Delta Air Lines has moved to spending only as a metric for earning status. And they’re considering no longer awarding full credit for your spending, unless you buy more expensive fares. That’s one lesson of a new product survey they’re sending to frequent flyers that helps them sort through how much extra customers will pay to earn qualifying dollars.

Other ideas being tested include,

- Bringing back change fees unless customers buy up to a more expensive fare

- Return of fees for getting help from reservations, with free assistance via chat features only

In other words, things that are available to customers now become ‘premium services’.

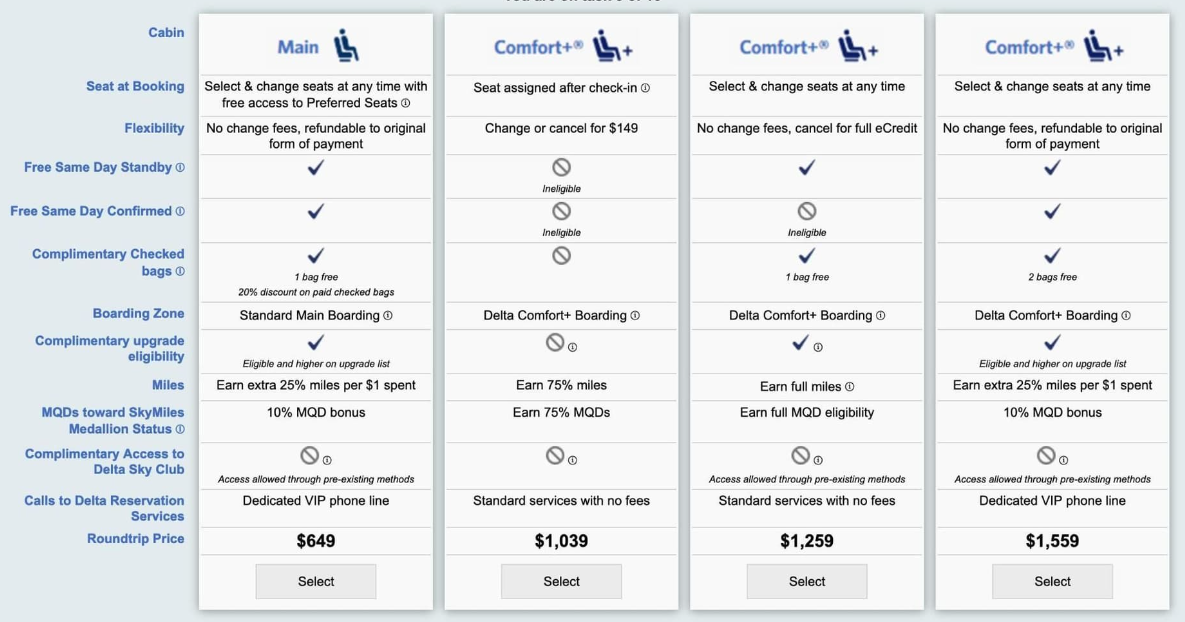

Delta has promised more premium segmentation, like they’ve done for coach with basic economy, regular economy, and Comfort+. Although Delta now markets Comfort+ as somehow being more than just extra legroom, but a different ‘class of service’ (except where that would mean paying higher taxes, such as departing the U.K.).

Comfort+ is ‘premium’. A Comfort+ middle seat isn’t really premium, though. And a Delta Platinum flying internationally in a Comfort+ seat no longer gets access to Sky Clubs. Less premium!

And they’re even testing segmenting the premium (first class) cabin by fare for seat assignments.

Customers taking the survey say “my blood was boiling by the end of it” after reacting to “the absurd offers presented.”

It’s obvious Delta is wanting to bring back change/cancel fees, add in phone fees, remove advanced seat selection, and overall continue their mission to charge more for less.

Delta may not make these changes, and they may not all be under live consideration. The survey is designed to test customer willingness to pay for different things, and to see what changes would cause people to move away from the airline.

There are ‘business’ and ‘leisure’ versions of the survey, and over varying flight lengths. They want to know which services and prices customers might live with. They want to know what the customer demand curve looks like (based on stated responses, rather than revealed preference or actual purchase behavior).

Delta is just a slightly nicer Spirit. Ed Bastain is a post turtle.

One could say that these changes, if they happen, are partly the fault of the government. If there was real competition in the airline industry, airlines would be more responsive to customer issues. However, all the airline consolidation has left most domestic flyers with limited choices. This emboldens the airlines to do whatever they want.

How much did they charge for filling out the survey?

I would love the option to just pay for seat upgrade and not miles, checked bags, etc and save $500.

Delta is not a premium airline. It never was. It never will be. No US carrier is Premium. They are all the same.

With a significant year end MQM roll over I was able to push my Platinum status out until Feb 1, 2026, but with all the egregious changes made to the program during the first week in January I quickly transferred out over $95,000 of recurring annual charges AWAY from my Platinum Reserve card, over to both my CostCo Visa and Discovery cards.

Now instead of spending my usual $7K+ per month on my Delta Reserve AmEx card, starting this year I am only using this card for my Delta flights, Lyft & Uber rides (to score their monthly rebates) & the 15 Sky Club visits.

Unless they make significant changes over these next 23 months I will then be done with all of it and will only fly Delta to keep spending down my stash of frequent flyer miles until those are also gone.

Gary. It’s all I can do to refrain from sending a hit man after reading this post.

Delta is, was, and always be, THE, premium airline.

Dang! Delta is making American look like Singapore Airlines in comparison. Would’ve never imagined that!

I got this survey. Mine was all focused on 4-6 hour domestic flights for business – not leisure in Premium Select or One Class. I rejected all and marked I would look at competitor flights or economy seats if they tried to implement any of the programs. Absurd that they would eliminate services (same day standby, checked bags, etc) when paying for Premium or business class!! I am Diamond – this survey leads me to believe they are going to eliminate a LOT of Diamond privileges in the near future…

I’ve been Diamond for 3 years, platinum before. I live in SLC, a hub. I AM 100% DONE W DELTA.. I will not fly them any longer. There is a long list of reasons but #1 became that they think I’m stupid and will play aLong w thier insulting changes. And you know what, so far I am happy to fly other airlines.

It’s a marketing test. Most of it won’t see the light of day.

And part of the purpose is to “float” ideas which competitors might consider as well.

The same chorus that argues that Delta is not premium can’t explain how it manages to consistently charge and earn more per seat mile than any other airline.

Clearly the hangouts on internet chat boards are a loud but tiny minority. Delta’s REAL customers pay more for its service and thus earns the title of being premium.

“relating to or denoting a commodity or product of superior quality and therefore a higher price. ”

150 plus million customers aren’t wrong.

Gary’s primary objective is to create premium page click revenue, facts be damned.

@Tim Dunn

Your proclamations about Delta are like claiming you picked up a turd from the clean end. Just because they may suck a little less in some areas doesn’t make them great.

I just took a Delta “comfort class” trip and it was far worse than basic coach in the days before dysregulation. In fact, it was horrible, from the poorly cleaned and maintained plane, broken PA system, lack of sufficient storage for customers in other classes, iffy ventilation, filthy washroom, and utterly awful food.

This race to the bottom is precisely why regulation setting basic rules is necessary. Somebody tell that oaf Buttigeig.

Maybe that price I paid, thousands more than the people in coach, is 1970s coach plus inflation. No value added, that’s for sure.

H2,

you STILL don’t get that premium is not defined by YOUR perception of quality.

Premium is defined by what customers are willing to pay and Delta most certainly does lead the industry in that regard

I’m not sure why you and others are so dense.

How DARE you post anything negative about Delta, the universe’s #1 premium airline?!?!?

Wait til my Daddy calms down and actually posts something more substantive than what he posted above, you’ll all be sorry!

@Tim Dunn

If by industry you mean our poorly rated airlines in the United States, you’re probably right. I have flown the Asian airlines and have experienced premium service. Being the fourth ugliest girl in school does not make you pretty.

@ Gary — Well, if Delta brings back change fees that just proves with a liar Hauenstein is. UFB. Only Delta.

Tim Dunce aside…Delta is proving once again that they truly believe they’re better than they actually are…and we’ll prove they’re not by keeping our wallets closed.

Good riddance.

Um…I’ve flown Comfort+, and it’s basically what coach *used to* be back in the day. It was better than Main Cabin (I wound up flying all three domestic cabins in one vacation), but it was the bare minimum of what I’m accustomed to on a flight—little different than my usual Southwest trips, but with a mimosa. Yay.

And I’m not saying this to bash Delta, because I actually do like them a lot. They accommodated me well during the flight cancellation. But I wish that people as a whole would quit acting as if they were some magical, mythical premium unicorn airline that’s justified in charging $500 for a $200 flight. That’s why I call them the Taylor Swift of airlines.

okay, i retract my assertion from the love field gate thread

tim dunn is not a 14-year-old son of a delta employee

he is an AI bot paid for by Gary to stir up controversy

to wit:

“The same chorus that argues that Delta is not premium can’t explain how it manages to consistently charge and earn more per seat mile than any other airline.”

This is a perfect example of how AI algorithms fail when deep nuance is needed to avoid the fallacy of false association (i.e. post hoc, ergo propter hoc.)

“Tim”, i can pay $4.50 for premium gas on the interstate or $3.50 for regular in my neighborhood, but in both cases it’s still liquid carbon with a difference of 4 octane.

Cost has no direct correlation with “Premium” or “Comfort” in US commercial air travel.

@ Gary — And how the hell can the justify giving less than 100% MQD credit? A dollar spent is a dollar spent. Obviously these morons gave no thought to the name of their status ” metric.” Medallion Qualifying Dollars was an incompetent choice. At least United had the foresight to change the name of their metric several years ago. Delta apparently doesn’t fully understand the rage of their “loyal” customers. I guess they will issue another round of insulting changes and wait for the angry backlash AGAIN.

@dodged. Hi find that highly insulting

Tim: “The same chorus that argues that Delta is not premium can’t explain how it manages to consistently charge and earn more per seat mile than any other airline.”

Anyone that reads Delta investor day publications can explain that because Delta says it: Interior monopoly hubs that drive their profits in conjunction with low costs at those interior hubs. There’s probably some small RASM premium from customers that prefer them, they do have a loyal group of kool aid drinkers, for sure, but even delta says it’s much more to do with their interior monopoly hubs when they’re talking to investors about their sustainable profits. It isn’t rocket science. Delta is a very well-run company (not a cult or your family, Tim) but they’re quite open about what enables their growth in coastal markets and profits and it isn’t really their brand, it’s the profits they use to subsidize other hubs.

Don’t mean to be overly simplistic about this topic, like Tim always is, but Delta is quite blunt that their monopoly hubs drive their profitability.

It’s funny how Tim raves about how “no one can explain…” uhhh. yes you can because Delta says what it is and, thankfully, their investor relations department, while sending out the shiniest version of Delta, is a bit more honest than Tim.

@ MaxPower — Honest is not a word that comes to mind whan discussing Delta.

I am a DL 2 Million Miler. I was Diamond for the first 6 years or so of the program but got over the top on the spending requirement with credit card spend. You may remember that at some point, to make Diamond, the card spend requirement went from $25k to $250k, a tenfold increase! I have been Platinum ever since. I had the Delta Amex Reserve card for many years but recently dumped it in favor of the Amex Platinum Card.

Unlike other commenters, even though I agree that DL has deteriorated a lot over the years, I will still fly them if the price and service are right and I generally like the onboard service. However, I am no longer tied to DL. Recently, they actually did something positive for us long time elites. In my case, I am now lifetime Platinum for being a 2 Million Miler instead of lifetime Gold. However, I no longer fly for business so will likely never get 3 million miles to make lifetime Diamond. I have enough MQMs to get to Diamond in the one-time conversion process but am still trying to make up my mind if I care. To me, the best Diamond perk has been global upgrade certificates but they have been hard to spend. OTOH, converting to spendable miles isn’t all that appealing as their value has depreciated so much.

max,

first,

if Delta gets so much from its core 4 (US interior) hubs, WTH have AA and UA been doing for the past 45 years of deregulation that DL has done?

and the internet is FULL of assertions that DL loses money on its coastal 4 hubs.

Neither of which is true. Delta has captive hubs – but so do AA and UA.

The simple fact is that DL gets more for its services and that includes from its loyalty program and credit card relationship.

Are there structural advantages such as that Amex charges merchants higher fees so they can share more revenue with Delta? perhaps

Did Delta outsmart AA and UA by winning engine maintenance contracts with all 3 of the global engine manufacturers such that DL lowers its own maintenance expenses and “subsidizes” its own employees and fleet? sure… but then why was AA and UA incapable of doing the same?

does Delta save over $1 billion/year on fuel costs compared to AA and UA because they had the foresight to buy a refinery which saves them on every one of the 4 billion gallons of jet fuel they burn? absolutely. Again, why didn’t AA and UA figure out a viable way to reduce their fuel costs as much?

the simple fact is that DL doesn’t get a huge revenue advantage from its core airline operations but certain does get some. They simply have developed a better business model which allows them to pay their people more, run a more reliable operation, and in turn get more high value business including in the highly competitive coastal markets.

btw, do you realize that AS had a net income margin of just 2% in 2023 – less than 1/3 of what DL got. B6 was unprofitable. Do you suppose that DL really can get by with small profit margins in these coastal hubs because their primary competitors aren’t any more profitable?

DL’s profits DO come heavily from its core 4 hubs but that doesn’t mean that their coastal 4 hubs don’t make money and the extra money DL earns compared to AA and UA is because of the better total business plan DL has over AA and UA.

And customers do pay more – via lots of channels – which means DL does have a premium product – whether you or anyone else can accept it or not.

One of the complaints over the last few years is that the Diamond population was too high, many members reaching that status on card spend alone. This made competition for upgrades tight, often pushing true frequent flyers down on the list. Frankly, I’m happy to see the requirements tighten up. I’m sure that’s why some of the other comments are about giving up on the various AMEX cards. I’m sure that I’ll drop my Reserve card when I retire in a few years.

Until then, the system is working for me.

I’m just spending down my Delta miles. I am a 2 million miles but since retirement fly infrequently. I have flown SW, United American and British Airways since retirement. Delta is not a premium airline at all, it’s the same as the others except SW which has no premium cabin or assigned seating. United is just like Delta, American slightly behind. British Airways and Air France are better than any domestic airline. I do have lifetime gold status on Delta but their dates are always higher. Ed Bastin is a dreamer if he thinks Delta is a premium product. Hope the flight attendants vote in the union just to irritate the ego maniac Ed.

and, btw, MAX, do you remember not that long ago that AA touted its high margin hubs at DCA, CLT and DFW but the size of those margins meant they had to be losing money in some hubs – and they said as much about NYC – just bolstered by how they allocated credit card revenues?

And UA loves to talk about its international network but there is hard data – whether you or anyone believes or not – that says they make significantly less than Delta in the same international regions. and when you add up all of profits in UA’s regions – including domestic – their domestic hubs really don’t deliver higher profits even though they talk about how huge those markets are and how well-positioned they are.

So, Delta DOES tell us that its coastal 4 hubs drive the majority of its profits but it doesn’t say their coastal 4 hubs lose money – because they very likely cannot given how much of their network is in those 4 hubs. Add in that AA and UA don’t tell us where they lose money or break even at best even though they underperform Delta and it is clear that everyone believes what they want but the clear evidence is that AA and UA neither make as much in their best hubs – and the question is why they can’t match DL – and then do a lot of flying that is not profitable.

feel free to explain that reality and then you’ll understand why Delta is indeed premium.

Plain fact MSP, DTW, SLC, ATL are all uncontested hubs – no other passenger airport in town competing for fliers

AA only has PHX, CLT on that basis

UA only DEN

Margins are higher when you have less competition, not anything ‘premium’ about it

They also just raised their checked bag fees 17%

Only a Premium airline like Frontier or Delta would nickel-and-dime customers like this, even in first class.

WTH do you think MIA is? they have an uncontested hub from the largest single airport to an entire region?

DCA is also an AA hub.

And DEN is very much contested. WN for years carried more domestic local passengers – but not revenue than UA.

And UA has multiple hubs where there is no other airline hub at the same airport even if there are in the same metro area at another airport.

but, if that is the case, why hasn’t UA figured out how put its hubs in places where it would get that premium? We are 45 years into deregulation and AA, DL and UA all have had the same amount of time to execute their strategies.

DL is more profitable because it has executed strategies that other carriers have not been able to match, have reaped higher profits from them, have reinvested more profits in its core airline business, and won more corporate revenue where it matters most – and the result is that DL gets more revenue – both passenger and total revenue – per seat mile than any other airline.

DL developed the premium finance airline model that no other airline in the US has been able to duplicate.

I received the leisure version of this survey. They’re also proposing only a small % of MQD on most fares. Eliminate Sky Club access for most Delta One fares. My answer on almost every screen was I’ll be looking at other airlines. I’m a captive in ATL too but there are options. I don’t expect anything positive for next year unless the economy tanks before then.

No this can’t be happening.

My head is about to explode.

Tim is arguing with Max which was said by Delta on investor day.

Therefore Tim is arguing with Delta?

But Tim can’t argue with Delta. Because Delta is premium so they are always right, backed by 150 million customer.

This Premium paradox is mind boggling.

I rarely get drawn into the who’s right…who’s wrong arguments here but find myself drawn into the discussion of what “premium” is. It seems to me that there’s a disconnect between what most of the posters are saying and Tim Dunn’s responses. The former are saying that Delta’s recent actions belie it’s status as a premium airline. Dunn says if they generate premium revenues they, definitionally are a premium airline. History is replete with cases of premium products and services which lost that status with a lag as they degraded their product or service, raised prices too much or allowed themselves to become obsolete. So most of the posters are really arguing that Delta increasingly doesn’t deserve to be considered a premium airline.

329,

the simple fact is that the few people that write on the internet DO NOT SPEAK for the majority of Delta’s customers.

We heard endlessly last year w/ Delta’s mileage program changes that millions of people would walk away – and that is absolutely not happening.

I copied the definition above and the definition of premium is based on what customers are willing to pay.

Delta simply collects more revenue per seat mile than any other airline – and what anyone THINKS about how premium Delta’s service is or is not SIMPLY DOES NOT MATTER.

The reason there is a perceived disconnect is because people want to equate their OWN ANEDOTAL perceptions of how they have experienced Delta service and try to impose that on 150 million real customers without considering the price those 150 million ACTUAL customers pay.

When Delta actually stops generating the premium, THEN AND ONLY THEN, can we say that Delta is not a premium airline.

We can all blur reality by our own personal experiences and by what we THINK or EVEN HOPE might happen but that doesn’t mean that is fact.

MIA has FLL and PBI as a crosstown bleed

DCA has IAD and BWI as bleed and on and on for pretty much any coastal hub except Seattle (though Paine is now there)

Looking at mid continent where the big margins are…

ORD bleeds to MDW – UA/AA

DFW to DAL – AA

IAH to HOU – UA

CLT no bleed – AA

PHX no bleed – AA

DEN no bleed – UA

ATL no bleed – DL

DTW no bleed – DL

MSP no bleed – DL

SLC no bleed – DL

That’s the difference – only Delta has all of its mid continent connecting bank hubs with no contest from another airport in the region.

See how quickly DL gets defensive about even an inkling of a smidgen of traffic at an alternate Atlanta airport – and you see how that’s the golden goose that they will defend more than anything else. Avoiding crosstown airports at a domestic connecting hub.

So I flew Delta for the first time in 20y on a paid F fare because they had the times I needed.

Check-in at Bozeman was pleasant, they had fresh popcorn at the gate. Nice experience, was pleased.

Flight to MSP was ok, service was meh, did get a PDB, snacks were meh, seat had a lot of pockets but both were incredibly dirty, crumbs etc.

MSP-DCA flight was delayed even though the plane had been there all day. App didnt show reason for delay nor did it ever update with the swapped aircraft, CS center Red coat had an attitude like how dare I ask why their flights are delayed.

Onboard pilot blamed the late arriving aircraft for the delay, even though it arrived early by 30m, not once did they ever acknowledge that our original plane went tech and was swapped.

Service to DCA was good, food was inedible. Cheese plate had stale cheddars and 10 small salamis and some terrible dessert. The smoked chicken ravioli came out cold and when finally warm enough the zucchini was mush. Two other passengers sent their food back as dry and inedible according to the FA when I told her how bad ours were.

In the end there was NOTHING premium about the experience, it was a typical flight on a US airline that couldn’t even be honest with us about delays.

AA’s food in F on the way out to BZN was much better but their service was even worse.

At least I can be a free agent and buy F where it’s best for me and not have to be loyal to a company that is purely transactional.

Delta is Not, never was, and NEVER will be a premium airline. The resident Delta-bot propaganda machine is working overtime today. Bottom line? DeltaSUX.

greg,

it is beyond laughable to argue that DL gets defensive about a 2nd airport in the Atlanta area considering the mess in N. Texas that has still not been resolved.

And you and others can’t get that N. Georgia has built up to the point that the majority of people in each proposed community for a new airport wants another commercial airport in their area. Pinning the blame on Delta when it is the actual residents that have decided the future of N. Georgia airports is beyond blame.

And, again, ATL is the only one of these hubs that was a DL hub 45 years ago. How did Delta manage to defend Atlanta and acquire 3 new hubs and AA and UA weren’t capable of figuring out the same advantage?

And, if you are happy to argue how much of DL’s profits come from its core 4 hubs, then you clearly are saying that AA and UA’s bubs are not near as good as they paint them OR they have a whole lot of dead wood alongside some mediocre hubs. Which is it?

I’ll accept the “DL’s hubs are in better metro areas” for them to price higher if you will accept that AA and UA”s hubs are not near as great as you and others make them out to be.

and given that DL is growing its network in major coastal competitive markets like BOS, NYC, LAX and SEA, what is AA and UA’s future if DL uses all of these much larger profits ($2 billion more than UA and $3.75 more than AA in 2023) keeps taking share of AA and UA’s large coastal markets?

Scott,

again, your PERSONAL experience doesn’t matter one iota in determining whether DL is premium or not given that they carried 175 million passengers in 2023.

No one’s experience mattered. What matters is what people paid to fly DL.

At least greg is arguing the right subject – he just has to come to the logical conclusion of his arguments.

Delta flies premium flights from MSP, DTW, and other premium hubs. When they fleece their elite, discerning guests, they do it in a premium fashion.

@Tim Dunn “it is beyond laughable to argue that DL gets defensive about a 2nd airport in the Atlanta area considering the mess in N. Texas that has still not been resolved.”

No, there’s nothing inherently wrong with multiple airports… LGA/JFK (and for that matter EWR)… SFO/OAK…. ORD/MDW… DAL should absolutely still be open, Congress shouldn’t have capitulated to the deal to carve up Dallas and cap Love Field gates.

And Atlanta might benefit from another airport. Delta wouldn’t, sure. And Atlanta benefits from Delta, just as Charlotte benefits from American. Delta plays some serious hardball with local pols. And with the airport. Even without slot restrictions the airport makes it as hard as possible within or just past the line of what the FAA will let them get away with in terms of how they treat new entrants (think back to B6’s entry into ATL).

Atlanta would benefit from more gates, whether those ought to be at the same or another airport. Paulding Field is a legit 1-2 hour drive from ATL…

Wait! I think I finally get Tim Dunn’s argument. And he’s right. Delta’s prices are premium even if their service isn’t. I get it now. Every one else is arguing about them not providing premium service while Tim argues it doesn’t matter because the price is premium.

Tim is arguing with Ed again?

What a confusing day.

“the simple fact is that the few people that write on the internet DO NOT SPEAK for the majority of Delta’s customers.”

That’s not a fact, that’s your assumption, aka pulling a Tim Dunn fluff.

Ed wouldn’t admit to ripping the band aid and backtrack if the people who write on the internet DO NOT SPEAK for the majority.

Delta has the most favorable margin profile because of the margin profile of its mid continent hubs – ATL largely, then MSP, DTW, SLC – all enjoying no cross town competition, favorable connecting geography, and corporate bases large enough to support one, but not two global carriers.

There is little premium about the hubs or the airline’s product that earns the margin at those hubs. you could run an AA product on time with those hubs and have higher RASM than peers.

It then uses the excess profits from those hubs to try and grow in more competitive markets that have larger total profit pools but less per carrier because of multi airport bleed and being so large they can support marginal players.

To play well in those markets you need to have top reliable and premium offering, which is costly.

DL has more profit from those midcon hubs to throw around and can accept less of a margin in LAX, NYC than UA or AA who rely more heavily on those markets for their profit.

Reliability was one of the higher cost differentiators, that’s what DL led with in the 2010s, and now UA/AA are eating the cost to be more reliable relative to DL than in the 2010s.

An interesting question would be if shareholders would be better off if they retreated further from coastal hubs that are profitable, but not as high margin and return as the midcon hubs – and returned the excess to shareholders. How much could the stock move with a really aggressive buyback/dividend program?

What a “spirited” discussion!

Just another way to fleece customers for “maximum revenue extraction.”

Along with the Amex Delta Gold card annual fee going up to $150 a year without a true corresponding increase in benefits, this is a poor decision for customers, and those who WERE loyal to Delta. I emailed them about the fee increase, hoping for a little more information or even sympathy, but got a terse corporate response, so I’ll be cancelling that card before the fee increase for me (which apparently will be in May even though my $99 annual fee was charged in January and they announced the increase last month…I thought I’d escape until next January but they just keep trying to squeeze us all out! I think I’ll switch to a Capital One card that gives refunds for ANY extra flight costs like baggage, I think up to $200 a year if I remember correctly.

@ Gary — Much of Georgia suffers economically because of the lack of another ATL area airport. If you live in midsized cities like Macon or Athens, you are screwed when it comes to airport access. There are many other parts of Georgia that are so inconvenient for air travel that no one will move there. It is time for another Atlanta airport, ideally to the East.

Greg,

we are finally getting there. Mostly.

The only part that you missed is the much higher non-transportation revenue – Amex, loyalty program and MRO revenue – and the lower costs from the refinery.

ALL of that PLUS the higher margins DL gets from its midcontinental hubs is what allows DL to subsidize not just its coastal hubs – which are still profitable but at lower margins than its core hubs – but also its employees’ higher salaries which help it deliver better service.

And, while the service at Delta is measurably better, it is indeed the network and non-transportation revenue that is what gives DL the revenue advantage.

DL’s marginally better revenue IS enough to help it win corporate revenue which is higher revenue and DL has been masterful in going into companies that have corporate agreements with AA and UA and win their corporate revenue where doing so allows DL to grow its network.

and, Gary, you once again are patently wrong. The citizens of the areas where proposed airports in N. Georgia could be built/expanded HAVE VOTED that they do not want commercial service. If DL is capable of convincing all of the people of N. Georgia that ATL is the only place that should have commercial service in N. Georgia, then Delta wins the prize for corporate brainwashing to do it to 7 million people.

And, again, why couldn’t other airlines figure out how to do the same thing in their hub metros?

it is a flat out lie that B6 wasn’t given gates at ATL. They wanted sole use of gates on an international concourse (E) for domestic flights. No other airline including Delta is allowed to do that.

Your commitment to what you think is true is admirable but it is no wonder that you attract so many readers that don’t know what they are talking about when you don’t either.

Gene,

Athens has air service on AA to CLT; DL doesn’t fly there.

any additional airports in N. Georgia would be north of Atlanta which would do nothing for Macon.

Macon is too close to ATL. It is closer from Macon to ATL and a much easier drive than from ATL to a number of points in N. Georgia

and if you want to talk about forced inconvenience, let’s talk about Denver’s decision to close Stapleton when DIA opened.

@ Tim Dunn — Please do not reply to my comments, as I will do same

I do not care what you think.

I have been a loyal Delta customer for many years. I am now going to cancel my Delta Platinum Amex card because it is not worth being loyal to Delta. We will now just shop other airlines.

@Tim Dunn

Then Walmart must be super premium. It has 230 million customers a week.

BTW you are wrong about premium prices. Look at places where they have competition. They are often the cheapest of the big 3. That’s why I bought tickets on them SEA to RDU. Lowest prices for a non-stop. Not because they were premium.

Wow

Say something from delta IR and Tim goes nuts.

Calm down, Timmy. You don’t seem to know much about the industry if you’re comparing Miami and dca to the market share of atl, MSP, dtw, or SLC… even your reply betrays the absolute ignorance of why aa and Miami isn’t as profitable. I’d say you’ll find out when delta adds a few flights from Miami (that you claim is the death of aa in Miami after a few drinks despite the actual gate capacity making you sound very stupid…)

You really should look at your beloved’s investor day slides.

They’re quite a bit more transparent than you are.

Why? Because they want investors to believe their profitability is sustainable and “great FAs and better food” are not sustainable from a financial perspective. One bad move and the FAs get mad and better food is matched or surpassed easily

It’s amusing for everyone when you reply a few times with 15 paragraphs but get a grip, buddy.

I’ll reply to whoever I want, Gene,

Max,

you are incapable of understanding that I am saying the same thing that DL’s investor presentation and Bastian is saying.

DL gets more revenue from passengers and other sources.

While you and everyone else argue, DL just keeps growing its presence in other carrier strength markets.

Yet another example. DL pilots have been told that NYC will be an A350 pilot base – something I said would happen as DL adds flights from JFK to Asia, markets that other carriers but not Delta serve.

The A350 can do what the 787 cannot – which is why DL flies from DTW to PVG and makes it work but UA bailed on EWR to China, BOM, and HKG.

DL simply uses its network better and smarter than its competitors.

AA and UA could have hubs in cities that only have one commercial airport but they didn’t do that, didn’t merge w/ carriers that had those advantages, and don’t generate the revenue that DL does even though UA esp. touts how great its network is – but facts show it clearly isn’t that great in reality.

Airline industry is overspending and overconfident post covid. The cycle will hit along with huge layoff as history will show. Buying a lot of planes.and eventually will lose customer base. This cannot continue.

Past….Little Timmy,

You’re an imbecile and a Delta lapdog.

Everyone else,

Little Timmy will now spend 30 minutes thinking of insolent and clever responses which will turn out to be insipid and inane..

In those 30 minutes, the world will be a little calmer.

You’re welcome.

Oh tim

You look at the markets you want and have no idea what’s happening to delta’s core markets

It’s actually cute how ignorant you are to what delta is dealing with

Your ignorance coupled with 8 paragraph nonsense is fun

Thanks

Your stupidity never ceases to amuse everyone

Meanwhile, Delta continues to make billions more than American or United and all you are capable of doing is insulting me and still can’t explain how AA and UA screwed up so royally for the past 45 years and can’t make as much money as DL.

And they can’t deliver the on-time, lowest cancellation rate, baggage handling, oversale or customer complaint ratios that DL does either.

So you resort to childish name calling.

You are a loser. A loser on full display for all the world to see.

The network merger chess player wasn’t Delta, it was Northwest (and Anderson is really NW)

DL’s vision was to pair up with CO in the 90s and got rebuffed (should be thankful given the overlap) – NW got the golden share in CO

NW/CO was blocked by the Feds in the 90s and set the stage for DL/NW

DL and NW filed all but coordinated bankruptcy and NW mgmt shortly ran DL

AA pre US, UA pre CO wouldn’t have had the same advantage combining with NW – no single airport city southern hub

UA / Delta could have been something in the middle adding ATL, getting to rationalize out one of SLC or DEN, coasts already built out, but lacking the fortress midwest hubs and the UA union too large relative to Delta threatening the Delta FA non union status.

UA / US another middle ground one getting CLT and rationalizing one of PHX/DEN but stuck with competitive ORD for the midwest. Tilton didn’t get that done.

US / NW would have been a domestic powerhouse lacking Europe/Latam but lost in all this is not even Anderson in 2008 saw that domestic connectivity would be the profit center of the 2010s – moves were about feeding global networks based on the experience of the 2000s

We all know loser isn’t a childish name.

Greg is the only one that has proven he is capable of an intelligent conversation.

DL was the first to emerge from bankruptcy and became the controlling company. There were significant members of DL’s exec team that were not from NW at the time of the merger and even less now.

DL did look at UA during UA’s bankruptcy and was interested in the SFO hub but, you are right, did not want to run the risk of having an all unionized workforce.

They didn’t gamble on UA, UA merged with CO, and the whole reason we are having this discussion about hubs is because UA’s network people were all ex-CO people. CO had no market share outside of its hubs, still doesn’t and that is what Kirby is trying to fix.

DL was the first megamerger and UA/CO were smart enough to go next and AA and US were the two remaining ugly girls.

none of which changes that even the DL/NW and UA/CO mergers were over a decade ago; AA/US was right out a decade ago.

DL has managed to not only grow its combined network into more competitive markets than any of the big 3 AND ALSO defended its core markets better than AA or UA.

DL has offset what it did not gain through mergers and asset acquisitions through foreign equity. DL overcame UA’s larger size at LHR w/ the VS acquisition.

DL’s equity in Korean offsets its hub loss at NRT given that ICN is a larger local market than NRT and also a larger connecting airport.

DL’s equity and JV with Latam will provide DL with the first ability to challenge AA to Latin America. DL with LA is already the largest airline from NYC and LAX to Latin America.

UA’s greatest win was against AA at ORD but it screwed up NYC and DL is much larger – 15% – than UA, something that was not true of either UA or CO before until just a couple years ago.

UA is fighting and has regained the largest LOCAL carrier status at DEN from WN.

Neither AA or UA have added any new hubs as DL has done with BOS or SEA and DL, which was the smallest at LAX at deregulation is now the largest.

and size in the airline industry – as with all network businesses – translates into pricing power. DL also delivers quality – including industry-leading reliability – which is why it has managed to win over corporate contracts even in competitive markets.

DL simply is running a better business, its customers pay more, DL pays its people more, and DL is able to keep growing its network.

And no one has yet to be able to explain how AA or UA are going to be able to stop DL given that DL makes more money, is healthier financially, and is spending less of its revenues to grow than AA or UA.

thank you, greg, for the intelligent discussion.

the value of CO/DL would have been a Texas hub which still would have been smaller than DFW, greater access to Latin America from Texas which could have combined very well with ATL – but most importantly NYC.

DL only had about 20% of LGA slots pre-NW merger so there might not have been antitrust issues.

DL plus the ex-US LGA slots plus NW’s twin Midwest hubs are stronger than what CO offered.

The only part that DL didn’t get was a Texas hub.

Neither CO or UA had a Florida hub and neither were large in Florida and UA still isn’t now.

While everyone loves to tout the superiority of their hub, the big 3 are fairly equal in strengths and weaknesses.

DL just happens to generate more revenue from its network. DL has the best blend of a strong domestic system w/ a strong international system which, though not as large as UA’s, generates more profits and is better connected to more of the US.

if UA succeeds at its growth plan, it will be a very strong competitor to DL – as DL exists today.

Few people realize what DL will do to grow both domestically and internationally.

AA will still be a large domestic airline w/ a few international routes other than to Latin America which DL will match.

tAim, how did delta acquire the 3 hubs it didn’t have 45 years ago?

seriously?

pop quiz: name the DL pilot bases 45 years ago

After several bad experiences last year personally, for those I recommended & booked on Delta, plus reports from friends & family about their flights or those of their friends, at least as far as Main Cabin/long haul Comfort+ is concerned, Delta is NOT nearly as “premium” as it used to be.

So, for all of the international segments to/from Asia booked for others so far this year, NONE of the long haul flights are aboard Delta (3 are Korean Airlines, 2 Japan Airlines).

For a recent RDU-LAX-RDU booking made for others, that, too, was NOT on Delta despite it offering nonstops in the market.

Finally, for our own travel, our upcoming 6th & 7th flights of the year (NYC-CLT-NYC) next/following week are aboard United, NOT Delta, as there isn’t much of a difference inflight anymore that makes the misery of JFK Terminal 4 worthwhile anymore, especially when Newark is the easiest & closest airport for us to use.

Delta is NOT nearly as good as it used to be for most flyers, and its long haul flight last November from Seoul to Atlanta in Comfort+ was flat out awful, especially the inedible food.

That the airline is even considering reimplementing change fees & reverting back to the bad old days of intentional product degradation & “hate selling” is hardly surprising as although the airline (and a certain fanboy) may still view itself as being “better” than others, our own experiences (note: plural) and those of people we know & trust last year speaks to a degree of ordinariness & mediocrity whether the airline (and its main cheerleader) admits it or not.

Anyone who’s still being duped by airline “loyalty” programs is just a willing victim at this point.

Timmy D. here is the real life equivalent of South Park’s Timmy. One always knows ahead of time what he’s going to say…

at least you have the self-decency to make it clear you are not rather than posting under someone’s user name.

and howard,

the beauty of the free enterprise system is that everyone gets to choose what they want. The only mistake you make is in assuming that your choices are anything more than your choices.

Delta still carries far more revenue and passengers and makes far more money than United.

Hagbard,

I can’t tell you w/ certainty but Chicago, MEM, DFW, MSY and BOS were all pilot bases in the past 45 years; I have no idea which were 45 years ago.

And the point is that DL decided to not try to compete with AA at DFW and ORD and UA at ORD – but instead merged with NW which gave it two of these “monopoly” hubs which others are quick to say is how DL makes so much of its profits.

Again, why couldn’t AA and UA figure out what DL saw decades ago? Having hubs in markets which you can dominate results in better earnings. DL has spent 45 years building its core hubs around that principle and has used the extra earnings to grow in competitive markets – and have a larger presence in NYC, BOS and LAX than any other airline. NYC and LAX are larger markets than every other hub for AA and UA.

And Delta figured out that investing those extra profits in more amenities and higher paid employees leads to a cycle of more profits and more growth.

Just got my renewal notice for Delta American Express card. Cancelling account since there appears to be no value added to AMEX card from DL airlines. Surpass cancellation next. Chase Hyatt card seems to offer more actual rewards and benefits.

I think it doesn’t speak well of Delta that first class on their branded-partner regionals tends to be better than on their mainline planes.

But I also think this was inevitable. It’s capitalism at work. They’re going to wring as much money out of us as they can while delivering as cheap of a product as they possibly can just like any other business.

It’s always going to be a race to the bottom. If those idiotic “standing” seats ever get approval, guaranteed first class will drop to what is economy today while economy is a standing cattle car.

Meanwhile the planes keep getting more janky because Boeing has decided it’s no longer in the airplane building business but is instead in the moving-money-around business.

I long ago determined customer loyalty is a farce. If you sell me a good product, I’ll buy from you again. If you sell me a bad product that time, I’ll go elsewhere, and I don’t care that you’re waving a $5 discount for a basic economy seat in front of my face. Loyalty programs are designed for only two things: Tracking you, and trapping you. The first one doesn’t so much apply to the airlines because they already have your info – moreso for all the other loyalty programs out there like coffee shops, fast food restaurants, etc. That 25 cents off of your Starbucks latte made the company a lot of money selling your information and purchasing activity to data aggregators.

But the trapping you side is absolutely what’s going on with airline loyalty programs. “Gee, this sucks but I can’t fly the other airline because I have all these points here!” So they can ensnare you into the sunk-cost fallacy and then continually degrade your experience with a much higher threshold of irritation before you get sick of it and fly a different carrier.

Re the “CO execs dont know how to compete” trope…

It built our EWR in the 90s and 00s when NYC metro was well developed and competitive.

Their growth included market share gains from pm Deltas weak ex Pan Am JFK operation, US at LGA on domestic, UA intl at JFK

Hauenstein the #2 at DL and commercial architect came from CO under NW’s Anderson. Both intimate with each position. because of NW/CO

What did DL do post merger?

Run the CO playbook in NY

Be #1 on time

Consistent paint jobs and interiors with cleanliness

Large destination menu

Punchy one liner ads

Build out the intl gateway facilities over 5-10 years

Poach corporates with direct status matches locally

NYC is a blip on DLs profit they could have done none of that save for being on time and still be a revenue / margin leader in the US. But the notion that CO execs can’t compete is bunk. They wrote that playbook.

Tim,

While Delta has dominated Atlanta over the past 45 years, it has also benefited from:

1) Eastern Airlines (OG) labor strife, especially after airline deregulation began (late 1970s into 1980s) in the pre-Lorenzo era (aka Frank Borman), followed by the chaos, catastrophe & bitter labor relations (aka union busting) after the disastrous Frank Lorenzo gained control of an already badly wounded Eastern in 1986 & then destroyed it before the bankruptcy court appointed Martin Shugrue, Jr. Trustee in April, 1990 – eight months before Eastern’s demise in January, 1991.

2) After Eastern failed in 1981, Delta’s reign was briefly challenged by ValuJet, until its rapid expansion & mismanagement resulted in the catastrophic crash of flight 592 shortly after take-off from Miami on May 11, 1996 when everyone aboard perished.

3) Although ValuJet purchased AirTran in November, 1997 to rebrand after the above mentioned crash & began challenging Delta again in Atlanta, all of that seemed to fall by the wayside after Southwest took over AirTran in May, 2011 & instead of using its deep pockets & good credit ratings to aggressively expand in Atlanta, has instead been more than content to play a distant “2nd fiddle” & also ran in Delta’s fortress hub in Atlanta – all while conveniently keeping other airlines, especially discounters like Spirit, Frontier or perhaps hybrid airline, JetBlue, from building a more vigorous hub in Atlanta than Southwest has to date, with its decidedly underwhelming, seemingly oligopolistic friendly, token “competition.”

Sure, Delta has been smart to make the most of its prior competitors’ mistakes & mismanagement in Atlanta, but having a junior “partner” (wink, wink!) at its fortress hub since 2011 sure hasn’t hurt!

Separately, agree current & past data shows Delta enjoying a significant revenue premium over its legacy/network peers, United & American.

And while some Delta domestic flights taken last year were “old school” Delta at its very best (side note: most of which, interestingly enough, were aboard its regional affiliates, NOT mainline) & there were also several excellent customer service experiences at the airport (LGA, EWR, CLT & RDU come to mind) or using the app’s chat, the truly disappointing experiences were far too numerous & egregious to overlook (bald faced lies with customer contact reps online, on the phone, at the airport; repeated incidents of exceptionally bad treatment of reduced mobility passengers [family members I booked on Delta in the belief they’d be treated better than on other airlines] at JFK, BOS, DTW & Seoul/ICN airports; not just bad, but utterly inedible food on the Seoul-Atlanta Delta operated flight; forcing reduced mobility pax to walk up a very long, steeply inclined jetbridge in Atlanta before being seated in a wheelchair in a vestibule that links the terminal building with the jetbridge) are very serious deficiencies that not only suggest the airline’s revenue premium is more a reflection of what the airline used to be instead of how it actually is in the here & now, but is also noted in the hope that the airline & its senior managers are made aware of recently experienced paxex, and also as a “caveat emptor” (buyer beware) for others so they don’t make the same mistake I did believing the airline offered better paxex (on the ground & inflight) than others when they choose where to spend their hard earned money (for themselves & their loved ones).

I take no pleasure in being so critical about any airline, but especially one that in years’ past truly was consistently better than most of its domestic rivals as Delta was.

But, that’s the point, “WAS.”

Because while there are still occasional flashes of the “exceptional Delta” most of us fondly recall, the inconvenient truth is that the Delta of now is not nearly as consistently “good” as it used to be, and more and more brings to mind the bad old days of its long gone rival, Eastern during its years of decline, than the fondly recalled Delta of yore.

Especially when using the abomination otherwise known as JFK Terminal 4, which is every bit as horrible as Eastern’s long gone terminal at JFK used to be – except, perhaps, for privileged few who use the Delta One section for departures & then hide away in a fancy lounge until it’s time to board their flight. For them, Terminal 4 is probably less odious (as long as they overlook the filthy windows, dirty/sooty ceilings, walls & structural beams/columns, leaky ceilings & discolored ceiling tiles [especially in the headhouse], that is) than it is for most of us.

FWIW, I spent 2+ years (including much time on site at JFK) analyzing terminal facilities, operations, expenses & contractors’ work for British Airways [when it operated at Terminal 7] & Terminal One Group Association, LP [Air France, Japan Airlines, Korean Air & Lufthansa], among others – so I do have professional experience & a trained eye regarding the repair & maintenance/upkeep & how costly that is for the passenger terminals & cargo facilities at JFK!

thanks again for the discussion, greg.

First, Hauenstein has probably had more to do with defining Delta’s network than any person. and he didn’t come from NW which is counter to your argument about NW taking over DL.

DL didn’t invent along of things that are part of their strategy including building a hub in NYC (CO arguably built a hub at EWR before DL did) and CO also developed a pretty high quality product.

DL didn’t invent seat back AVOD but has it on more aircraft than any other airline in the world and is pushing to expand that to include free WiFi.

Execution is as important as coming up w/ ideas.

And DL has bested UA in NYC by managing to accumulate the most slots – not just in NYC but in the US – which also includes more flights to/from NYC including all 3 airports.

CO’s failure in NYC and UA only made it worse was by thinking too highly of EWR; it is a smaller airport w/ less runway capacity and can only do so much. Many people mocked DL’s 2 NYC airport hub strategy and yet DL hasn’t cut flights and runs a 15% larger operation than UA.

And the US-DL slot swap was entirely DL’s doing. No other predecessor airline had anything to do with it.

and UA’s vulnerability to DL in NYC is a product of both’s partnerships and aircraft. DL has overtaken UA as the largest airline from NYC to Latin America because of the Latam partnership which far surpasses what UA has in the region.

The A350 has greater range and will open routes including to Asia that UA cannot fly on its current 787s. They might pull more seats off and/or wait for Boeing to increase the MTOW of the 787 but for now the A350 in either version will do more for DL than what the 787 can do for AA or UA.

Nothing in life is static. What UA acquired from CO matters now as much as what DL acquired from NW. What AA, DL and UA and everyone else does w/ what they have and opportunities they see are what matters.

and, I think we agree that size translates into revenue premiums. The reason why each of AA, DL and UA have the revenue premiums in their hubs is because of their size; DL has simply looked at its entire business and is increasing its dominance in markets at a faster rate including by growing into markets where other carriers are strong.

*CORRECTION in above:

Eastern failed in January, 1991 NOT “1981” as mistaken written above.

Apologies for the “fat finger”/proofreading before posting error! 😉

Howard,

I would concur w/ most of what you wrote.

Delta has indeed gained because of other airlines’ weaknesses and has grown in spite of them. AA and B6 is the most recent example. being profitable enough and having the resources to grow when opportunities arise is key.

DL and WN have long been very well-run airlines. They, like AS, know how to do what each needs and to the extent possible, stay out of each other’s way.

It isn’t lost on DL, I am sure, that WN seems much more interested in BNA where DL is also growing but WN is certain to drop more routes from ATL as it seeks out better opportunities.

As for JFK T4, of course DL could wish they could take its CVG terminal or even the one in BOS but that isn’t possible. DL did what it could and continues to build. Unlike the Middle East airlines, US airlines have to work w/ the land airports have and the cost it takes to build terminals.

ATL and JFK WORK for DL; they aren’t cathedrals. I would argue few US airline terminals are anywhere close to great – DL at DTW would be the closest.

and I have never denied that DL’s customer service is not what it was pre-covid; neither are any other airlines and neither is most of the US. Some industries have come back but I enjoy fine dining more than ever because good restaurants and good service do exist.

My point in always talking about revenue whenever service is mentioned is because no product or service is any better than what people will pay for it.

DL, for all of the reasons discussed here and more, manages to get more for what it sells.

175 million customers aren’t wrong.

DL has a formula that is not an Asian airlines and it is not AA or UA or WN but DL does get better revenue across its entire network than its competitor.

The definition of premium includes a monetary valuation.

Thanks, Tim, for the kind words & your excellent rebuttal.

Fully agree with everything you said.

Following up RE JFK T4:

The terminal, especially the headhouse, is a disaster, be it the horrifically long lines to clear security (even with pre-check); the overworked, often surly staff; the abysmal treatment reduced mobility pax experience (exceptionally long, often ACA violating long [>30 mins], waits in a cordoned off pen for wheelchair attendants to arrive; whiney attendants who complain about the long distances between the headhouse & distant gates [as if the person in the wheelchair has any control over that!]); the shabby condition of the terminal with its dirty/sooty ceilings, structural beams/columns; dirty windows; leaky ceilings & stained ceiling tiles; stained floors & more that as the predominant tenant, Delta should demand better from the terminal manager/operator, JFK IAT, which is linked to Amsterdam Schiphol Airport via Schiphol USA, because the place is now >20 years old & sure is showing its age.

Agree, as the tenant Delta has less control than it did with its now demolished Terminal 2, which it managed (note: the City of New York owns JFK & LGA Airports; the Port Authority of New York & New Jersey [PANYNJ] leases the airports from

NYC & operates/manages them; the airlines or other entities sub-lease their facilities from PANYNJ) & considering its early 1960s vintage was in remarkably good condition until it closed 1-year ago after more than 60 years of use.

So, yes, Delta does not have a more direct control of JFK T4 like it does at LGA or did at Terminal 2, but surely it can & must demand a better state of repair & upkeep from its “landlord” (aka JFK IAT) because it’s dirty & terribly run down.

When Terminal 2 was still around, we actually preferred it over T4.

But, with all DL flights now operating at T4, we avoid it as much as possible.

We don’t expect JFK T4 to be as wonderful as Tokyo Haneda Terminal 3, Seoul Incheon Terminal 2 or Singapore Changi Airport are (although that would be nice, even welcome and appropriate at the USA’s “premier gateway” in a city that sees itself as the “Capital of the World”…), but the place is a dump & is desperate need of vastly improved security clearance areas, a top to bottom scrubbing & cosmetic refresh, plus far better ongoing repair, maintenance & upkeep thereafter for all passengers, NOT just the fortunate few who are quickly whisked from curbside to fancy lounges.

Hopefully once New Terminal One & Terminal 6 open later this decade, JFK T4 will feel obligated to update & modernize its rapidly aging facilities (especially the horrible headhouse).

But, why wait? The place is a dump already & is best avoided – which we’ll continue to avoid as long as it remains overcrowded & rundown.

Howard,

Delta is spending money at JFK T4 and would love to have the entire place to itself so it could at least make the final decisions but there are multiple non-DL partner airlines in T4 which also have leases.

Again, DL could not have built anything at JFK that could give it the size it needed to operate a 250 flight/day hub without spending tens of billions of dollars.

Let’s not forget that EWR is not exactly a shining star either. Neither is AA in PHL or UA at IAD. AA at JFK is a nice facility but as AA has welcomed a bunch of airlines to try to make the economics work for a facility that AA never used to its potential, T8 is not great.

DL’s Terminal A at BOS is probably the nicest NE terminal – and it isn’t even large enough to operate all of DL’s international flights – which is why DL is still talking w/ Massport about expanding terminal A or creating some behind -security connector between A and E.

US airports are woefully inadequate esp. when compared to Asian airports. I’m not sure why anyone bothers to try to compare them.

and again, DL is growing the scope of its network at JFK including w/ new flights to S. America that UA has not matched.

As DL adds flights from JFK to Asia and takes advantage of the A350’s range, it is certain that DL will gain even more advantages.

and I would agree w/ you that human service to passengers w/ disabilities is inferior to much of the world even though US buildings are generally as good as the rest of the world in accommodating disabilities.

Well, maybe I’m in the minority but I think they should charge for premium services. Because people have gotten used to try to get everything for free from not checking bags and not wanting to pay for it. So they’re gonna get free bagcheck at the gate. introducing basic economy tickets. Then complaining about no good seat. And not being upgraded, etc? If you want each of your 5 kids to bring on your own luggage. And not be smart and packing 1 bag for the family. Then you should pay that $500 to fly across country, stay home or drive.

I don’t really care what fees they charge, but my hard limit is not being allowed to choose my seat. For that, I’ll take even a more expensive flight with another airline.

I guess that’s the game- Delta makes its choices, I make mine.

Regulate the industry, nationalize the big national carriers

Remember…the best way to show you appreciate your customers is to treat them like crap!!!

Who said that? Delta AIr Lines said it.

OMG, the BS on here requires hip boots! Delta can claim they are a premium airline and charge accordingly. But that is their claim, and lately in my experiences, there is nothing about Delta that is a premium experience. The actual experience before, during, and after a flight, is no where close to a real premium 5 star carrier. Heck, my Delta experiences are not what they were prior to 2023 and I usually only fly Delta domestically.

But more to the point, Etihad, Emirates, Qatar, ANA, EVA and Singapore are premium airlines and fit that definition. Delta is not even close to those carriers,

@JohnB,

Absolutely agree – Delta has declined significantly compared to pre-2023.

It’s about the same as United (we stopped flying American 10 years ago) domestically, and after an especially bad long haul flight this past November (discussed in one of my prior reader comments above), will be avoided in favor of foreign carriers whenever possible going forward.

Well, I at least can try to make an on-topic comment……………….

I have no idea why anyone would sign up for a DL Sky Miles account when they can sign up to Flying Blue and be treated at least half-way decently.

It depends on how often you fly SkyTeam.

If you fly regularly, Flying Blue is good. I sometimes fly multiple times a year, but other times I’m flying other alliances and then their expiration policy is a pain. My choice is Virgin Atlantic because it’s miles don’t expire and it’s much more generous in earning than Delta. Virgin can be easier to earn status on than either Flying Blue or Delta depending on your flying pattern, or whether you have a Virgin Atlantic or Air France credit card.

@Jim Lovejoy

Flying Blue and Virgin are great programs, compared to Delta! Example: an economy award to AMS or CDG can reserved most times with Virgin or Flying Blue for 12k to 20k. With Delta, one is lucky to get an award to Europe, for 40k. That’s not including bonus point transfers. SkyMiles is NOT a premium FF program at all. SkyMiles is a money pit. That only has become worse each year.

This is why I have learned to travel with carry-on only – the cheapest way possible. Because the entire experience is being nickeled and dimed….so not worth it to fly anything other than basic. I can use the money saved at my destination.