I’ve known that Citibank was working on a refresh of its American AAdvantage small business card, but we finally have some concrete sense of what they’re thinking.

Here’s a product being surveyed by Citibank as a refresh of their American AAdvantage small business card. This may not be the final card they come up with, although I’d note that when they surveyed a refresh of their premium AAdvantage Executive card the survey I wrote about was very close to what was ultimately offered.

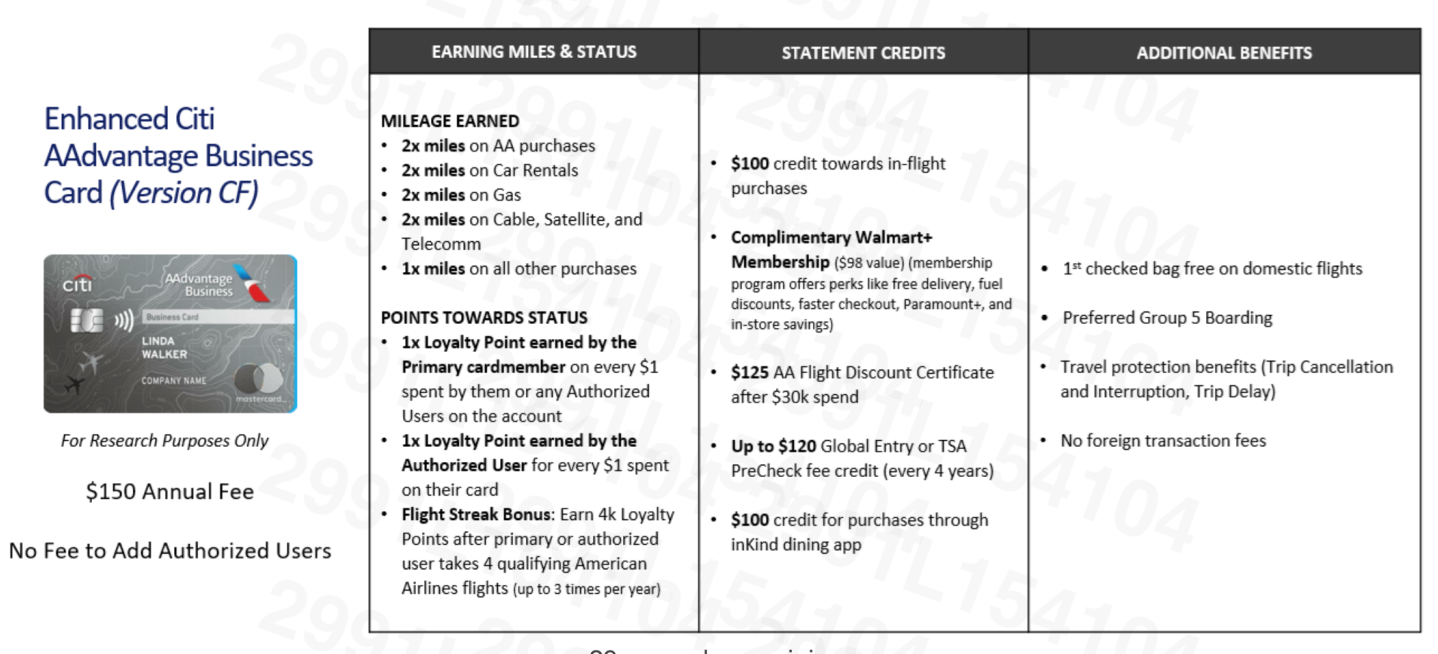

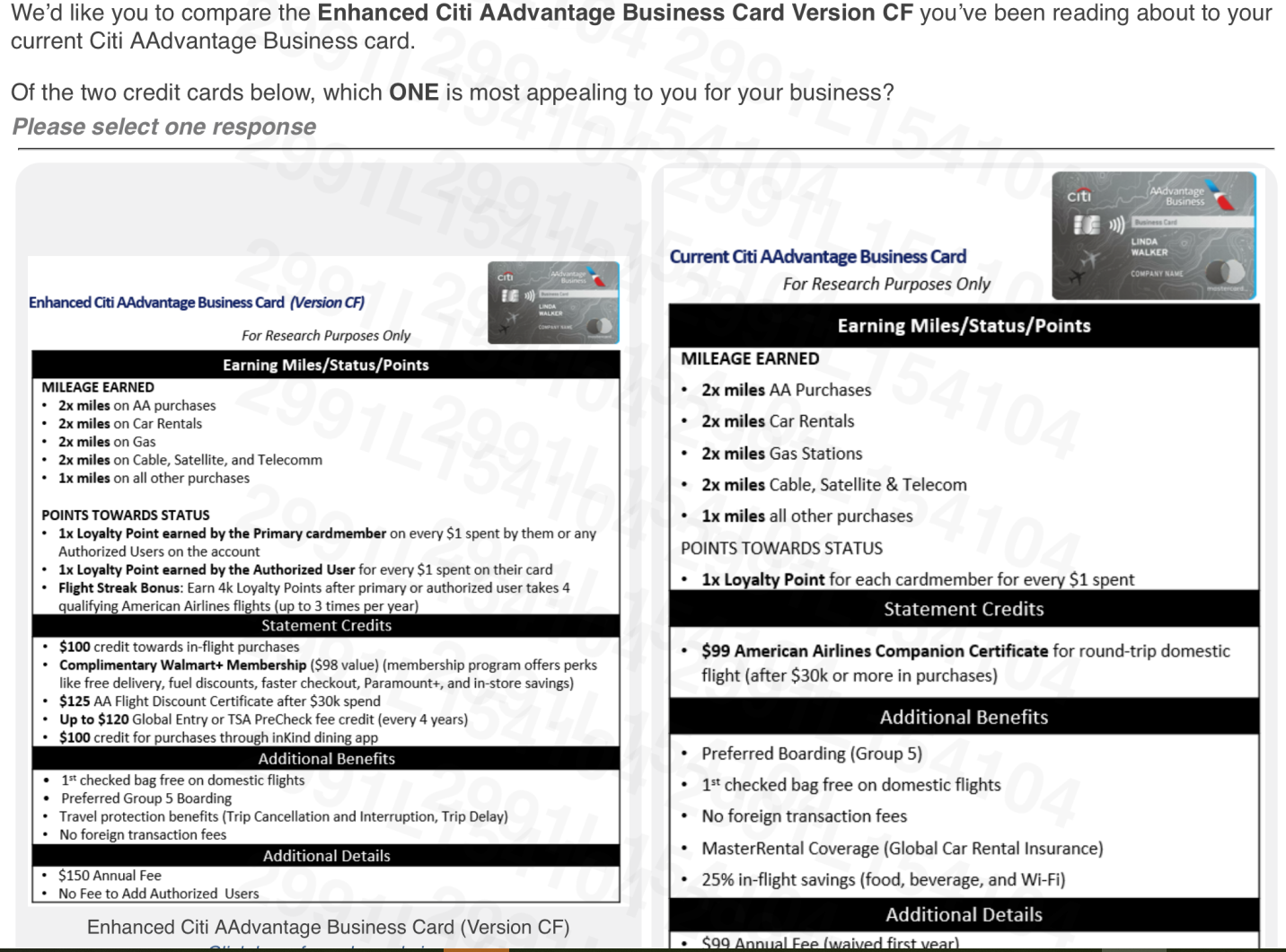

The thinking here is a $150 annual fee card (vs. the current $99), positioned along the same “$150 business mid-tier” lane as the United and Delta cards, where the marketing story is “fee is offset by credits.”

It replaces the current $30,000 spend benefit of a $99 companion certificate with a flight discount certificate. In the survey they A/B test the discount amount ($125 / $200). The companion certificate has high upside if you use it well, but restrictions are annoying. The discount has a smaller upside but is simpler.

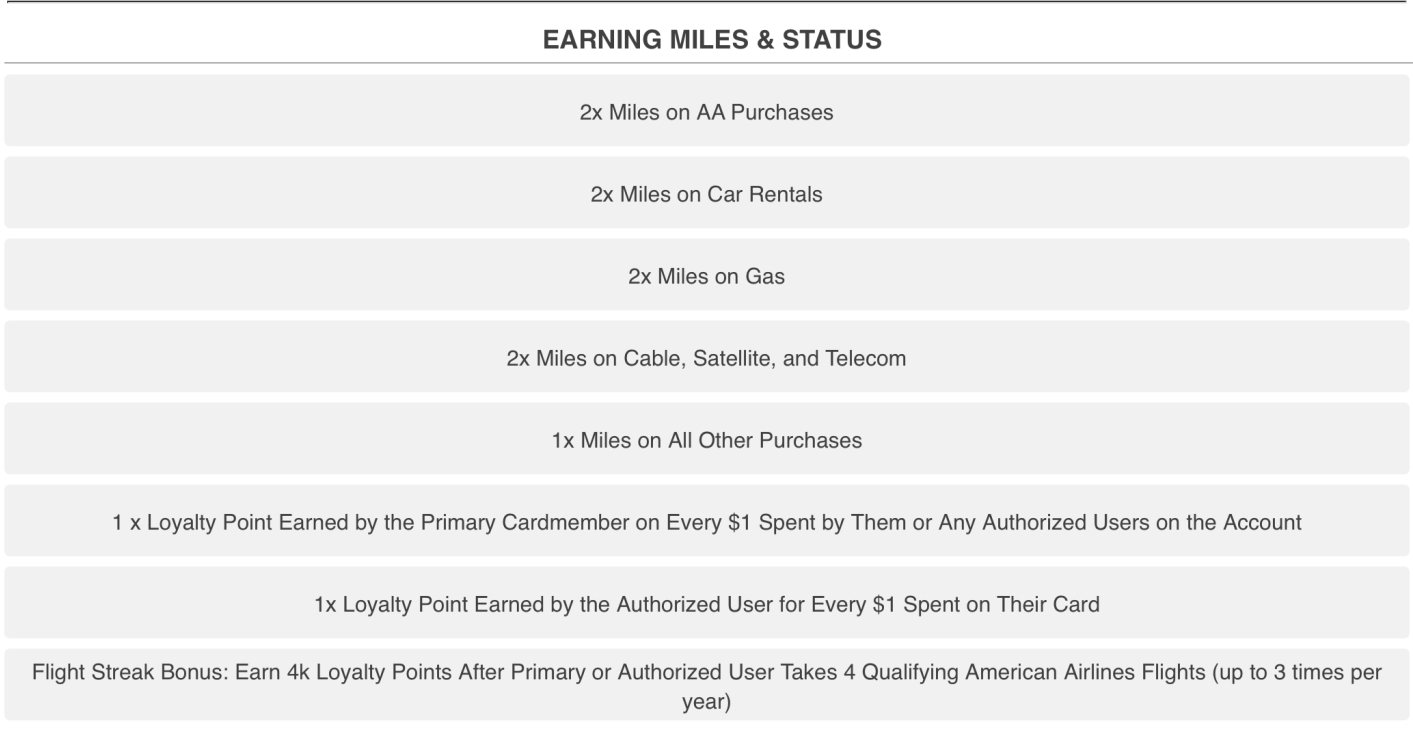

Earn in this example is 2x miles on American Airlines purchases, car rentals, gas, and cable/satellite/telecom and 1x on everything else. But the real benefit is that it earns one Loyalty Point towards status both for the primary cardmember and for the authorized user when the authorized user spends money.

And it would add a ‘Flight Streak bonus’ similar to what the new mid-tier consumer Globe Card provides: 4,000 Loyalty Points after 4 qualifying American Airlines flights, up to 3 times per year (so up to 12,000 Loyalty Points per year).

Statement credits:

- $100 in-flight purchases credit (but American doesn’t sell enough food on board for this to be useful in my opinion)

- Complimentary Walmart+ membership (‘$98 value’ and of course comes with Paramount+) along with Global Entry/TSA PreCheck credit every 4 years

- $100 credit via inKind dining app

Other benefits are first checked bag free (domestic), Group 5 boarding, and travel protections (trip cancellation/interruption and trip delay).

Survey participants were asked which of the following features they valued. Personally I think the last three are what drive value to the card, since other products earn rewards for spend faster.

My key takeaways:

- The would make Loyalty Points-earning for both the account owner and the authorized user for the same spend a permanent feature of the card – not temporary and not targeted. So my wife gets the card, I am an authorized user, and my spend earns status for both of us.

- Adding ‘Flight Streak’ like they offer for the new mid-tier consumer Globe Card with 12,000 bonus loyalty points for 12 flight segments is strong new value.

- And there are some decent statement credits potentially, like a $100 InKind dining credit spendable at over 5,000 restaurants.

This all strikes me as more than worth the $51 increase in annual fee, in addition to the $99 annual fee which opens up redemptions in the AAdvantage Business program, where you earn small business points in addition to the miles from your flying and where you earn an extra loyalty point per dollar spent on tickets that you tag as business trips.

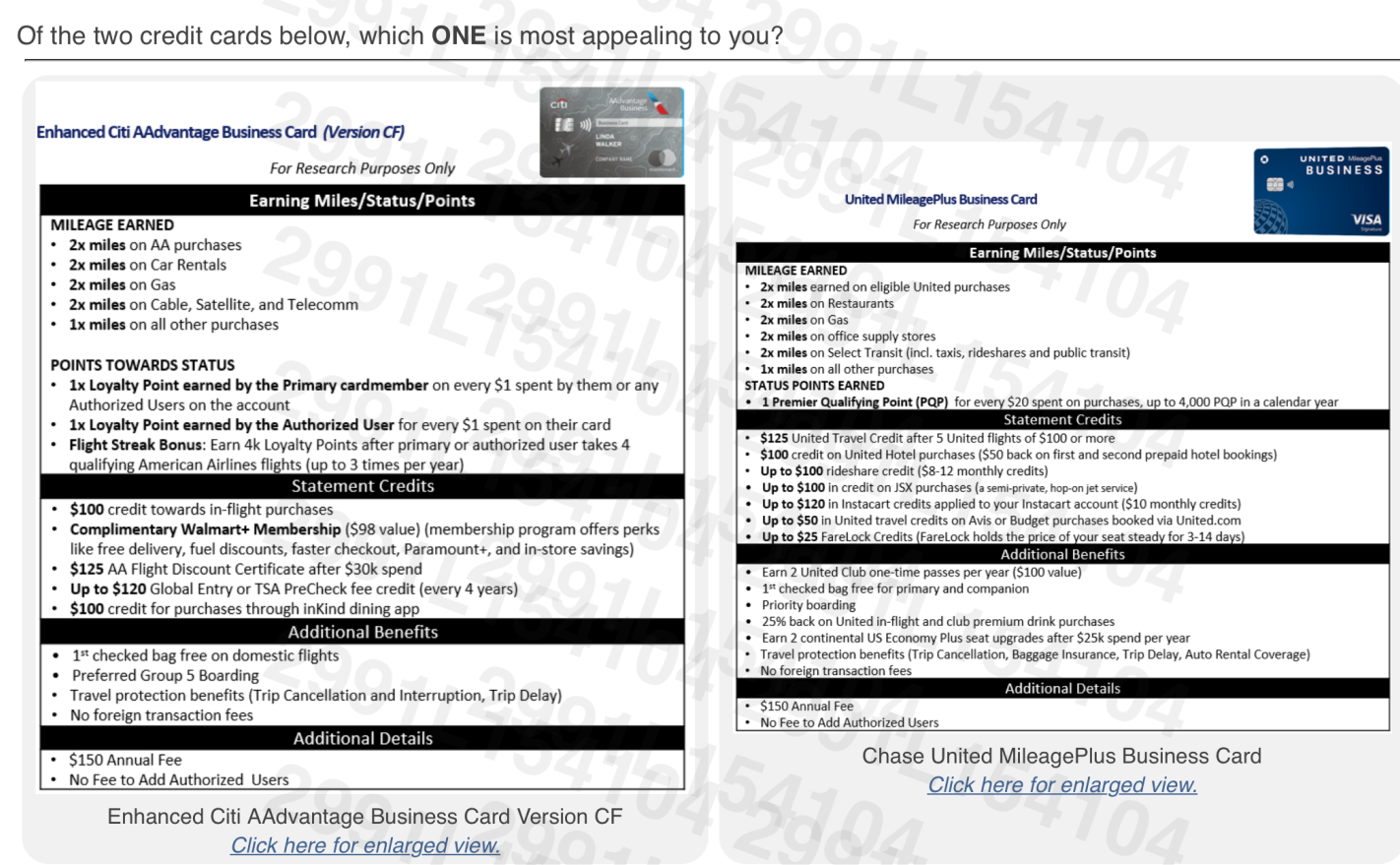

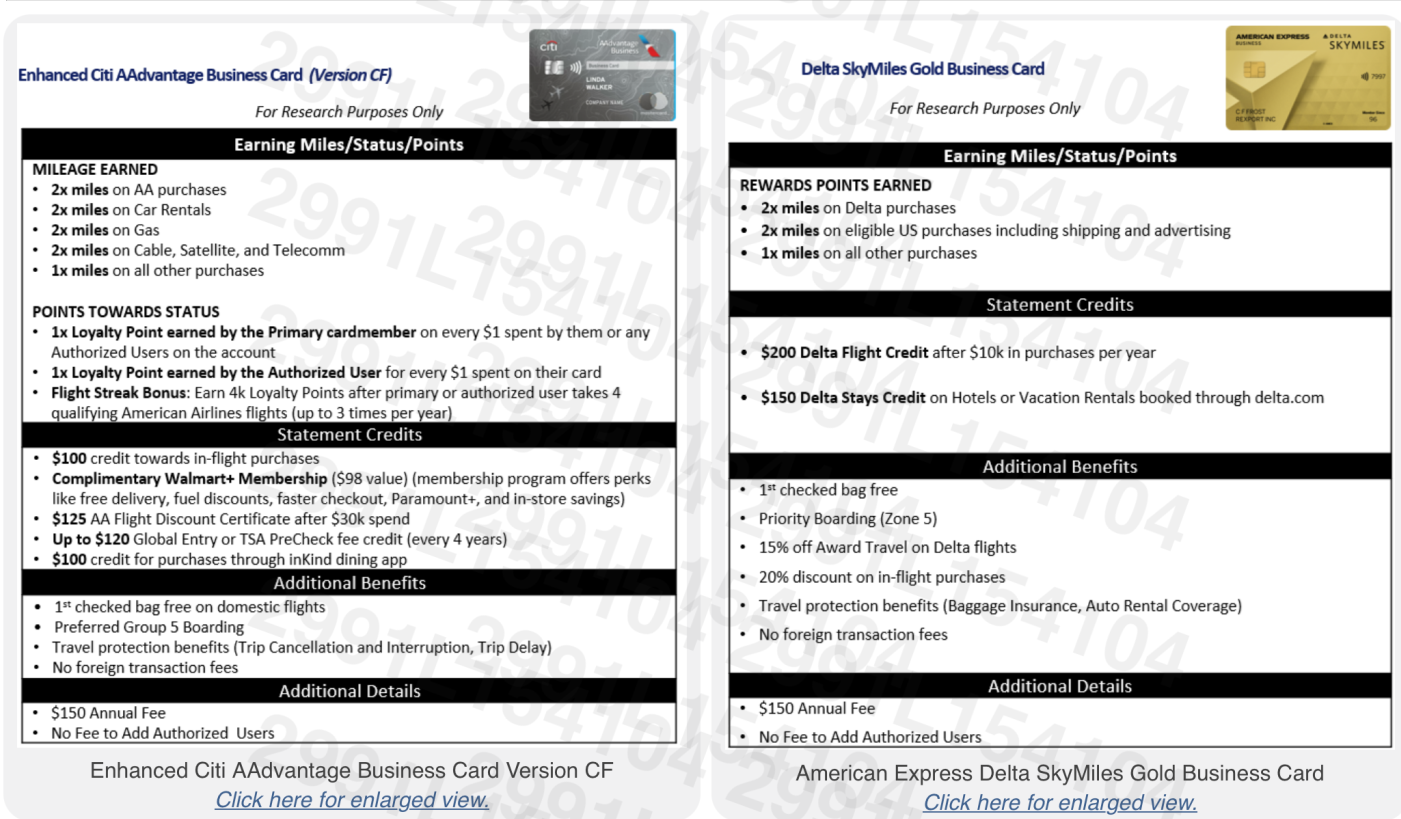

During the survey, customers were asked to compare the proposed card to the United and Delta small business cards, though I’m not sure that’s the right point of comparison. For many people, they’re considering a cash back card (or some other card) and the small business card of their preferred airline – rather than going out and comparing airline cards. A Miami-based small business owner isn’t going to think well, I like the credits on the United business card.

Surveyed customers were also asked to compare the new product against the existing one.

This is one of those rare cases where a product actually looks better for its target market than what’s offered today, even with an increased annual fee.

(HT: Robert)

*yawn*

“$100 InKind dining credit”

*burp*

$51 extra dollars in annual fee

*fart*

Would the flight steak bonus stack with the one that comes with the Globe card?

I got that survey. They compare it to a United card and another AA card with a bunch of coupon crap. Seems like they might considering doing some lounge passes like the United card.

@ymx — Flight… steak? Or streak? If it’s steak, I’m slightly more intrigued!

I saw a survey with a different set of offers and a higher price point.

More coupons, one with a companion certificate and one without, but more coupons.

Was this card custom designed for OMAAT?

In defense of comparing across airlines, this may be a signal of going after high spend markets like New York, LA, and Chicago.

Not useful for Charlotte or Miami, while DFW and DC is a bit more useful (DFW for Southwest, DC for United).

I wonder if they used the owner location as a pre-requisite for comparing across regions. Like you mention, not useful for Miami, but definitely useful at a fair number of other hubs or key markets.

Full disclosure: I’m a market researcher, so trying to figure out their logic for why they are asking this.

As a lifetime Platinum and Prestige card holder, this has exactly zero value. I will be dropping my card. But the SUB was appreciated

Oh great, some crappy coupons in exchange for a 50% cash increase in the annual fee. No thanks.

I would love this update. Our business already pays for Walmart+ so that alone really helps. I love the idea of permanent LP earning for authorized user spend and also the flight streak addition really sounds great. I’m all on board for this! They just need to make it easier when adding an authorized user for the business card to be able to add the employees AAdvantage number in when signing them up. It’s a mess right now with all of our employees being assigned random AAdvantage account numbers when they already have their own accounts because Citi doesn’t allow you to input it when you add them to the card.

Why not remove telcom and another business specific category or just it:) Not very robust for a travel card TBH. Add rideshare, hotel status, or car rental insurance. My other Visa issued cards have WAY more benefits. Hopefully they will go back and modify this configuration to be more business. Where is lounge access? I travel a lot and use the lounge for calls. All this means is I have to keep my consumer card for my business. What’s the point of bothering to apply for another card? Glad they are trying, but this needs some new eyes/approach on the benefit configuration.

“Let’s double how many people have status through card spend!” Great.