel chains. My stay pattern will radically change in 2013. For me, the tipping point has been reached where the “stay experience” is worth more than devalued loyalty points.

The sentiment that hotel loyalty programs do not need to offer big rebates was evident in seminars at the 2013 Americas Lodging Investment Summit in Los Angeles in January.

Several of the hotel executives for major chains were discussing how hotel loyalty programs are looking to move beyond points to improve loyalty and customer satisfaction.

That is a move that benefits the high value frequent guest with hotel stay amenities and special services, but may leave the leisure traveler high and dry when it gets more difficult to earn sufficient points for free hotel nights.

Brilliant – thank you for sharing. What’s your view on Hyatt’s generous award chart then? Do you think we should expect an eventual devaluation there anytime soon?

22,000 points for an award night at category 6 Hyatts seems like too good to be true, especially given that it is relatively easy to earn Hyatt points via their credit card/Chase points, compared with other chains with more inflated award charts…

This is a great planning tool for a leisure traveler who has the flexibility to move dates around……..very useful for that trick………near retirees on aspirational trips take note!

IMHO – I think management teams are finally looking to reap the rewards of their efforts in building up these loyalty franchises. Its time to monetize them! The time (as you say in your post) has finally arrived with occupancy and revPAR looking good. Its interesting there were so many devaluations at the same time – and I don’t have any basis for pointing to collusion… As long as they all do it over time, not one looks better than the other and each brand’s piece of total loyalty dollar pie remains relatively the same… Collectors of loyalty currency are mad (there is a parallel to the plight of Cypriots here), but their loyalty points are the liability of those that issue them and since there is no hard backing to those points, the issuers of loyalty currencies can do what they please (as with any fiat currency)…

I wouldn’t really consider this a tool since it doesn’t show the whole picture. This just shows nationwide occupancy trends but doesn’t take into account the demand patterns which make up individual markets. I’m willing to bet that the if we put an Average Daily Rate chart up against the chart above, we would find that the high occupancy summer weeks are among the lowest rated ADR weeks because the overwhelming majority of guests are leisure driven and more rate-sensitive. Certainly, there will be seasonal beach markets where the ADR will be at its highest, but for the most part, the high ADR weeks are driven by the business traveler who is not as sensitive to higher rates. About the only consistent truth is that December is typically the slowest month among hotels as businesses don’t send as many people out and leisure travelers are tending to stay with family and friends.

To Points Surfer…regarding Hyatt, the thing is from pure earning from hotel stays they aren’t really any better than the other chains. The issue for them is that Ultimate Rewards doesn’t differentiate between inflated point values and sensible point values which affects them since one ultimate reward point is one Hyatt point or one Hilton point even though the former is worth a lot more than the latter.

I couldn’t find Gary’s chart showing earn rates and $ required to spend at a hotel to get the basic vs the highest redemption so I made my own.

Numbers for each chain in order are: points earned on $1K in spend, $ spend to get one night in lowest level room, $ spend to get one night in highest level room.

Carlson: 20,000, $450, $2,500

Hilton: 15,000, $333, $6,333

Hyatt: 5,000, $1,000, $4,400

IHG: 10,000, $1,000, $5,000

Marriott: 10,000, $750, $4,500

Starwood: 2,000, $1,500, $17,500

So Hyatt really falls somewhere right in the middle in terms of earning from their own hotels. Their own credit card reflects this as you earn 1 point per $ spent everywhere vs 5 for Carlson and 3 for Hilton. Starwood is actually the worst chain but I guess their points + cash options are good. Hilton’s most expensive spend required used to be $3,333 now it’s $6,333. Makes sense as to why they raised it when you look at that, but a bit more gradual would have been appreciated.

If Hyatt finds that a significant percentage of points in circulation are coming from UR transfers, then the fair solution would be to simply double both its own earn rate and its own redemption rate to put it on level field with the other UR hotel partners. To only raise the redemption rates would be awful

Also you would think that if Hyatt ever did that to be fair they would need to not only raise the earn and burn rates but to multiply member’s current point levels by the same multiple. For example member John Doe has 500,000 points in his Hyatt account. Hyatt increases its earn rate to 10 points per dollar spent, its redemption rates all double so the top category is 44,000 points and John’s points balance increases to 1,000,000 points. John is no worse off than he was before such change. However Chase members are as now all of the sudden 1 UR point goes half as far as it did before.

I really hope they don’t make such a change but at least if they were to do so, doing as I described would be the fair way to do it. Hopefully that day doesn’t come. The downside to them is that they probably wouldn’t sell as many points to Chase which does net them cash. If at the end of the day rooms are being used for point redemptions when there remained excess capacity, then they really aren’t all that worse off.

If you are a business traveler, it is OK to remain loyal to either SPG or Hyatt. Hilton is still OK even with the new devaluation.

On vacations, my main goal is the destination, not the hotel. Any good 4* hotel will do just fine. And, I prefer to eat all my meals in local restaurants.

@ Jeremy

Thank you for your input. You raise reasonable points. I suppose I am still a bit shaken from the Hilton devaluation since I was in the process of building up my balance for a high-end redemption in the Maldives but I don’t yet have enough points to book before the devaluation kicks in and they weren’t nice enough to double my current balance 😉

Hilton’s situation is fairly different from Hyatt’s though as you points out above. Also I do agree that the method you suggested for Hyatt above is the fair way to do it, but I suppose if they went that route they would have to do it suddenly and unannounced, otherwise I suspect there would be a flood of UR to Hyatt transfers ahead of implementation just to get in on the doubling of points balances.

Bring back the Great Recession! We may not have had any money, but all our travel was free!

I think hotel points at the new airline miles. Most of the hotels have made the points and status harder to get or keep like airlines did a few years back. Now many are moving to hotel credit card offers to get status or earn big bonus nights.

Airlines on the other hand are becoming even more of a hard market but a few good deals still around.

I also think that technology is catching up with us. As the systems get better there will be less hacking however the shopping partnership rebates should improve in accuracy (I hope).

@Gary, The only thing this chart shows is that occupancy rates are at the same levels as back before the great recession yet they were providing awards at lower levels back then.

It would be more helpful to show where the average daily room rate sits in the same light. If you have occupancy rates at 2007 levels but with prices 20% higher, then people would be able to follow why points have been devalued.

The other factor that would be good to include is the points supply (total # of points within a given program). If you had a chart showing these points within HHonors, Marriott, Hyatt, SPG etc. over time, I think we would be able to better understand the points devaluation.

We see occupancy rates at similar levels to 2007 and my guess is that average daily room rates probably are not significantly different from 2007 and definitely not to the extent to which programs have devalued their points. Thus, that leads us to the points supply which is probably significantly higher than in 2007 and this may be the real reason why programs have been devaluing their points.

This graph pretty much matches hotel prices for the most popular US cities over the year. 45% equals about $130. Its also indicates why you don’t want to be redeeming points mid October to April unless you’re getting a significant break.

Thanks for sharing, interesting data!

The silliest thing I see when people complain about “devaluation” is when they fail to first adjust for paid rate inflation and the cost of point acquisition. If paid rates increase 25% from one period to another, and the points required increase 20%, you’re ahead. Similarly, if promotions and earning opportunities are more scarce and it becomes 20% more expensive to acquire you points, but paid rates have increased 25% during the same period, you’re also ahead (ceteris paribus).

Interesting note of this chart is the “windows” of opportunity that the chart shows in good weather months of April-May and September………for an aspirational trip those are key facts and the paid rates are going to reflect the drop from the busy summer months………..so from that sense it is a great “tool”……..and I will use accordingly……..

Hotel loyalty programs at this point are 100% only for the business customer.

If you’re paying for your own hotel the only thing you should be loyal to is priceline.