United Airlines has come a long way over the past decade. It was a real basket case under disgraced CEO Jeff Smisek, who was ousted in a corruption scandal. That carrier had sad aircraft, unhappy employees, and a shrinking route network.

Oscar Munoz was thrust into the role of CEO in 2015, and began to turn things around with employees. He gave them inspiration and a belief that the future was going to be better, and that made a difference in their interactions with customers. He signed off on real product improvements to go along with their new business class seat. And he hired Scott Kirby as President, who turned around their strategy.

United had shrunk its domestic route network, shying away from competition. They were running regional jets between places like New York and Atlanta. Kirby developed a plan to re-grow the network.

Wall Street analysts initially hated it, but Kirby was right and he kept explaining it. This growth was utilizing the assets they had better – it was cheap – and growth mattered because it made United more relevant in the markets they served beyond their hubs which would translate into credit card acquisitions and that meant making a lot of money with really high margins.

Then during the pandemic Kirby leaned into growth, announcing large aircraft orders and a product refresh that would make customers like flying the airline more. And he didn’t explain so at the time, but there was a plan to monetize the addition of screens (and later the introduction of Starlink internet) through premium targeted ad sales.

Against this backdrop United Airlines has become a more premium carrier, though it still lags in many ways. In the airline’s telling, though, they’ve already won. Aviation watchdog JonNYC reveals a set of internal slides from an employee presentation which paints the strongest picture for the carrier. United’s improvement is real, but the extent of it they present is misleading.

UA slides pic.twitter.com/LUY2ZKP6XE

— JonNYC (@xJonNYC) March 11, 2026

As you look throgh the slides, pay attention to United showing different base years in different cases. 2019 mades sense as the last normal pre-COVID year, and they’ve used that benchmark since launch of United Next as the benchmark for its target of about 75% more premium seats per departure by 2026.

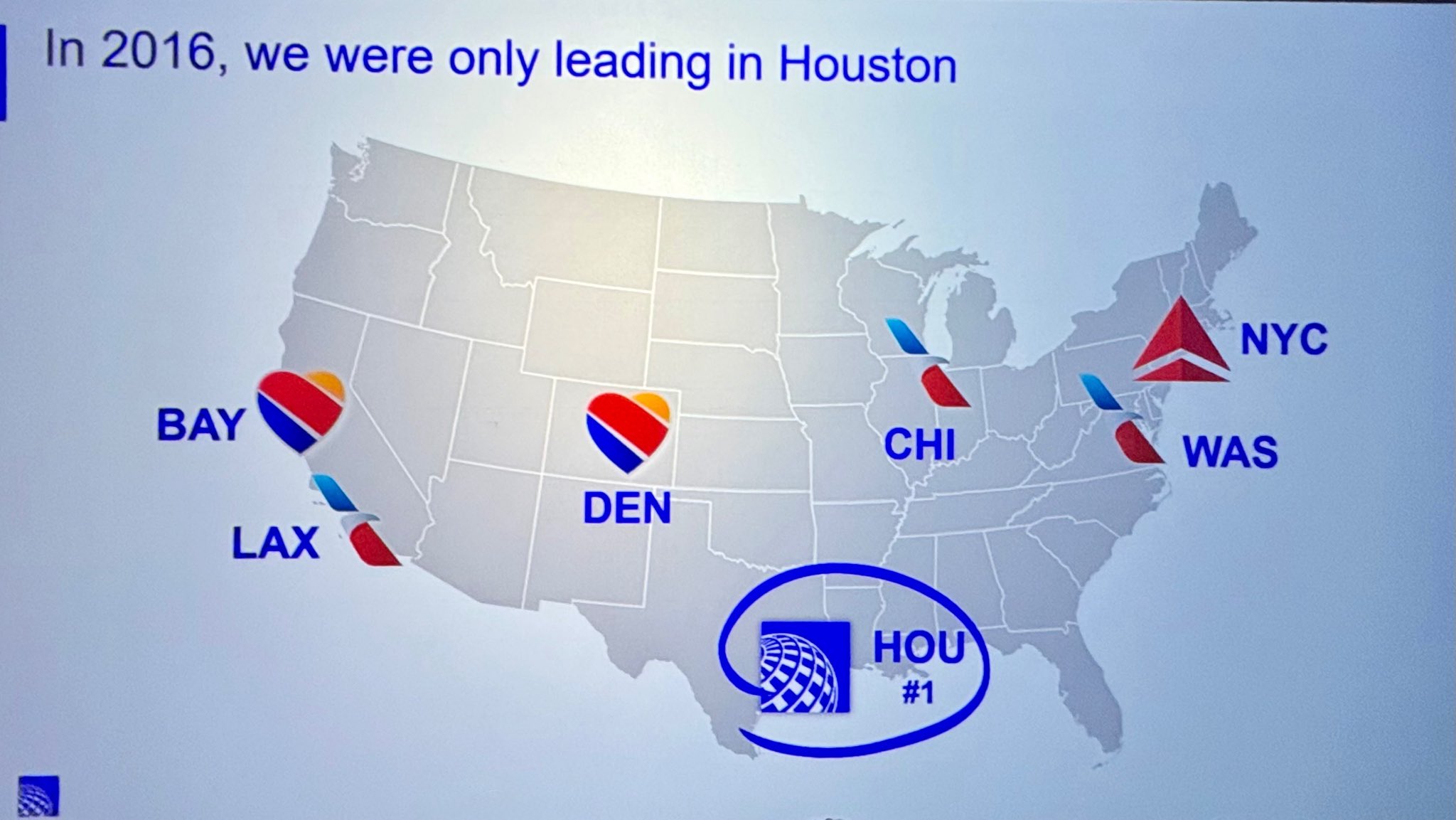

They use 2016 to goose the numbers. They had fallen to their lowest depths. They had cut 1,200 flights following the Continental merger. It’s also when Kirby started at United. It makes the before-after story look most dramatic, and also is most flattering for Kirby.

United Is Bringing On A Huge Mainline Fleet

United really does have an enormous renewal program. At the end of the year their firm order book included:

- 150 Boeing 787s

- 270 Boeing 737 MAXs

- 119 Airbus A321neos

- 50 Airbus A321XLRs

- 45 Airbus A350s (pushed to after 2027, they remain a question mark at best, and note that the slide omits these)

United Next anticipates more than 630 new aircraft deliveries through 2034.

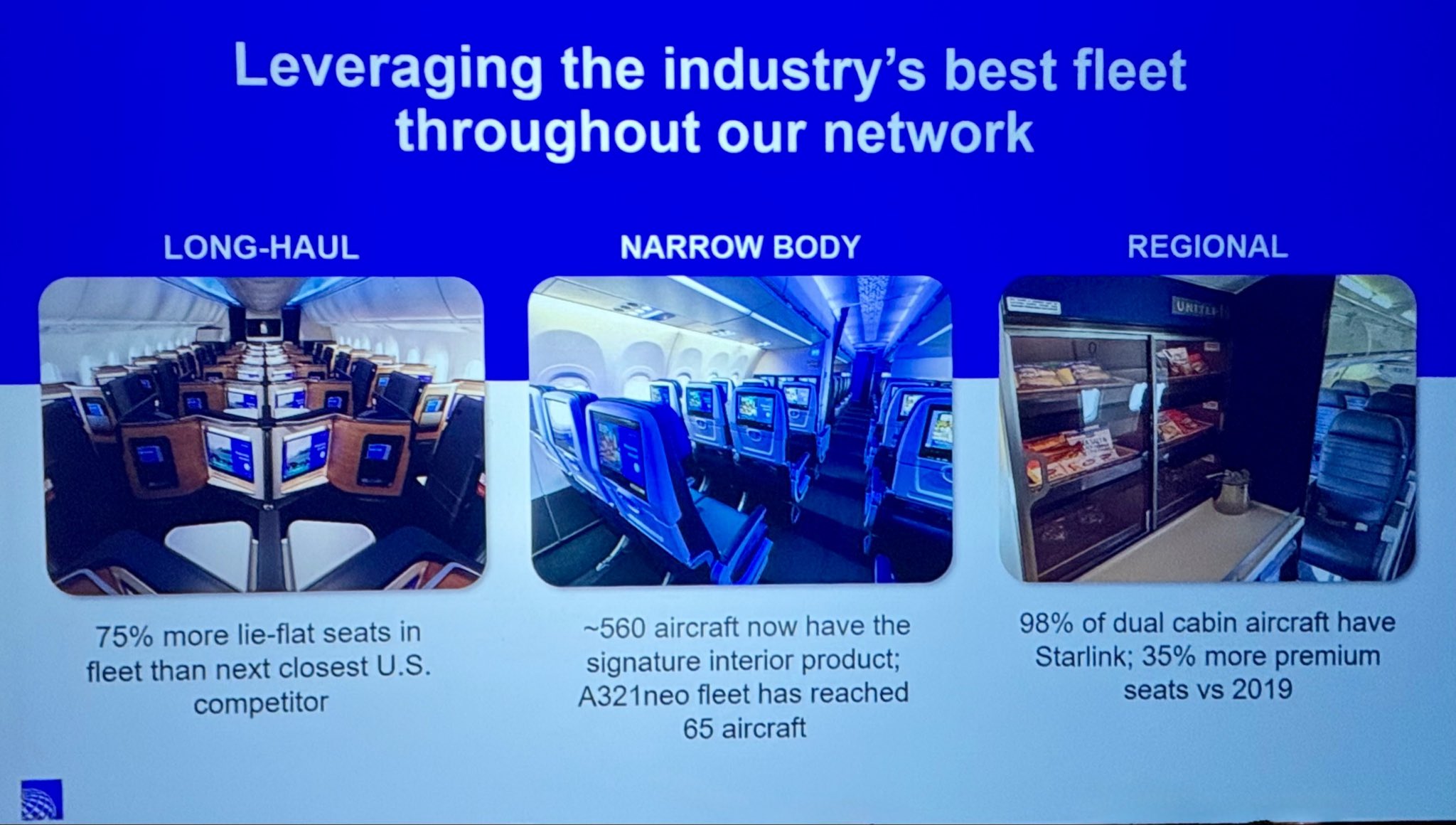

United Exaggerates ‘Best Fleet’

The announced plan in 2021 was to increase seats per domestic departure by almost 30%, replace at least 200 single-class regional jets with larger aircraft, and raise premium seats per departure by roughly 75% by 2026. A lot of what the deck presents as network strength is really upgauging of aircraft. There are fewer tiny regional jets, more mainline seats, and more premium seats per departure. That’s not the same thing as share gain!

The “industry’s best fleet” slide is mostly a slogan. They exceeded 530 new or retrofitted aircraft in their signature interior in 2025, and last month said Starlink was already on most of its two-cabin regional jet fleet (more than 300 aircraft). That’s good, but its Polaris business seat lags.

That seat was mid when it was introduced in 2016, signed off on in the cost-cutting Smisek era as a way to squeeze lie flat direct aisle access seats into the same cabin footprint as the old six-abreast business cabin on a 777. With the seat you no longer needed to book away from United, but American’s is better and Delta’s non-767 fleet is better too. Their new Polaris seat with doors will thus far only show up on new planes.

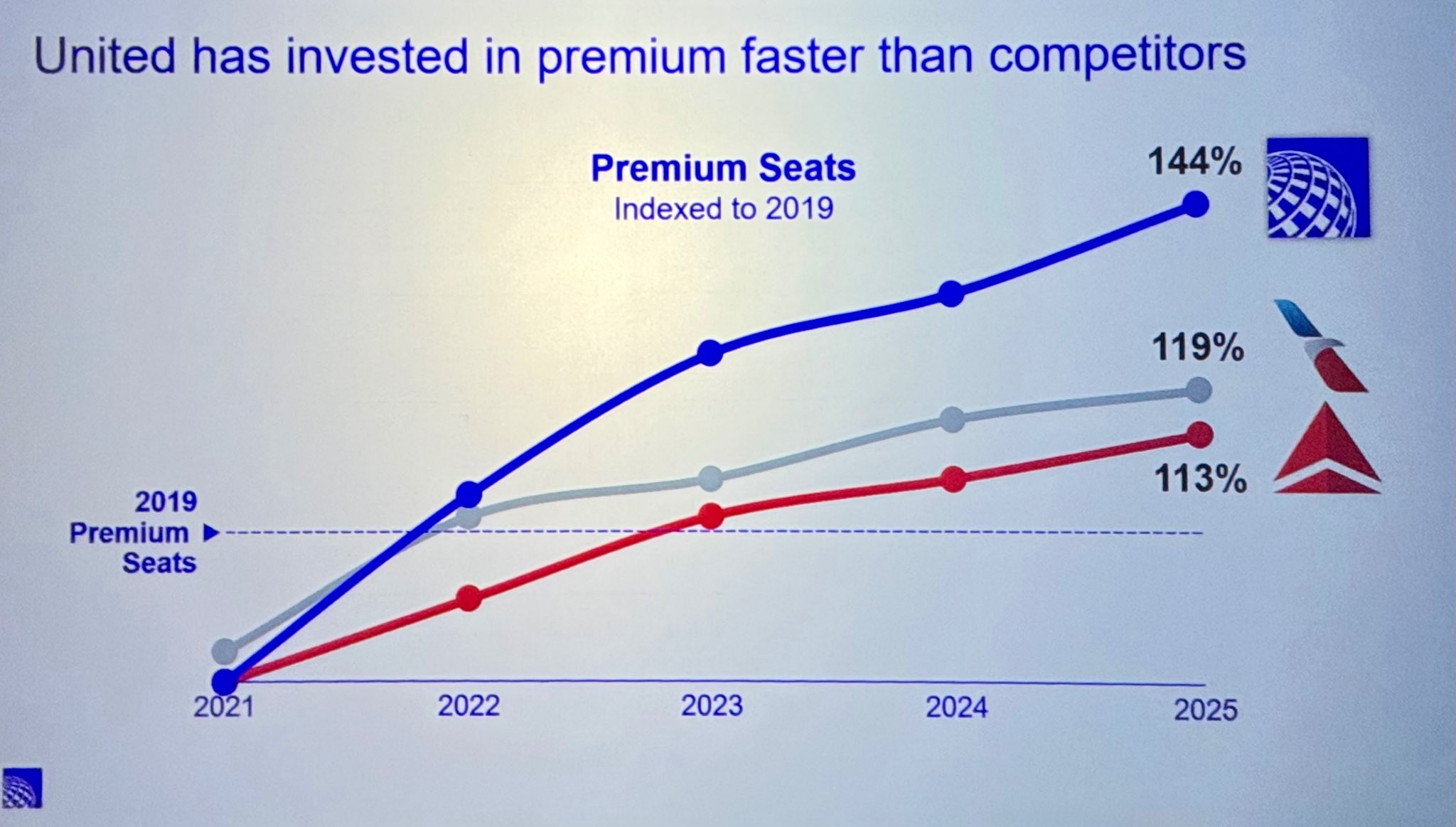

What Does It Mean To Lean Into Premium ‘Faster Than Competitors’?

United in many ways started off ‘less premium’ so talking about rate of increase from a low base isn’t meaningful, though they’re reaching a point where they do have a lot of premium seats (including extra legroom coach) on offer. But premium seat growth ‘faster than competitors’ is really a timing issue.

![]()

Nearly all 2026 Delta seat growth is premium. American is just now growing its premium cabins. United’s slide doesn’t mean they’re ‘more premium’. Just ask anyone that’s eaten their long haul meals.

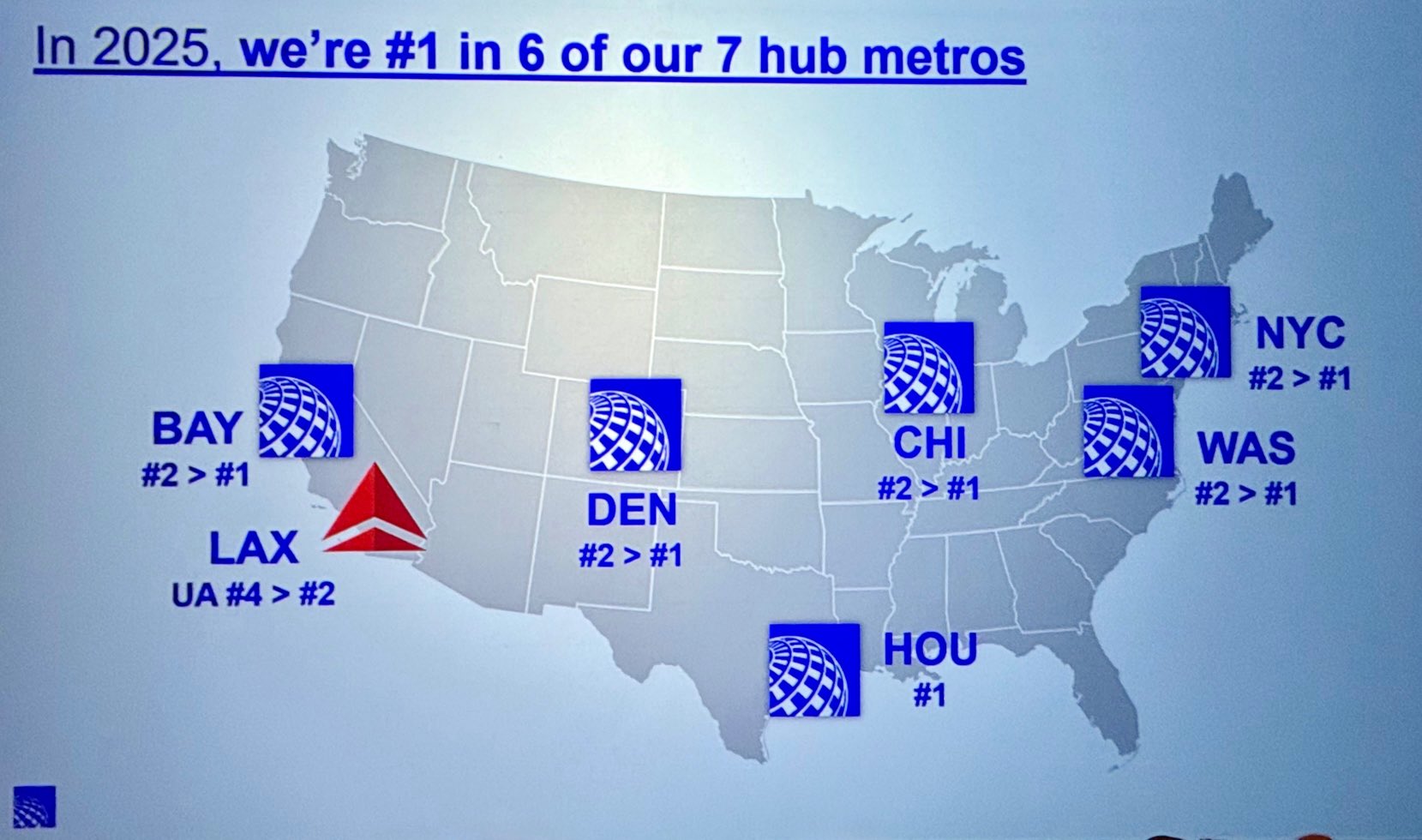

Is United Winning At Nearly Every Hub?

Where things feel most stretched is the claim about being number one in six of 7 hub markets. They’ve rebuilt scale in several cities, but…

- Newark isn’t the same market as New York LaGuardia and JFK, sorry it just isn’t, and Delta is seen more as ‘the New York airline’ – but Delta is at slot-constrained airports while United only now wants slot restrictions back at Newark to keep out competitors.

- They were already number one in San Francisco, they call it ‘Bay Area’ to make it look like there’s been improvement

- American has pulled back in Los Angeles, and that’s a big piece of the United change there. American also retired too many planes during the pandemic and didn’t have the aircraft to regrow in Chicago after the pandemic. United was already number one there in 2019, but it’s American’s stumbles rather than United’s success that’s widened the gap.

- United has grown at Washington Dulles, which they’d ignored for years, and American Airlines can’t really grow at Washington National because of slot restrictions and runways that don’t support widebodies. They’re also different markets.

- Meanwhile, they’ve invested in Denver while Southwest and Frontier has struggled. That’s a strong connecting airport, but it’s still Denver.

What United Leaves Out

There’s a glaring omission from these slides. The biggest driver of industry profit is cobrand credit cards. And while United improved its card deal in 2020, still lags Delta and American in deal terms (though has surpassed America nin card spend). They recognized $3.2 billion of other operating revenue from partner agreements including the Chase co-brand deal last year. They’ve shifted to give a few more miles to cardmembers while charging non-cardmembers more for awards in an attempt to put more cards in wallets, though interestingly with no requirement to actually spend on most of the cards.

United’s domestic buildout has improved the airline’s relevance. They’ve gone more premium. They’re more attractive to potential credit card customers. United has improved more than any other U.S. airline over the past decade, hasn’t replaced Delta as the country’s premium carrier though it is clearly the leading U.S. flag carrier, and American continued its slide until a year ago.

WHAT?! Deceptive practices?! By a US corporation?! United?! Naw…

Meanwhile over at DAL: Let’s give Ed $100 million in stock incentives… also, raise prices 200%!

Southwest has dramatically reduced its schedules in California, especially Oakland, since 2016. Southwest’s recent policy appears to be to increase captive market fares and then decrease frequency as customers stop buying. This is why United’s relative position improved in the SF Bay Area.

If I tell anyone in my family to come pick me up at Newark they will laugh and tell me to enjoy Jersey.

Very accurate, Gary.

and the simple fact is that AA underspent on developing its product while DL started spending on product right out of bankruptcy so, of course, DL doesn’t need to spend as much per year.

It is not uncommon for airlines to win in their hubs; DL does the same thing in 7 of its 8 metro areas. But AA, DL and WN also are the largest in dozens of additional cities other than hubs, something UA is much less able to say.

and UA’s massive fleet spending could well bite it in the backside this year and beyond as they and the rest of the industry having to absorb billions in additional fuel costs.

UA uniquely has to absorb labor cost increases that the rest of the industry has already taken on.

Not to speak of the capacity they will have to pull from their system because this much growth just doesn’t work when you are also trying to raise fares necessary to cover fuel costs.

you do have to wonder what UA analysts and execs do all day long and it is clear that figuring out new ways to pat themselves on the back is a big part of their meaning in life.

this is the kind of stuff that I look forward to from Jon… there are clearly people at UA that think it is worth their while to leak it to the world

@Tim Dunn — Who is Jon (Galt)?

I’m guessing Jack’s family isn’t going to the airport to pick him up no matter which airport he uses.

@Tim Dunn: Long ago, a colleague said: “When things are good, everyone thinks the good times won’t end. When times are bad, everyone thinks the bad times won’t end. Neither case is true. Almost everything goes in cycles.”

Fuel costs are cyclical. They are above the trend line because of short term issues in the Middle East.

But aircraft orders are long term. So the question is whether fuel costs will revert to the mean (or below) before the planes must be paid for.

@Gary: No one ever made a profit long term in the airline industry following the analyst herd. WN is merely the most recent casualty of the Wall Street analysts.

Oscar Munoz did a great deal of the heavy lifting but that somehow keeps escaping Kirby’s mention.

@Gary Leff

I think it’s silly to not include EWR in the NYC analysis since United is actually competing (and frequently winning) on long haul from EWR, which means they are getting customers from NYC. Not just NJ.

That being said, United’s graphic is wrong in WAS. Southwest is the biggest if you combine all three airports. You can’t really include Dulles and omit BWI in the DC analysis.

Additionally, United’s graphic just says LAX, but if you actually look at the greater Los Angeles area, Southwest is the biggest airline and is probably the only airline making money in LA.

@John H EWR is inconvenient unless you live in lower Manhattan or Staten Island. JFK and LGA are closer and have less traffic than EWR. United’s marketing is picking whatever they want to make themselves feel better. However, Kirby knows EWR isn’t NYC so that’s something.

@Jack — If you live in lower Manhattan, all three major area airports are somewhat ‘convenient.’ If you’re like Gary, and can leverage your BILT relationship to fly Blade to EWR or JFK, even better. United has those timers on the yellow Taxi in NYC, showing 24 minutes to EWR, 45 to JFK, which, unless there’s no traffic, is laughable, but yes, usually EWR and LGA are closer than JFK from Manhattan.

@Tim Dunn — I meant to mention, unrelated, but, well done on Delta ditching 717 for EWR-MSP; it seems mostly a220s nowadays. Woot!

lawyer on the couch,

the problem for UA’s huge capex during a high fuel cost period is that UA’s plan had been to use all of those new airplanes to grow.

With high fuel and the need to cut capacity, UA will be taking on a lot of new aircraft – with the cost associated – with little revenue growth above costs. and the chance is that UA’s debt will go up as it takes these massive orders which are a combination of what they were supposed to get years ago but Boeing keeps rolling as well as what is on the books to be scheduled this year.

UA has lived like the good times would never end and could face a much harder landing than the rest of the industry as the bottom falls out this year.

(Selectively) Worst to First (Again, Sorta)

We’ve all done it with fish pics, right?

Grammar

Can I buy you a subscription to any sort of proof reader vs. gettting a Citi Strata card?

@Gary Leff, if you are going to have a go at United exaggerating best you check yourself.

United’s Premium seat graphic clearly states Premium SEAT… and you want to query the meal product to devalue the claim?! You know what the graphic data relates to. BTW, the meals in Polaris have improved considerably. Took way too long but greatly improved now.

JFK sucks ass for those of us outside of the immediate metro area. The issue for United@EWR is getting connecting flights from smaller regional airports.

@ Gary – You and Jon do not know the context or when the slides were used.

Those slides were presented at an annual training meeting in DEN the first week of Sept 2025, so quite a while ago. The target audience is many of the managers at the DEN training center, as well as the pilots who train and check the other pilots. I would describe them as generally more company-friendly, and many of the managers as company Kool-Aid drinkers. The executive level knows that what they present will be well received, and people will clap. The questions will be softballs, mostly as they say. They were presented as saying, “Since we, the current executive team, took over here, this is what we have done for you.” It was not to present for a financial purpose or at a public venue, though there were probably 1,000 employees in attendance; no other employees were shown this anywhere that I know of, only in DEN.

After stating that and with over 30 years at United I will say that mostly what Kirby has said is right, he seems to be the smartest UAL CEO in the last 30 years, wants to be the biggest airline, seems to really hate AA which is understandablele but weird since I would guess he would still have friends there and he seems to really want to run an airline not just make a buck and get out.