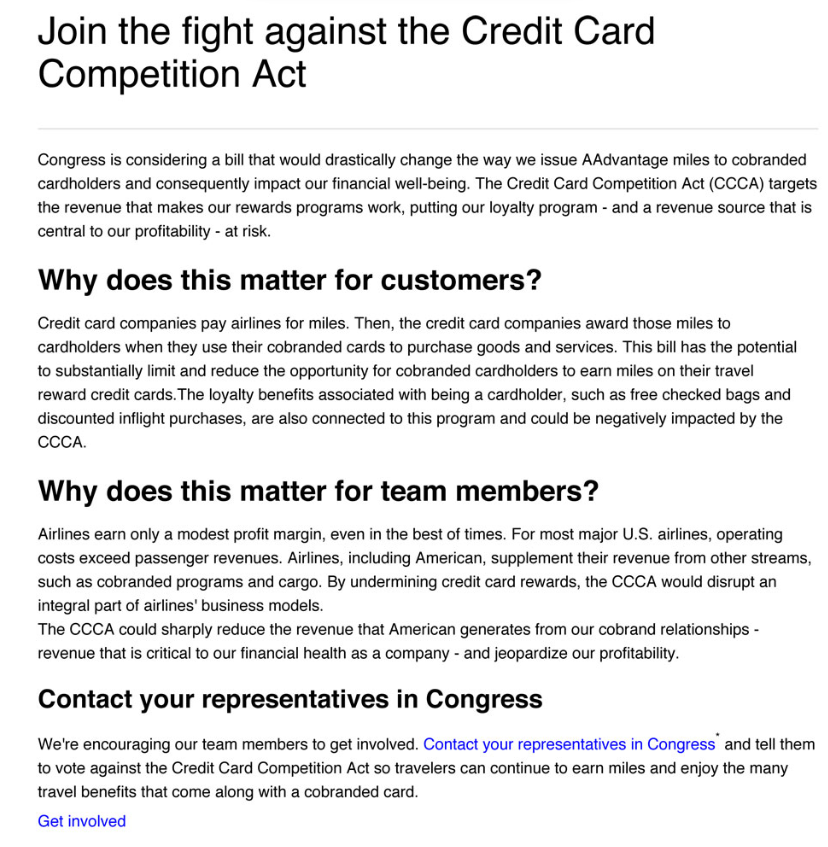

American Airlines is asking employees to lobby against legislation from Senators Dick Durbin and Roger Marshall that would limit credit card interchange.

Nothing is going to pass this year. President Biden was the Senator from the banks Delaware and hasn’t made this a priority. Heading into an election it’s the perfect issue to fundraise on both from retailers (who would love the gift of lower card processing costs) and banks and payment networks (who see an existential threat to their business). But threats to interchange remain an ongoing existential risk.

Interestingly, American presents the (true) argument to employees that they pushed back on me over for so long – that they lose money flying planes (cost per seat mile is greater than passenger revenue per seat mile, and even passenger revenue plus cargo, in many quarters) and only turn a profit by selling miles to banks.

Rewards may seem like a side issue but it matters politically to the extent it shows how consumers are affected (and shows consumers that they are affected).

In Australia, for instance, where interchange is limited we’ve seen an increase in credit card annual fees as well as a cap on rewards earned on many cards, and limitations in the availability of credit. We’ve also seen big Qantas devaluations. Cards could still earn one mile per dollar, but each mile would be worth less (less costly to Qantas to redeem) in order to account for lower revenue per mile.

Reduced credit availability is bad for the economy overall, but it’s also bad for consumers who are forced to use their next-best available credit option – revolving balances on a credit card may be less than ideal for many, it’s also a real need if you must fix a car to get to work. Your car still needs to be fixed, and you may find yourself looking at a payday loan with far worse terms.

- The Durbin Amendment to Dodd Frank which lowered debit interchange didn’t lower consumer prices even as it lowered costs to retailers (and limited access to banking, since debit swipes used to subsidize fee-free accounts).

- And credit card interchange limits in Australia and Europe didn’t lower consumer prices there either. In fact when Australian businesses were allowed to add surcharges to credit card payments, the government then had to step in further to limit those surcharges because retailers were taking advantage of consumers!

Retailers spend a lot on payment processing, but they’re also receiving a service in exchange – the near instantaneous processing of payments from customers!

When retailer lobby shops posit that the cost of card acceptance has risen markedly since the start of the pandemic, that’s really just (1) inflation, and (2) an indicator of success – they’re generating higher revenues!

And they’re processing payments in one of the least costly ways possible. Cash is much more expensive to a retailer, given incorrect change and employee theft (not to mention counterfeiting risk). Some retailers do prefer cash of course, but one reason is that cash transactions facilitate tax fraud while card payments are far more transparent.

Ultimately credit cards aren’t just a cost to retailers, they facilitate transactions that benefit retailers, but they also benefit consumers while bundling financing and consumer protection at the same time. Interchange companies are profitable because they provide an important service, and also innovate in convenience and combating fraud. Impairing their margins – by law – to benefit the bottom lines of big merchants undercuts all of those benefits.

This is about special interests pleading for favors from the government against the public interest, though retail lobbyists mask their interest in fake consumer benefit. Obviously for American Airlines and for other big airlines, big dollars are at stake too.

When Visa, Mastercard et al blocked their merchants from charging an additional fee for accepting a credit card, the Durbin amendment made sense. Now that merchants can charge a fee for accepting credit cards, this is a problem for the free market to resolve.

If selling miles to banks becomes far less profitable because of Senator Dufus (oops, my apology to Mr. Durbin) getting his special interest bill passed and signed into law, then passenger revenue per mile MUST increase to near to the cost per seat mile for airlines to avoid another appearance in bankruptcy court. Its basic economics 101. No wonder AA is saying this to its employees. Let us know Gary what the other three large airlines say to their employees.

Wow, Gary. I’m kinda shocked that they put that in writing. You’re owed ana policy by AA and some forum posters….

This is a non issue for Delta. They earn premium revenue from flying highly efficient planes, with premium seats and selling them at a premium.

Gary – I have to admit that I’m curious what you base your assertion on about cash being more expensive than plastic for business owners. As a small business owner whose business forks out thirty grand a year in credit card fees I’m frankly stumped how I would pay a tenth of that if I happened to only receive cash. As in pretty much any business, if my employees are short on cash that’s on them to cover rather than me or my business. Phrased another way, if I only received cash I could employ someone for 20 hours a week at $20 an hour simply to count money with no other job and still come out ahead.

@ Christian – I was genuinely curious: if those credit card fees went away, would the $30k go towards lowering prices to your customers?

Can’t wait for the thinly-veiled undeclared article paid for by the credit card industry on God Help The Points screeching about how consumer protections are bad for consumers.

@Christian I believe the crux is that cash requires more time to inventory, is significantly more vulnerable to theft (from employees or otherwise), and requires time spent going to the bank and depositing. $30k in interchange fee’s is obviously a lot, but it represents a savings of time and security over cash.

Merchant fees in the US are roughly 2% higher than in other developed countries. Inevitably that just becomes an additional overhead for all businesses, which all consumers end up paying for. It is in the general interest of the American consumer, although not of the airlines, to see such fees reduced.

@Richard – There’s so much false in what you’ve written.

In the U.S. there are more card payments, and those cards bundle more services for consumers as well as generating higher average purchases for merchants. It’s not some sort of overcharge.

It is 100% false that this is driving up prices for consumers. When interchange was crammed down in Europe and in Australia, consumer prices did not go down – it was just a giveaway to merchants.

@Christian – “I’m curious what you base your assertion on about cash being more expensive than plastic for business owners”

1. Employees make incorrect change and there’s loss of cash

2. Employees pocket cash

3. Large amounts of cash often lead to higher insurance premiums

4. Cash on hand = risk of outside theft

5. Chase has to be deposited, this incurs time cost, merchants often don’t do it daily and they’re losing return on the float vs.electronic deposit of funds.

I have stopped playing the airline mileage game, now find the cc with the best cash back. It seemed that when I accumulated enough mileage for a trip, the airline would devalue. Status was nice until the airlines started pre boarding half the seats.

@ted poco

If this bill were to pass you can definitely kiss cash back cards goodbye.

Gary, in the older days, I could easily negotiate an additional 5% off when buying furniture from a local store and paying by cash (personal check) vs. credit card. The store was locally owned, and the owner was happy not to pay CC fees and also getting money immediately without waiting for several weeks for CC payments. Even now my local well-stocked large store in a major metropolitan area and specializing in Asian food has a sign that they will not take cash for purchases below $10. A few years ago my wife was a treasurer of a small professional society with a non-profit status with the annual membership fees ranging from $5 to $25 annually. The CC interchange fees were eating a large portion of their member contributions. The interchange fee are significant expense if you run a small business. .

@Alex77W – a nonprofit isn’t making change and may trust its staff not to pocket the cash, reasonably or naively. A local store may just not be declaring the income…

For those who think they can/want to use only cash, the G will think you’re a drug dealer (or at least a tax cheat) & take your cash.

Merchants have a mercantile mentality. Of course they want something for nothing, or at least for less. Of course they will keep the money and not pass savings on.

Last time I was at the FLL airport, the fast food restaurant (Burger King?) would only accept debit/credit cards, and all I wanted was a small coffee!!

I’m surprised some consumer focused company (WalMart, McDonalds, etc) haven’t come up with their own swipe card servicing company. Or better yet, bought out an existing network just to control swipe fees. Heavy cost up front, but just a 1/2% savings per swipe adds up real quick!!

Visa, MasterCard, & Discover would blow a fuse, but something needs to break the monopoly.

@Gary – Apologies for the delayed response. I was away and missed following this topic but here are my real life counterpoints.

1. As I stated, like most businesses any shortage falls on the employee to make right.

2. Same.

3. My insurer has only covered $5K since we opened since cash is fungible.

4. Yes. This has never happened to us in decades in business but it absolutely is possible.

5. Of course you have to deposit cash in person, in our case by a salaried manager so no additional costs are accrued. Your mention of the float is inconsequential if the business has sufficient cash flow. If my business NEEDS that cash that badly then there are bigger problems that need to be addressed.

I have no idea who this IHL group is but in a best case scenario they’re making assessments that are skewed, more likely simply wrong. On my scale it takes around 30 minutes a day total for a salaried manager (including myself) to complete all dealings with cash. This counts weekly deposits. Dealing with credit cards alone with a blend of cash and credit takes around 15 minutes daily. I simply don’t see how that half hour a day currently, even doubled if we got purely cash, would be worth the approximately $75 a day I’m paying in credit card fees now.