Matt at Saverocity penned an important post about whether or not a $1700 3-cabin first class roundtrip between Boston and Seoul is even a good deal.

He points out that my tweet included #ScreaminDeal #Hurry and wrote,

How about Hashtag #Bollocks #to #you?

The deal, that is, not the tweeter, he is just sharing what his readers want.

Let’s explore this, with a scenario. It assumes that you actually get off the plane, stay say 3 nights, and get out of your hotel room… of course you might just want to fly there and back which is just magical, and I wish you good speed….

And he goes on to posit that you’re going to spend ~ $2400 per person on the trip. That’s still a lot of money, and there are other things you can do with that money.

Matt’s post brings up for me something I’ve learned about the frequent flyer community over time, and that’s that it isn’t really one community, or rather one group of people all with the same set of goals.

There are people who like travel, people who like math games, and people who just like planes. Aviation junkies and travel nuts aren’t the same. Some people want to live as cheaply as possible and that’s why they chase a deal, and others want to get as many experiences as possible and deals let them do that in relative comfort.

That and that decision-making happens at the margin.

If you’re at a margin where $1700 x 2 tickets or a given getaway is the difference between funding an IRA and not, then it’s probably wise to scrap the discretionary trip and set aside money for retirement.

But if you’re already funding your retirement, and one of the things you do spend money on is travel, where you go may be influenced by where you can get the best deal. Should I go to Seoul next, if I haven’t been, or to Buenos Aires? Relative prices matter, whether you can do a long trip quickly because of the relative comfort matters (preferences, age factor here).

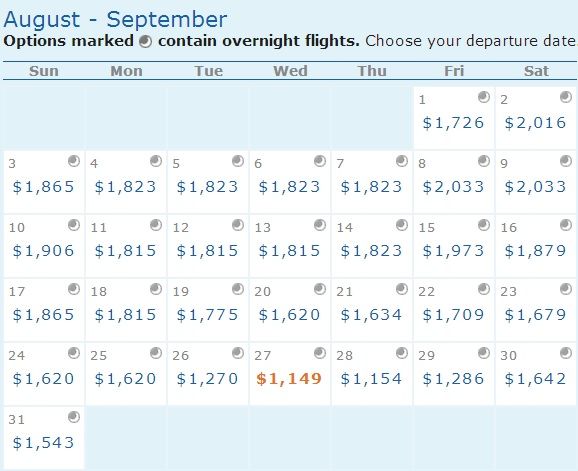

A quick search on ITA for BOS-ICN roundtrip in economy, 2-6 nights with a departure any time in August, shows lowest price trips ranging $1149 – $2033 depending on day you leave and length of trip.

The Seoul fare is not even close to FREE TRAVEL. But it compares well with the regular price for coach.

So let me say — unequivocably — from where I’m coming from, this was an absolutely fantastic deal.

If you’re going to take a trip outside the U.S., the fare meant a chance to do it in first class for about the price of coach.

And since it earns a 150% class of service bonus (ean 2.5x flown miles) you’re picking up about an extra 24,000 redeemable miles to boot. Plus the tickets are refundable. So it may be a better financial deal than buying coach, even aside from the inflight comfort (which is something I’ll pay a premium for).

That’s the sort of calculus you’re going to do, or should do — how does this stack up against what you would otherwise be doing? Again, at what margin? Factor in incremental price, tradeoffs, preferences.

Peoples’ tradeoffs are different, their goals and preferences are different. Where Matt — who challenges the idea that a $1700 first class fare (base fare that’s about 90% off the ‘regular’ price) is a good deal — is at, and where many people are in the community.. it doesn’t work for them. And it shouldn’t.

That’s also why there’s a good diversity of blogs, different people writing about similar subject matter from a different perspective.

You find the sites that speak best to you and your interests, or that challenge your thinking, and read those. And there’s enough diversity of voices to do that most of the time.

We often hear outrage! Outrage! At the opinions or advice of others. How could they say that?! Don’t they just realize that…

Not everyone you disagree with is evil or stupid of course, your position may be perfectly logical for maximizing what you value most .. you may be engaging in transcendent criticism where you differ on values, rather than immanent criticism where do differ on how to maximize the same values.

So yes — I think $1700 first class roundtrip US – Seoul is a fantastic deal. But it isn’t something that everyone should do. Given.

- You can join the 40,000+ people who see these deals and analysis every day — sign up to receive posts by email (just one e-mail per day) or subscribe to the RSS feed. It’s free. You can also follow me on Twitter for the latest deals. Don’t miss out!

You know we’re headed toward a worse recession when a $1750.00 Business Class fare, RT, from BOS-ICN is debated.

Now, if there was no such thing as “Internet streaming videos”, the YouTube founders and Google CEOs/Chairman were put in Gitmo, and it was all DVDs, LDs, Videos, hardware, cellphones, blogs, etc. which would cause much less Frequent Flier/Hotel point devaluation and an even less Obama wealth distribution (without his crappy ObamaCare) the fare would sellout in less than 6 hours.

My opinion, and I’m correct. Because the only thing out of South Korea now is Samsung with Google/NSA’s Android, and Samsung really does suck. What other reason is there to go to South Korea, except to transfer at ICN (IMHO). Thanks.

ED

It is an AMAZING deal!!! Wishec I could have gotten it before it went away.

There’s also the fact that if you live far from Boston you have to get there which is going to be a few hundred dollars. Then there’s always the question of opportunity cost. If you’re someone like me who doesn’t get vacation time and ~60% of your income does not come from hourly wage, that could be significant.

For a trip like this, if you live in SFO, and the trip is from BOS-SFO-Seoul, then could you just board from SFO & miss the BOS-SFO segment? Was this flight cheaper if you just went SFO-Seoul?

Otherwise it’s stupid to fly from SFO-BOS-SFO-Seoul…

I think this was a great deal. But I think the point Matt is trying to make is that just because it is a great deal doesn’t mean you should buy it. It all depends on you, what you are looking for, your circumstances, etc. And you thoughtfully pointed that out. I’m glad different points of views get brought up and also that we can address them in positive ways. Nice job Gary.

@Emily no you had to originate in Boston, could not skip a leg. And Starting in San Francisco would be several times more expensive.

For a trip like this, if you live in SFO, and the trip is from BOS-SFO-Seoul, then could you just board from SFO & miss the BOS-SFO segment? Was this flight cheaper if you just went SFO-Seoul?

Otherwise it’s a waste of time/ money to fly from SFO-BOS-SFO-Seoul…

Gary,

Thank you for the deal! I have purchased one and have second one on hold. This deal is great! Leave these unhappy, confused fellas alone! Your blog is something that I always read enjoying about super deals, food and opinion daily!

oops I dont know why it posted another one. Can you delete the previous comment?

Thanks for the reply, Gary.

Thanks for the friendly retort, I appreciate the perspective. For those who think I’m weird for promoting financial independence over following the crowd, just think what this blog could be if Gary didn’t have to push credit cards every few posts- and it was all just commentary.

That’s financial independence!

Gary,

That was a fantastic deal and while I couldn’t take advantage of it this time since it wasn’t my choice airline, I totally appreciate the heads up.

Don’t sweat the haters. Of course Matt is right, you could fly economy, or one could donate that amount to charity (what’s with all these whiny internet chumps telling me how to spend MY money anyway?) Yeah you could dump the cash into your 401k or a Roth (I can’t do this either as I already have to stop my contributions in October every year to avoid the wrath of exceeding the IRS 17.5k limit since I’m not yet 50).

@ ED — It’s your opinion, and it is babble. Seoul has a lot to offer, and I look forward to returning on this great deal!

Thanks, Gary. I would have missed this one if not for your blog!

Good points. Frankly I think the trip in the nose of UA’s 747 isn’t worth much, plus getting to BOS & then flying to SFO but not on an AA321T. But moot point for me since I’m not supposed to be paying for airfare this year ;-). + Soul isn’t high on MY list. And I will be flying thru ICN on Asiana next month on way back from B-Day trip to HKG using UA pre-deval miles in OZ 1st ICN-JFK. Interesting the HKG-ICN is now on OX’s new A380 but in buz, apparently not doing 1st on 3.5 hr flgt. Okay since I can try buz. Outbound 2 HKG in CX First 🙂

I think it’s a fantastic deal. Would I stop everything to jump on it? NO. Why? Because I can get a better deal than that, by buying miles and using them for premium seats to places I really want to go.

Hey Kevin,

You can do more than $17.5K,and it sounds like you might want to. I’ve written 2 posts this week on how to do that…I would suggest looking up HSAs and Backdoor Roths, they might offer you a solution if your comp is too high.

Of course, you have a point that I shouldn’t tell YOU what to do with YOUR money- but you could also understand that the original post by Gary without balance also encourage spending.

I don’t think I am being a chump for telling people to save more in a country filled with debt and terrible retirement savings, maybe a whiner though 🙂

Oh yeah and what is it with all these internet chumps that through around names online? I’ve yet to meet one in person who does that.

this is a no-brainer. YMMV. anyone in the points/miles game should have a crystal-clear understanding of their means, prerogatives and breaking points. your financial security is only one thing that hinges on it.

Wow. I thought it sounded like a fantastic deal. I don’t think you have to justify yourself to naysayers. Seems to me that there are too few people posting great business class/first class deals. I ultimately chose not to buy this particular deal but this is the kind of post I would like to see more of…

This is an amazing deal! If I wasn’t in the military, I’d snap up these tickets in a heartbeat! Korea is beautiful, and the food culture is simply one of the best in the world!

$1700 for a biz trip from the US to any Asian city is an amazing deal! Anyone thinks it’s not should not play the point game. They just can’t afford it!. Period.

Three easy pairs of “or” criteria for this being a great deal:

1. You actually want to go to Korea or can pick up a cheap ticket from there onward

2. You live within a reasonable drive of Boston or can get there very cheaply

3. You have sufficient vacation/retirement time and/or you just like spending 30+ hours on airplanes drinking like a fish.

If this had been “Chicago to Europe on Oneworld” instead of “Boston to Seoul on Star” I’d have been all over this one. But it’ll cost me $400 to get to/from Boston, I’ve already allocated my vacation time this year to other trips, and I have absolutely no use for United. Easy pass for me.

You’re both right!

If you weren’t planning to go anywhere, it’s not a good deal.

If you’re concerned about making an elite level next year, it’s a great deal for PQMs, but doesn’t “break even” ($0.10 spend/mile) on PQD, so I hope you have some expensive business travel.

If you already wanted/were planning to go to Seoul, it’s a great deal to get a better class of service.

If you were already planning a vacation out of the country, it’s a great deal to start your vacation early.

I was planning to go to PVG sometime in the fall to bolster my PQMs for the year and visit a friend. This deal was a no-brainer for me — I can do ICN in F, spend a few days, and a Y hop to PVG and back for a few more days for less than the GPU-upgradable W fare I was planning to buy. (At this point for me, life’s too short to do a mileage run in Y.)

There are cheaper places to travel, cheaper ways to get there, and cheaper things to do, but I’ve never been to Seoul and it gets my closer to my original destination. It’s making for a very busy travel year for me, though!

It was a good deal if you had to already be there.

Unless you took the 6am flight from BOS you had to overnight in SFO, so add hotel in either SFO or BOS on top of getting to BOS.

Don’t even think of getting off at another city because those tickets would definitely be flagged, so you’re flying to Boston all the way or UA would hit you for the fare difference, so add either 14h in SFO or another night in Boston.

So add 2 nights possibly in a hotel, r/t to Boston.. And 1+ days of extra travel.. It was a great deal if you needed to go to Asia, but wasn’t really worth going out of your way to do it… Plus this is UA F not a partner F, where I would have jumped on it, if it was a partner flight.

http://www.youcaring.com/littlelevi (my dog was hurt in a hit-and-run) please consider helping with your coffee $$.

@Gary, thanks. I just wish this one had been around when I lived in Seoul. I am now temporarily in a remote part of China.

Anyway, many international schools, at least the good ones, pay for a round trip ticket to their home in summer, so yeah, I would totally have jumped on this deal. Every summer I stock up on supplies from home, cram it all into 3 suitcases and unfortunately, have to pay the high baggage fees. Flying FC changes the game plan for teachers. Usually, 70 pounds rather than 50 is allowed, and your baggage costs are included in the FC ticket, meaning that I’d probably still bring another bag or two, saving on even more supplies that I don’t have to buy in Korea. It’s all relative.

I enjoy reading all of the bloggers. All of you have an angle and depending on where I am at in this journey called life, I’ve picked up some great tips.

Oh, and I’m flying back on American Airlines from Shanghai to LAX in a week and a half, and used US Airways miles (cc signup plus buy points plus MS). Its all good! Saved me a ton of money. Thanks everyone.

@Matt, I want to learn more. I’ll see you in your forum.

@Kevin – the $17,500 is a 401(k) contribution limit. You can also contribute $5,500 to a non-deductible traditional IRA each year, regardless of your income. Depending on your circumstances, it might make sense to convert the traditional Ira into a Roth, which you can do regardless of your income. Stop complaining and focus on actually maximizing your savings.

@Bostonwalker, aren’t you really doing the same thing you’re accusing others of here – putting down people who go into this with different motives or strategies than yours? I went to Seoul a year ago, and had a great time, but did it with United points earned with credit card signups and UR transfers. I can afford to play that game, even if I can’t toss out $1,700 cash for a first class ticket, or choose not to despite the fact it’s steeply discounted. Gary knows he has a mix of types of readers, and it’s perfectly suitable for him to cater to different preferences in his choice of blog posts. I’m interested in what can be done with points; you’re interested in discounted cash offerings. I’m sure there will be plenty of things in this blog to help each of us, without a need to criticize each other’s ideas.

One size does not fit all! I for one see this as a deal of the century as I travel to Seoul routinely. The post was nothing more than a heads of availability, totally your decision to pursue. Thanks for the original post!

While Matt at Saverocity is generally a good resource for tricks and tips on frugality in general, I find he usually is preaching one particular view of frugality (his) and is condescending towards others that don’t share his view or (like me) find it even irresponsible in places. For one, he is reliably anti- miles and points collecting, so take his views on travel deals with a grain of salt. Ironically at the same time he rails against miles and points he encourages people to buy other things they can afford even less: houses. He preaches saving money to afford the down payment on a home instead of renting, and doesn’t for a second consider how it might not be responsible to encourage people to take on mortgage debt simply to become homeowners. Miles and points may not be for everyone, just as the chains of a mortgage might not be either.

Hey Chas,

Just to clear something up:

I love points and miles – I haven’t paid for a revenue ticket in years due to them. I just say hoarding them is not smart because you expose yourself to devaluation risk.

As for this mortgage stuff you say.. I have a lot of thoughts on these matters, but I never encourage people to buy a house they cannot afford – that is stupid advice.

I do think people should be saving when renting – whether towards a down payment or otherwise – and yes, I do think that in the long term home ownership offers a path to wealth generation because of the favorable tax treatment of ownership.

And I started a thread just this week proposing that while things like mortgages are generally considered ‘good debt’ we should seek to break these ‘chains of a mortgage’ as soon as we close on it, and pay it off as fast as possible.

The thread is called: How much of your debt is good debt today:

http://saverocity.com/forum/threads/how-much-of-your-debt-is-good-debt-today.343/

@Matt worth thinking through Josh Barro’s take on homeownership as a poor investment (and separately the tax treatment is for the most part already baked into the price of the asset you’re acquiring).

http://www.nytimes.com/2014/05/06/upshot/everyone-wants-to-be-a-homeowner-why-not-a-foodowner.html?_r=0

Megan McArdle has some good thoughts in defense of homeownership in response to Barro here:

http://www.bloombergview.com/articles/2014-05-07/buying-a-home-isn-t-bad-for-you

And I should disclose in this context that I both own and rent — I purchased a home, decided to move, now rent it out rather than selling it. And the place that I’m living in presently is rented. Factors in that decision include that I’m not going to stay in the place very long and overall bet against valuations in the market in which I’m living (not betting against prices per se, just stagnation, not worth the financial obligation for little expected upside). I also don’t need the lock-in effects of a mortgage to force savings.

Hey Gary,

Thanks for the articles, its always nice to see other perspectives.

Personally I view home ownership as forced savings (with a mortgage) – I dislike mortgages, I currently own – until next week when I move out and paid cash. But I view mortgages as a necessary evil for many people who want to own.

So – there is a distinction between home ownership in the rent vs buy world, and mortgage debt.

The tax advantages are key – on the financing side they are solid – real estate tax deductions, mortgage tax deductions etc – but the real good stuff is on the sale side. That is the edge over renting.

Renting short term has lower transaction costs and is certainly wiser – I am renting a summer house for a while, then may rent or buy depending on housing stock and duration at location.

Again though – the bigger picture here is that while there are some people, like yourself who have the financial wherewithal to make a savvy decision to rent,for every one of you there are 100 that see a successful person and say “Gary rents, why would I save for a down payment?”

Then they don’t save anything, and blow it on a 3 cabin F ticket 🙂

From a behavioral economics standpoint, home ownership is a second best that many people should probably do. But that advice doesn’t hold at all times or circumstances, there are costs people don’t factor and people can easily overbuy (just as you suggest people get in trouble modeling others, certainly in the middle of the last decade people were seeing their peers overbuy into homes they couldn’t afford over time). Home ownership reduces mobility. The transaction costs both buying and selling are huge. And during a pricing frenzy it can turn out to be quite the bad investment.

But renting isn’t a bad option for many, you’re paying for housing rather than bundling your housing payment with what works out in many cases to be an inferior investing option.

The trick of course is that you need to save. If you need a mechanism to help lock you into savings, home ownership is one such option.

From a public policy standpoint the home mortgage interest deduction is ludicrous. But it’s pretty well locked in. It also gets baked into price, it’s less obvious than you think that it’s the borrower capturing the benefits. There’s also a ton of money there, at some point I do think we can expect to see tax reform here, it will be hard to dislodge the benefit from those currently using it. But removing it only from new buyers has perverse consequences as well, the sale value of existing housing stock could drop (making that house a less good investment..) and reducing labor mobility. And yet with that much money and that perverse a tax break on the line, policymakers have designed changes that were far more ridiculous…

Your models can’t hold tax policy constant. Same goes for tax-advantaged retirement accounts. When considering a roth vs 401k, the taxes are essentially the same if you hold your tax rate constant. Some people want to pay taxes later on the bet that their income will be lower and so rates lower. But will they be? The long term direction of income tax rates will undoubtedly be up. But does that mean you should bite the tax bullet now? You’re betting that the government will keep its deal and not tax the money upon withdrawal. But do you trust that? It’s a whole lot of money at stake, and we’ll be in a quite poor fiscal situation. I’d defer taxes not because of my bet on my future tax bracket but because I don’t trust paying taxes now won’t mean I get to avoid them later.

In a purely theoretical sense there’s not one right answer, since the answer depends on assumptions that you can’t control.

The important thing of course is to save. If you aren’t doing that you have a problem. If you need a second best option which helps you do that you’re better off than not saving but maybe not better of compared to an alternative you wouldn’t take advantage of.

Key is to understand your situation, be meta-rational enough to understand how you respond to incentives, and act accordingly.

I agree its great for forced savings as you say.

Home ownership has capital risks, whereas renting does not. Renting is guaranteed to cost money because you have no skin in the game and no chance for upside- so by ensuring you have no downside risk on the loss of capital you lose upside.

Closing costs aren’t awful in my opinion. Buying a home is equitable with opening a rental agreement in my experience (can certainly be higher with mortgages and city/state tax priced in. Selling of the home is a bit of a hit, but you could try more modern approaches such as leveraging FSBO.

Tax policy change risk is valid – but my belief is that they won’t seek to estrange the middle class so they will keep most of these breaks.

The section on cap gains is focused more on the housing industry, and sure it may go also – but it isn’t easy to pull $250/500K of cap gains exemption away from people, in fact it would likely be a constitutional battle, and not an easy one to win.

As for you stuff on Retirement accounts -valid, they could change, but again, a huge issue to attempt to face. And most importantly casting doubt on it should not prevent people from funding them.

That is the real issue again – people hear that 401(k) could possibly change, so they can again excuse themselves from saving for it, and why not fly to Korea?

Regarding taxes, I wrote on this fairly recently comparing a tax deferred to a tax free investment, and in truth while most people assume taxes will increase, historically they have not. When reviewing historical data for my post what we saw instead was politicians will use the tax rate to win favor, and they will have no qualms in lowering it.

There is one right answer – it is diversification. The one wrong answer is spending money on unnecessary luxuries when holding debt, or not financially sound.

It sounds like Matt’s priority is financial independence. That’s fine, but it’s not everyone’s gig. It’s high on my list, but I’ve had too many friends die young to put all my eggs in the “future basket.” So, I am one who chooses to balance saving for the future with living life to the fullest, and I recognize the challenges and conflicts.

I’m new to this hobby (the miles/points one), so I’ve been reading a LOT of blogs. There are, as Gary says, all kinds in this game. I’m a “rather have an amazing first class experience once a year” over “three cheap but cool trips to interesting places.” Part of it is a love of luxury, and part of it is trouble taking much time off. But, it takes all kinds, and I respect that.

My sister-in-law and her partner went to the Virgin Islands the same year I did. They spent 2 weeks camping on St. Johns and I spent 4 days at the S.T. Ritz. I probably spent more than they did, but wouldn’t trade places for anything. And, neither would they. We both think the other is nuts–in a kind, loving, respectful way. (If I am camping out, you better be paying ME–a lot.)

Gary clearly didn’t mean everyone who reads his blog should go fly to Seoul in First Class. He meant that anyone who ever thought they’d like to go there, and leaned in the direction of FC flying, should jump at this deal. Those of us to whom this did not apply nodded and moved on; others jumped on it (and I hope a lot of them got it). I appreciate the heads up, even though this particular one wasn’t for me. The next one might be (I read all the tropical island-type posts with great interest, and often bookmark them).

I don’t think anyone is advocating travel of any kind over funding one’s retirement.

Well said.

Hey Mbh,

All my point is that you can travel and live for today on points, and save the money to improve your financial position.

I think everyone should want financial independence, and sure that means some sacrifices – but not ones that you would notice. Just making smarter decisions. I’ll have to sit down one day and count how many countries I have visited and how many crazy things I have done to enjoy the NOW… but it’s a lot.

I’m not saying give up living life, all I am saying is recognize the opportunity, and use miles and points to offload the cost of living in the moment – storing up your cash for better things.

That’s the value of miles and points – taking the burden of cash off the table so you can target that into debt or savings.

Thank you for posting about this fantastic deal Gary. I was able to grab two seats. Keep ’em coming 😉

@Matt writes “I think everyone should want financial independence,” I agree that saving enough (and taking other financially prudent steps) to be in a financial position of strength is desirable. The context of discussions about financial independence often center around “retiring early” or “being able not to work.” I thought I’d simply share that I *want* to work. It’s not about basic necessities but about creating something, building something, doing something that’s valued by others for which others are willing to offer something of value in exchange. Work is not something to be avoided, although of course being in a position of financial strengths limits the sort of risk aversion which might interfere with doing just that.

It’s really simple. If you were financially independent, you could still run every business you like, but you wouldn’t have to follow other peoples rules.

In the case of this blog- you can still run it and build a business and help people, but you wouldn’t have to write those X out of 10 Chase card promoting posts.

The site would still earn money, but you could be free to write non affiliate driven content.

That must be better for you, and your readers?

@Matt: I fail to see how recommending people jump on a great deal for first class tickets in any way violates the priorities you list in your response to my comment. How is what Gary suggested inconsistent with what you believe? Are you just opposed to ever using cash for travel? Do you think people should only travel on points/miles? That’s not really very reasonable, imo.

@Matt you keep taking jabs at me and my content here, and for the purposes of a polite discussion I’m just going to ignore that snark.

Much of the financial independence discussion focuses on retiring early as the goal, and that’s certainly not my goal and it’s a goal I find quite boring. A strong financial position can free you to take entrepreneurial risk, as I noted above. And that does interest me.

But I also don’t think it’s the only thing of value, that you should defer as much consumption as you possibly can until some future time when you have “enough” and are “financially independent.” In fact, responsible consumption as you grow your income can work well from a behavioral standpoint too.

One of the best pieces of advice that I got in my mid-20s came from one of Sir John Templeton’s partners. The advice he gave his own kids was to save half of each raise. You never miss the money, since you were never spending it in the first place. Enjoy life and save at the same time.

That’s not the formula that will work for everyone, but it’s just as myopic to think that spending for enjoyment WHILE you save is a negative either.

Back to your snark about credit cards, since you offered that earlier in the comments as well, I’ll broaden it and talk about earning money off of a business. It’s not just to eat, to gain shelter. As I wrote above, I have a passion for “doing something that’s valued by others for which others are willing to offer something of value in exchange.”

I don’t have to write about credit cards, there’s all sorts of talk and speculation about quotas or other such things, and at least in my personal experience and context it is utter nonsense. I write what interests me and what I want to write about each and every day. And I do it without fear, and I do it genuinely feeling comfortable at the end of each day with what I’ve written (although I’ve gotten hotter under the collar on occasion than I probably should, I’ve aimed more snark at targets I considered deserving but that I ought to think better of because it’s not all that I want to be.. and I try to learn from that).

Gary,

No snark. Pure, honest talk. That’s what we seek in financial independence too.

In the past you have got hot under the collar about ‘name calling and snark’ but this thread had a reader calling me names and you took no action. I’m a big boy, so I don’t mind, but I think it is worth pointing out.

I’m not being snarky here, but it seems to me, and the people I talk with, that you have a ton of great content here, then you throw in a ‘feed the family’ post. That is not intended to be derogatory, it just seems to be the way you post.

You post X number of pure, important, on your mind posts… then you post another Y number of pure affiliate posts – you have said yourself that you have a ratio of these in the past, something like 1 in 8-10 (perhaps it is more in recent days).

Are you honestly telling me, and the crowd here that you aren’t influenced by affiliate revenue? I am sure I heard that you admitted this just recently?

So, rather than bring in nice old stories of Sir John this and that, why not reflect on what it means in reality today, and how it could be different?

There is no shame in making money, all I am talking about here is being honest about it, and deciding if you are happy allowing it to drive your content or not.

@Matt I don’t police comments, I do ask for a certain level of discourse. And when it crosses an (admittedly subjective) line I might do something.. extreme sexual stuff, extreme profanity. But for the most part I ask for and don’t get the level of discourse I wish for. I have no doubt that’s my own fault, and if I knew how to do this better I would.

I’m not saying affiliate revenue doesn’t matter, quite the contrary, if I can write a post that I think it helpful to readers and also benefit from it I think that’s fantastic. I realize that not every reader benefits from every post, and some are very vocal about it, but the posts that tend to be among the most popular are the credit card posts. I write for myself, what interests me, but it is fun when I see readers light up. I feel good about the content of my posts that include referral links because I do my best to make the best offers available that I know of whether there’s a financial interest for me or not and I try to never hide the ball when there’s a personal benefit to me.

Suggesting though that I’m somehow not being honest, and coming back over and over to other content in a post about spending money on travel vs. saving and bringing additional attention to your post that I thought was an important (albeit in my view not fully complete) contribution just rather baffles me, that’s all

Put another way, some people just don’t know how to graciously accept a compliment 🙂

I’ll take it! Not sure where there was a compliment but I’ll certainly take whatever I can get thanks!

For the name calling stuff, I was referring to how you were upset when people talked about ‘pimpin’ in the past with regard to your posts and promoting the virtues of a credit card. You seemed fast to be offended at a word when you are the subject, and made that the focus on conversation rather than the actual subject under discussion.

As for coming back to discuss points, I think that posts open up opportunities for discourse, and I think that there were many aspects in this post that were worth exploring and extrapolating.

I would hope that our conversation has added perspective to one another, and our readers and hasn’t been baffling or perplexing to anyone. We are just sharing views here.

So, thanks very much for the compliment 🙂 It’s been fun chatting!

Gary,You did not purchase any united tickets not because it was good deal but because like Lucky you are permanetly banned from ever flying united ever again.You must have your million miler elite status taken away too.

@banned from united – genuinely no idea where people get ideas like this from. My United MileagePlus account is definitely active, most recent miles posting date June 4, 2014.

@Matt “Not sure where there was a compliment but I’ll certainly take whatever I can get thanks!”

The post begins, “Matt at Saverocity penned an important post..” with a link to yours. I’m recognizing the importance, and sharing my thoughts on what you’re saying, all while introducing readers of this blog to yours.

That may not be obviously a compliment to you.. noted. 🙂

You linked to my site, and I got a boost of about 100 page views…arigato. The post wasn’t complimentary, it was a retort.

I’m a grateful kinda guy, but I see a crop dusting here, which isn’t going to get me jumping up and own.

Cheers 🙂

@Matt sorry, obviously I can’t see your stats, I’m disappointed more readers didn’t click (well, it shows more outbound clicks on my side than that, but still). Probably because I summarized your position. Hopefully fairly.

I didn’t mean to suggest I was giving you some sort of traffic, but I felt like my post was respectful. And disagreement, if done in a fair and respectful way, is I think a substantial compliment. At least that’s how I meant it!

Incidentally, not familiar with the colloquialism ‘crop dusting’ in this context. I sure hope you didn’t mean that the way I found it listed in the urban dictionary!!

Seems to me @Matt is just trying to get some people going to his site rather than yours. Really I think his self-interest is fairly clear here. His message is quite a good one in fact, but not really sure why he has to diss others views to get his over, perhaps he thinks you are getting more traction than he is.

@Gary, I did mean it in the urban dictionary way 🙂 I’m cheeky, and better in person. I hope we will enjoy a pint one day.

@steve I’m not, but there is some truth in what you say. I’d be as happy to chat over on my post or my forum, but rather than reply to my post Gary posted, so I am conversing here.

The truth is I do want more readers, but I don’t want bad ones – there is little point in trying to draw in a few eyeballs of people who disagree with my perspective, it provides a short term bump, but there is no real value in it.

And by bad I don’t mean you are bad people 🙂 I just mean if you are stuck in your ways I wouldn’t want to bother trying to convince you otherwise – but I do see value in being a voice of reason when it comes to ‘deals’ and whatnot. Even though that isn’t fashionable.

I just diss on occasion, it something I need to work on, I have a big list!