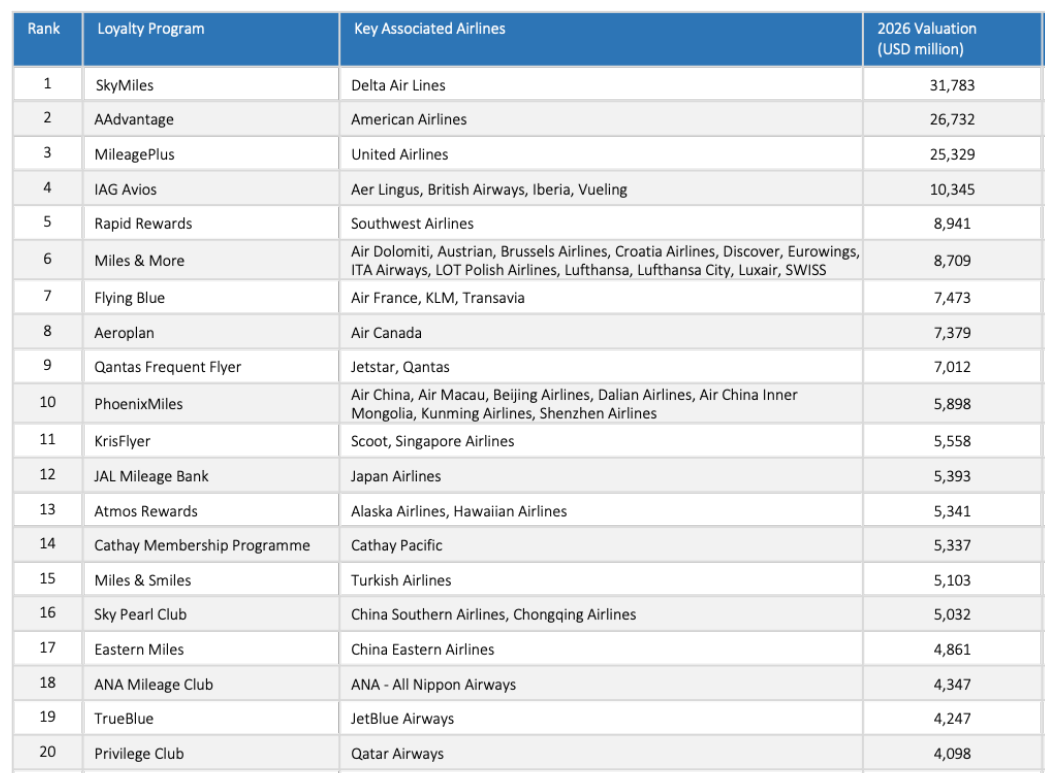

A new consulting report values the top 100 airline frequent flyer programs. It pegs Delta SkyMiles number one, worth $31.783 billion and American AAdvantage number two at $26.732 billion.

What’s so striking about these numbers is that the entire market cap of American Airlines is just $6.72 billion including its frequent flyer program.

Financial analysts and the general public have come to realize that airlines are no longer just ways of moving people from place to place. They’re credit cards with wings. (American does have significant debt backed by AAdvantage.)

- Some carriers often lose money just flying people and cargo alone (American Airlines)

- Others may make money flying, but make the bulk of profit from their bank partner (Delta)

- And in any case, frequent flyer revenue is very high margin (39% – 53%, depending on how the airline does their internal math)

United’s MileagePlus valuation at $25.329 billion isn’t quite as dramatic as American’s – United’s market cap slightly exceeds this figure at $27 billion.

There’s a big drop to IAG Avios (British Airways, Iberia, Aer Lingus etc.) at $10.345 billion. The rest of the top 10 are Rapid Rewards, Miles & More, Flying Blue, Aeroplan, Qantas Frequent Flyer, and PhoenixMiles.

On Point Loyalty says the average program value is now $2.4 billion, up from $2.0 billion in 2023 with 62 programs rising in value, 21 falling, and 17 entrants like IndiGo BluChip worth $534 million.

In a ‘bigger than a breadbox’ rough directional sense the rankings largely make sense. The US big three airlines have the most valuable programs, coalition loyalty programs and the strongest non-U.S. franchises are valuable. But I wouldn’t over-rely on the specifics.

On Point says it analyzed more than 170 airlines and used 50-plus variables to estimate the value of each program. The model estimates pro forma Adjusted EBITDA, applies an adjusted multiple, with the valuation assuming a minority 10-49% stake sale or IPO backed by a long-term agreement with the airline.

I’m not sure that actually makes sense – we’ve seen how spinoffs with long-term agreements actually do in practice. Air Canada had to buy their program back, because the bad incentives between them and Aimia made it impossible to service loyal customers or to effectively grow the value of the program.

These programs also used to be overvalued based on spinoffs because most that have actually happened were Etihad using loyalty programs as a workaround to control an airline without running afoul of foreign ownership restrictions.

Still, it’s notable that the top 3 airlines here account for about 35% of world frequent flyer program value, the top 10 about 58%, and the top 20 almost 79%. So this is really a suggestion that a small number of giant programs are value and that there’s a very long tail. The big loyalty programs in the U.S. are the most valuable because of

- scale

- unregulated interchange

These programs are valuable because they deliver the best premium motivated customers to bank credit cards.

Delta reports that American Express revenue was $8.2 billion in 2025. Qantas Loyalty reported FY25 EBIT of A$556 million. IAG Loyalty said 2025 operating profit before exceptional items rose to £469 million/€548 million.

There are some challenges with the report:

- It gives the illusion of precision giving rankings and dollar values down to the million, but doesn’t disclose the data they’re using for each. In fact, the presentation is more precise than the underlying method supports. I wouldn’t take the difference between number 13 and 14 literally.

- It is not valuing “pure loyalty.” The methodology includes airline financial health, home-market GDP growth, political stability, and investor friendliness. These might factor what an airline could get in a spin-off, but doesn’t tell you which program is the better operator or even which has more valuable customers or current revenue performance.

During the pandemic, American, Delta and United each raised between $5 billion and $10 billion in debt backed by their frequent flyer programs. American had AAdvantage appraised six years ago at between $18 billion and $30 billion. So we do wind up with order of magnitude directional correctness here.

Bear in mind that this is also not a ranking of the best consumer programs. Delta SkyMiles! It’s a ranking of who’s monetizing their business best. United’s cobrand deal isn’t as lucrative as American’s or Delta’s. Delta benefits from American Express having lost Costco a decade ago and renegotiating with unprecedented terms to lock in the partnership.

And credit card deals aren’t just the profitability engine of airlines, they now drive where airlines fly. Delta shared in October that a big reason for their expansion in Austin is that it’s such a fertile area for them to sign up high spending American Express customers. But this isn’t new and isn’t just Delta.

- A key reason Southwest went into Hawaii (and also why they need premium products, international and partners) is to drive cobrand spend. Cardmembers need aspirational destinations to motivate them to get the card and keep it top of wallet.

- When Scott Kirby joined United he laid out card acquisition and spend as a key rationale for restoring the airline’s domestic route network. He argued that being number one in a market produced outsized credit card uptake, and that relevance in a market was needed to generate card spend. And we’ve seen some of the ‘sexier’ routes United has added clearly supported by aspirational redemption bets – destinations like Nuuk, Greenland; Bilbao, Spain; and Faro and Madeira, Portugal.

- Meanwhile American has been hurt (their card spend volume has dropped from first to third) because of weakenss in high spend markets. They’ve pulled back in Los Angeles, New York and Chicago. In fact, they retired too many planes during the pandemic and lacked the aircraft to build Chicago back up, and are now slated to lose O’Hare gates. Retiring widebodies and focusing on short haul flying and the Sun Belt, they’ve lost some of the drivers of aspirational points acquisition.

Travel is aspirational. Airlines have premium customers, who are the ones with high volume credit card spending that’s been driving all of the growth for issuers. Card companies want to incentivize spend across their networks and using airlines as the marketing vehicle works. That’s what makes the programs so valuable.

Of course, this value is contingent on programs that consumers still value (for some reason that even includes SkyMiles) and on the underlying of economics of interchange remaining in place. If it’s regulated down, or competed down by new technologies, that’s a huge risk area.

All these values are based on flyers wanting frequent flyer miles. I now sort of want them but don’t feel bad if I fly basic economy and don’t get any miles or few miles. The choice of basic economy is not on price alone but a personalized algorithm that only I know the key.

Airlines are going after the class of people that can afford to fly multiple times a year and/or have the financial ability to purchase economy plus or premium class. This used to be the domain of business travel but business travel has been permanently altered by the use of Teams, Zoom, Google Meet and other project management tools. Even when doing business online yields a horrible result. I live this every workday of my life.

These same individuals are fertile ground for co-branded credit card sign ups. That’s the new frontier and why ULCC such as Frontier have a dark future because they will struggle to get that cadre of flyers. They will get the $49 fare customer and unless the ULCC can sell enough in ancillary service it’s just endless cash burn.

The accounting treatment of miles has always struck me as phony. More phony than normal business accounting.

I’m highly disappointed that Tim has not piped in to whine that the analysis understates the magnificence of Delta.

100% Gary. Airlines have become credit cards/banks with wings. And these companies are playing games with accounting tricks, pretending they have no money to pay workers, dividends, etc., but then, these separate loyalty programs are flush with cash to pay top-level executives, huh…

the data speaks for itself.

The takeaway is how much the airline detracts from the total value of the enterprise at AA. the market cap of most publicly traded airlines is higher than the value of their loyalty program – Gary’s analysis is correct

The value of the programs is an “enterprise value”. If you are comparing that to the value of the airline’s publicly traded stock that is apples and oranges. You would need to include the fair value of their debt too,

As Paul said. The correct comparison is an estimate of enterprise value (which does not change due to daily fluctuations of the stock market) of AA vs the enterprise value of the AA credit card program. Market value (via stock market value) plus Debt including airplane leasing might be a rough estimate of enterprise value.

AA revenue is being helped by anyone with a brain redeeming AS miles for AA flites. This tasty goose is likely to be cooked before the 2027 summer season.

Topically unrelated but both B6 and NK need to be carved up and sold to multiple buyers. AA needs to overpay for the assets of one or both to have any shot of future success as they cannot organically grow with their hi costs and debt load. While the latter would increase with a future purchase(s), per unit cost savings would help profits NOW and buy them some sweet stock market love.

The doubling of jet fuel prices disproportionately hurts smaller airlines. The smell of consolidation is moving from a simmer to a boil…

The valuation disconnect reflects that airline loyalty programs aren’t just more profitable, they’re fundamentally different assets. While airlines are capital-intensive, cyclical transportation businesses exposed to fuel, labor, and geopolitical risks, loyalty programs are asset-light, high-margin distributors of a quasi-currency with predictable, contracted revenue streams from banks.

The critical insight is that these aren’t separable businesses. The airline serves as the redemption backstop giving the currency credibility. As programs shift earnings toward credit card spend and away from flying, they boost short-term cash but risk long-term engagement elasticity when finite seat inventory becomes increasingly monetized.

The strategic question isn’t whether loyalty programs are worth more, but whether management should optimize them as integrated balance sheets. Rather than maximizing short-term annuity value from mile sales, carriers could treat programs as regulated financial products with explicit capital allocation, essentially running banks with airlines attached. That’s where the next valuation breakthrough (and the biggest strategic risk) lies.

They need to be very careful with devaluing points, whether by raising the redemption amounts or limiting availability. There are too many good cash back cards paying 2% (and sometimes more), that it could be very impactful to airlines financial performance if momentum shifts away from co-branded airline cards. Anecdotally, in the past two years I’ve dropped my AA and SWA cards and will jettison UA next year, just not enough value in them to justify paying annual fees or using in lieu of the real cash earnings on a % cash-back card which I can then use to buy tickets or upgrades at my leisure.

@Tom M – That argument only works if you redeem miles poorly. A 2% cash-back card is capped at 2 cents per dollar, full stop. But premium cabin awards routinely break that ceiling by a wide margin. For example, AA business-class awards to Europe can price at 57,500 miles one way, while comparable cash fares often run $3,000+ round trip, and sometimes far higher depending on route and timing. Even using conservative math, that yields roughly 2.5 to 3 cents per mile in real value after taxes, meaning a 1x earning rate already beats 2% cash back, and a 2x category effectively delivers 5%+ return. The same dynamic shows up across programs like Flying Blue, where ~60,000-mile business awards regularly replace tickets costing several thousand dollars. The real value comes from arbitrage. Airlines price premium cabins at levels most people would never pay in cash, yet still release award seats at fixed mileage rates that imply far higher returns than any flat cash-back card can deliver. Cash back is a fixed floor, while premium award redemptions are a variable ceiling, and that ceiling still materially outperforms. YMMV.

115K AA miles can you give an A380 Apartment on Etihad that may cost $7000. It’s a screaming bargain.

Delta Skypesos will charge 500K for a seat that VS or AF/KLM price much lower. Its enough to make anyone other than Tim Dunn scream.

the only people that are screaming are those that are incapable of finding bargains on DL and Skyteam.

They exist but some people are so preoccupied w/ the internet that they can never find them.

Note one more time, though, which airline program is the highest valued in the world.

Apparently giving away billions of dollars in inventory on the cheap is not the best way after all

Nice analysis Gary.

Does Tim have a job?

Tim

I have seen bargains on Delta, at times certainly.

For instance, a mere 200 or so points to fly via Moscow in the winter on Aeroflot.

These days the bargain is 500K points to fly via Saudia in the summer.

Now, when Delta opens a new route, such as SLC to Seoul recently, they are sometimes tolerable, such as a mere 200K points to fly to Seoul. But one cannot wait for Delta to add to its pathetic international network to get a non laughable deal.

SKyTeam certainly gives you deals — but Delta charges 495K for the same seats VS and AF/KLM sell for 1/4th to 1/5th.

Delta is great for mathematically challenged fanbots and fanboys

I meant Delta used to charge 200k Points to fly via moscow on Aeroflot (when it was allowed). And that too in the winter. A screaming bargain.

@Principal Lewis: From your analysis it appears you are the first generation of your family to win a scholarship to Special Ed.

This was such an eye-opening read — I had no idea that airline loyalty programs like AAdvantage could be valued at multiples of the airline itself, it really makes you rethink how much these programs drive airline revenue and customer behavior these days, and it honestly feels like credit cards with wings more than just rewards for flying; I’m curious though, do frequent flyers actually feel like they’re getting real value from these programs anymore, or is it mostly a way for airlines to lock people into spending? Also, while browsing other topics about how companies build long-term customer trust and value, I came across this interesting resource-https://qualityrenovation.com that made me think about how much strategic planning goes into loyalty and reputation in completely different industries too.