I write frequently about the best credit cards. But for there to be ‘best’ there also needs to be ‘worst’ and we don’t shame those enough. These are the cards with unavoidable fees, weak or no rewards, and luxury pricing without real benefits to match.

Most of the truly awful credit cards have layer after layer of fees and are aimed at consumers with bad credit who may want to rebuild. But there are good products and bad ones within that market. There’s a special place, though, for the Luxury Card that charges you a $1,200 fee for less value than you can expect from a no annual fee cash back product.

Here are perhaps the 6 worst credit cards in the United States. Perhaps you know of othres that I missed, or maybe you even have one of these? (In which case, repent and reconsider!)

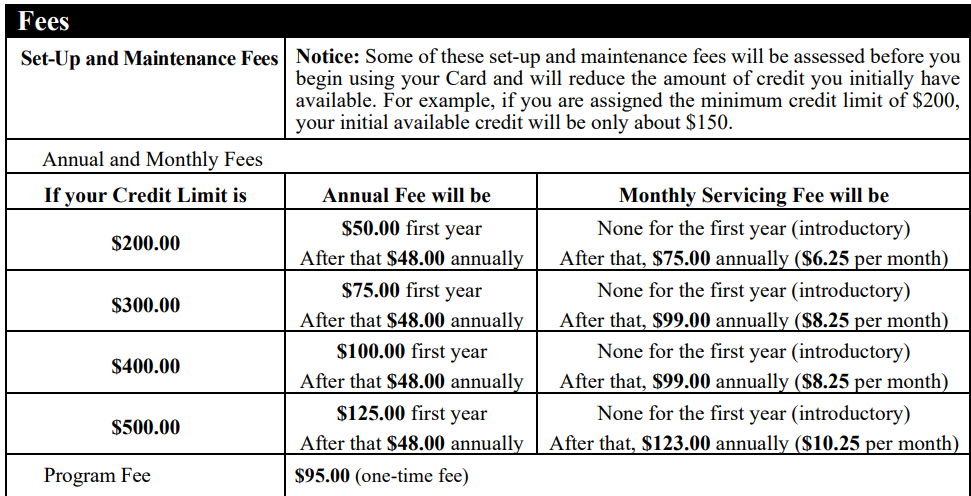

- Total Visa Rewards promises up to 11% cash back. Ok, sure. It has a 35.99% APR, a $95 program fee, first year annual fees that range from $50 to $125 (then $48 thereafter), plus monthly fees starting in the second year that total $75 – $123, depending on the amount of credit between $200 and $500 they extend to you. And if that’s not bad enough, the card’s setup and maintenance fees reduce your initial available credit. So you’re going to need to pay those off in full before you’re really even able to use the card.

- Revvi offers up 10% cash back ‘at select merchants’ and 1% on payments, a 35.99% APR, $95 program fee, first year annual fee of $50 – $125, then $48 annually, and monthly fees after year one of $75 – $123 annually depending on credit limit that runs $200 – $500. That credit can be reduced by the annual fee. There’s also a 25% credit limit increase fee after the first year.

- FIT™ Platinum Mastercard® I have to give credit to NerdWallet for finding this flaming pile of excrement – a $400 initial credit limit and a $95 processing fee before activation. That processing fee alone is about 24% of the initial credit line. There’s also a $99 first-year annual fee ($125 annual fee thereafter) and a $150 annual maintenance fee after the first year.

- PREMIER Bankcard® Mastercard® / offers credit limits “up to $700,” a $55 – $95 program fee, $50 – $125 annual fee, $0 – $10.40 monthly fee, and a 36% APR. Like the ones above, it is marketed as a credit rebuilding product, but the fees cardmembers are charged are exactly what’s standing in the way of actually rebuilding. Imagine paying a $75 annual fee for a $300 credit line, and that fee reduces the credit line.

- Reflex® Platinum Mastercard® maybe it should be called Reflux? A 35.90% APR, $125 annual fee, and after year one, a monthly maintenance fee of $150 annually for $300 – $500 limits or $120 annually for $750 – $1,000 limits. I

- Luxury Card™ Mastercard® Gold Card™ is the premium version of the worst possible credit card, with a $1,199 annual fee and $349 authorized user fee. Cardmembers earn 2x on airfare and hotel reservations booked through LuxuryCardTravel.com and 1x on other spend. It’s basically a $1,200 metal card with maximum possible 2% points value. No annual fee actual 2% cash back cards exist. But you get TSA PreCheck and a Priority Pass!

I don’t have an issue with cards that are meant for consumers rebuilding their credit. Those are going to be expensive, because overall it’s risky to extend credit to that group of customers.

And the value that you want to compare those to isn’t the top of the market, like a no annual fee 2% cash back card. You want to compare it to ‘this person’s reasonable alternative’. A rebuilding card can still be better than a check cashing store, and that’s important to remember when calling to regulate various forms of credit. Often consumers are picking the least bad option for them. You can’t regulate the need for credit out of existence so you just leave that consumer worse off.

But within that genre there are decent cards and there are ones I just would suggest to the most extreme credit rebuilding case.

For those types of cards you want to avoid an annual fee. You can often do that with a refundable deposit – you’re putting out a small amount of cash and borrowing against it. The card reports to credit bureaus as you pay it back each month. And it often has eventual upgrade path after you’ve demonstrated responsibility. The key is to avoid anything with program fees, activation fees, monthly maintenance fees, or an annual fee that’s large relative to the credit line.

Capital One has the Platinum Secured Credit Card and Quicksilver Secured Rewards. US Bank has Cash+ Secured Visa and Altitude Go Secured Visa. Navy Federal has cashRewards Secured. OpenSky Plus Secured Visa promises no credit check.

As for somebody that would consider a Luxury Card Gold Mastercard, well, all hope is probably lost for that person. They are easily in a position to do better and their mental model of value is simply inverted. Maybe they read too much Veblen and think that a high annual fee represents a status good.

Thanks for highlighting these. Interest rates like these need to

Be outlawed.

I’d be in favor of linking card rates to prime plus a few points.

That said. I haven’t paid any cc interest in over 20 years

Thot Leader: “Here are the worst cards; be sure to use my links!”

@1990 these are not my links. I linked to the cards purely as receipts.

@Gary Leff — Forgive me, dear leader…

@1990 — rofl!

I hadn’t heard of any of these before which is probably a good thing. Name ‘em and shame ‘em!

Oof. NYC-area thunderstorms. Safe travels, if routing through here tonight. @L737, I see DMV may be getting some too.