I receive compensation for content and many links on this blog. Be aware that websites may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Citibank is an advertising partner of this site, as is American Express, Chase, and Capital One. Any opinions expressed in this post are my own, and have not been reviewed, approved, or endorsed by my advertising partners. I do not write about all credit cards that are available -- instead focusing on miles, points, and cash back (and currencies that can be converted into the same). Terms apply to the offers and benefits listed on this page.

Bilt CEO Ankur Jain published his annual letter for 2026. It’s well worth a read, because it gives a roadmap for where the company is headed and drops some interesting statistics along the way. For instance, Bilt expects to process over $100 billion in housing payments in 2026. That’s about 5% of the market, and they’ve only just started mortgage. They report “1 in 4 U.S. rental buildings now in the Bilt network.”

And I think we can back of the envelope how many people have Bilt credit cards, too.

- They’ve reported over 5 million members and said that 15% had cobrand credit cards. That’s about 750,000 cardmembers.

- Then they say that “83% of the original active cardholders requested a 2.0 card, while housing spend stayed consistent month over month (with a slight drop in rent made up for with the addition of mortgage). ”

- We don’t know what an active cardmember is in this context. But this could mean there’s about half a million Bilt cardmembers today.

- And Bilt says 30% are annual fee cardmembers (the Obsidian and Palladium cards) – that’s 150,000.

Just 11% of cards linked in a Bilt wallet are their cobrands (of course, people with the cobrand are likely to link other cards, too). Linked cards break down as 56% Visa, 32% Mastercard, 9% Amex and 3% ‘other’.

And they’re seeing 2.1 times the non-housing spend with their new card compared to the old Wells Fargo one, even with fewer cardmembers. That makes sense – the old card was great for earning Bilt Points on rent, but was only o.k. for other spending. They have new cards that are top of market in their category for actually earning rewards for ongoing spend.

- Bilt Blue Card (See rates and fees) has a $0 annual fee, and earns 1X points on everyday spend.

If you’re maximizing the value proposition of spending alongside housing payments, then the card allows you to earn 2.3 transferable points per dollar on your spending. And these are the most valuable points you can earn. That’s top of market for a non-Bilt catch-all card, and clearly top of market for a no annual fee card.

- Bilt Obsidian Card (See rates and fees) has a $95 annual fee and earns 3X points on your choice of grocery (up to $25K/year) or dining (your 3X category choice remains in effect for the entire calendar year), and 2X points on travel.

If you’re maximizing the value proposition of spending alongside housing payments, it can earn 4.3 points per dollar on grocery or dining.

- Bilt Palladium Card (See rates and fees) has a $495 annual fee and earns 2X points on everyday.

If you’re maximizing the value proposition of spending alongside housing payments, it can earn 3.3 points per dollar on most of your spending. I’ve ever written how to turn this into a 4x on everything card.

Now that their cards actually reward ongoing spend, and not just buying ‘five bananas’ each month to unlock points-earning for rent, Bilt says members are now engaging beyond housing, with monthly card spend “at Bilt’s neighborhood partners” growing in dining (20%), rideshare (22%), fitness (47%), and travel (320%). The new card uses merchant-funded offers through Bilt Cash to drive greater engagement.

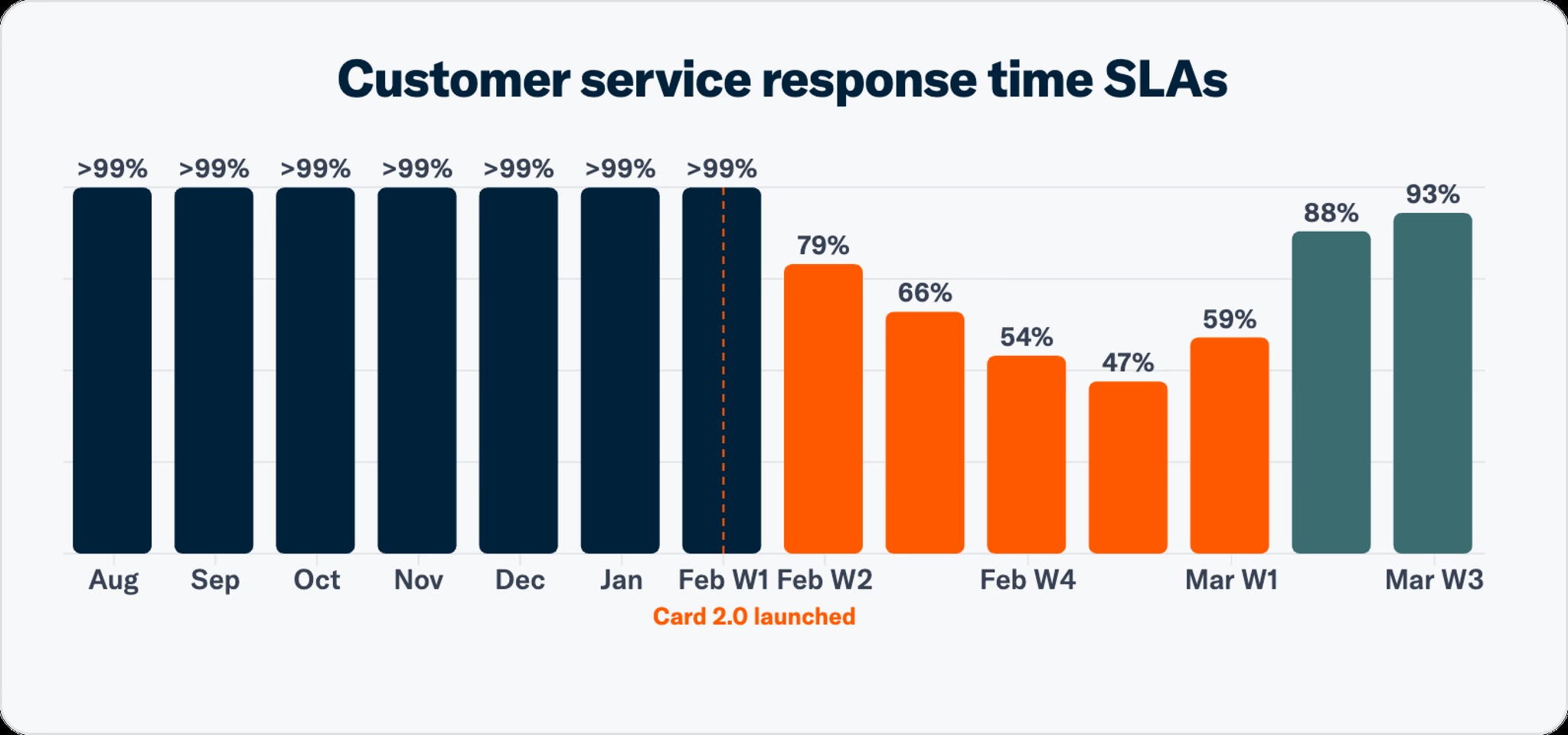

Notably, though, they acknowledge their “support experience” lagged and “response times went up” after the new card product launched, though they suggest they’re close to reverting to goal now (they don’t define what that is).

Credit: Bilt

But what’s the real takeaway? It turns out it isn’t about the card at all. The letter is formally telling you the card is not the core product. Instead, it’s a housing-linked membership, payments, and merchant network.

Bilt is tying together four businesses at once: property-manager software/payments and leasing; resident loyalty; merchant customer acquisition and checkout; and a smaller premium card business.

Its real-estate materials pitch on-time payments, maintenance and amenities management, leasing incentives, higher renewals, lower delinquency, and “new revenue through neighborhood spend.” That’s been a part of the core pitch to landlords from the beginning, and why they brought several big ones on as investors and so many buildings have partnered with them.

Bilt offers property owners resident-engagement and payments. Their materials pitch more digital payments, lower delinquency, earlier renewals, lower leasing-incentive cost, and passive revenue from neighborhood spend. They claim +300% early payments, +20% early renewals, 4 weeks faster decision timelines, -12% delinquency, and +30% digital payments. Bilt doesn’t disclose pricing deals for this, so the revenue logic gets featured but we don’t know the unit economics.

Meanwhile, merchants pay Bilt commission for access to its members who spend. That’s Walgreens, Lyft, restaurants, GoPuff, and parking garages. That’s why they reward you for spend with their partners whether its on a Bilt card or not. And they’re pushing into seamless checkout experiences broadly.

Bilt pitches a modern checkout flow with digital receipts, personalized offers delivered during checkout, and automatically triggered perks like complimentary items or rides. They’re doing customer acquisition, loyalty, checkout, and upsell in a box for small and larger businesses alike.

- What originally interested me in Bilt is that they solved the distribution problem figuring out how to reach high value customers in a way that no one else had done it before. I wrote in 2021 that they were going to be a very big deal because they had customers everyone wanted – in their homes, through their housing payments, in a very sticky way.

- They could then incentivize these customers to do business with their partners, and that would be a lucrative business. Bilt has customer acquisition at move-in, precisely when their habits reset.

- And Bilt sitting in the middle of $100 billion in housing payments is itself a valuable business. Then merchants pay commissions on spent. Property owners get retention and operating efficiency. And there’s a credit card, too.

Bilt can offer better points than competitors, with bigger transfer bonuses, and elite status opportunities occasionally (they’ve done it with United, Hyatt, Air France, Accor) because their partners value the customers they have specifically. Bilt doesn’t just come buying points, they bring affluent young urban professionals with a lifetime of earning and buying ahead of them.

And the addition of Bilt Cash is a bigger deal than most people realize, I think. It isn’t just earned on their credit card, but from points-earning across their partners, too. It’s redeemed on partners through merchant-funded offers, so it’s cost-effective. And it additional spending to partners where Bilt earns commission. In most cases redemptions cost them less than they’re earning from the partner, which is a way of saying that the partners are paying Bilt to generate more commission. And the ability to move the needle with their desirable customers makes them even more attractive to their next partner (and that next partner grows their ecosystem, making the value of their network grow a the same time).

The letter is mostly a narrative consolidation of prior product launches, but brings them together in a broader story that I think is helpful for understanding their actual business (or at least their vision for what the business becomes).

Also interesting in the letter is the discussion of their new AI concierge, which they say members are using across rewards, housing, dining, travel, and fitness. There’s no hard data on volume, transaction completion, or errors. So it’s just a description of potential where they take a customer basis and offer them agentic transaction capability. Now they have to figure out how to make it useful enough for members to drive real transactions at scale.

If you are not looking for another credit card, Bilt is still pretty interesting: link your existing cards, take the stacked local rewards, use the neighborhood benefits, and use your existing rewards cards. That’s how Bilt describes most of their members.

If you liked old Bilt because it was a simple rent points arbitrage, that product is gone. There’s no more floating your rent (and maybe earning on a high yield savings account in the meantime), either.

Where they need to start nailing things quickly is on execution and customer service. Jain’s letter uses the word “trust” six times. They recogize that for this to work, members need to trust them with their homes. It also means execution risk matters to many members even more than rewards. A missing Walgreens credit is annoying. A missing mortgage payment is a real problem.

But what a lot of people negative about Bilt miss is that there’s a real business model here, it’s just not what they thought it was. If there’s a real criticism, it’s that Bilt is trying to run too many businesses too quickly all at once. That’s how they win, but it’s also how they can fail if they don’t execute well enough across the board. They’re managing rental property workflows, housing payments, a card program, merchant checkout, rewards accounting, and AI support to name just a few things and each of these systems requires trust which requires executing well and providing quality customer service too.

I’m finding that there’s no richer program out there now, but I am watchful over my mortgage payment to make sure it completes (it has) and I recognize that it’s more complicated with accumulating a proprietary currency alongside points that rations benefits across a diverse array of partners – each offer with its own terms and deadlines (and only $100 of Bilt Cash carrying over to the next year).

That’s a real sweet spot for extracting outsized value from a program, but it requires paying attention and staying engaged – which is also the exact kind of behavior that Bilt is looking for. Members who lean into what they’re offering can generate a lot of value, if only by earning status in the program and using ever-increasing transfer bonuses at each level. I just moved a few hundred thousand Bilt points over to Japan Airlines Mileage Bank on March 1 with a 125% bonus. Where else can you do that? And especially when I’m earning those points at a faster rate than I would on any other credit card by spending with my Bilt Palladium Card.

The reason that Bilt raised money at over a $10 billion valuation last summer (and I don’t know what terms or liquidation preference goes into that number, but it’s still impressive) is that they’ve done something novel and significant in using housing relationships as a distribution platform. They’ve acquired customers in a really unique way. They’re high value customers. And they’ve developed a model to monetize and reward those customers richly at the same time.

And they have a vision to continue doing that in deeper ways. Their hospitality platform – that helps restaurants earn loyalty by delivering better experiences to members! – at least has the endorsement of real top chefs and restauranteurs whom I genuinely respect. I haven’t seen it in action, so I can’t evaluate it, but check out who’s on board – Will Guidara! Thomas Keller! Danny Meyer! Daniel Boulud Michael Mina!

Introducing Bilt Hospitality for Restaurants.

Bilt's newly launched hospitality platform is a fully managed concierge service that unifies the guest experience before, during, and after every visit. We're proud to have some of the greatest names in food and hospitality with us. pic.twitter.com/TuGVPx6dxr— Bilt (@BiltRewards) March 22, 2026

I don’t know how much revenue comes from property operators, merchants, card economics, housing payment fees and float, or travel commissions. The business model exists but I don’t know what the math looks like, what the margins are in each business segment, what their rewards P&L is like, or how much of the Bilt Cash redemptions they’re actually funding or how important breakage is in the model (I really think their expiration policies are a mistake, since they’ll be a disincentive to spend on the card or transact in significant ways towards the end of a year).

But I do know that this is one of the most ambitious projects we’ve seen in loyalty marketing since the original launch of American AAdvantage in 1981 – and people forget that American initially only rolled that program out as a test.

For the love of all that is Holy and good in the world. Stop promoting BILT!!!! It’s not sustainable, is confusing, will likely have several class actions against them, for violating FTC rules, has caused hundreds of customers mortgage payments to be late and does a disservice to your readers. The incessant posting about BILT has become annoying

Excellent analysis.

This has potential and I’m sure looked good on a pitch deck as a disruptor. Not surprised they raised the cash. But as you and they note, the trust isn’t there yet after a botched roll out. All this agentic AI stuff sounds great – AI will seamlessly get me a restaurant reservation, a cab, blah blah – until you try and interact with Bilt’s not great AI customer support.

My guess is that their customer base comes from renters with large landlords in urban areas. Not a bad customer base to start with, the question is if that base will stay with Bilt as they age versus “graduating” to Amex, Chase etc. Don’t know enough to answer that question yet.

Is this a valuable points earning and transferring card? Sure, once we trust it enough. Appreciate the data points but I’m still waiting a few months before considering anything with Bilt and mortgage payments. No need to pay to participate in the beta test.

Gary, I’m not gonna ‘yuck’ anyone’s ‘yum’ on here, but… how much do BILT ‘fluffers’ getting paid these days? Bah…

Built came on board with no-fee rent/maintenance payments.

That is no longer true, so why keep them?

I love Bilt and am very happy with the Obsidian.

However, please, if you have one with Autopay on, please check. I noticed that a few days after the date it should have posted (but before the late date) that it hadn’t posted, so I call to ask.

The nice man on the phone looked into it, then went away for a long time to ask a supervisor, then came back to tell me that at least for this first month I should turn Autopay off and make a one-time payment. (So I did.)

Could have been my fault, or it could be teething issues; but please check if you have Autopay … and hate late fees.

Gary – glad to see you’ve pivoted from endlessly hyping the credit card after the initial sign up push to now pushing the narrative that the credit card is a minor aspect of a broader business.

The company has positioned itself to consumers as a credit card company, not a do all neighborhood ecosystem. Go ask the people in the demo Bilt supposedly has a grip on about the company – you will get blank stares. Let’s not pretend that the ecosystem is valuable and something consumers care to engage with actively.

If the setup of the biz is so genius and Bilt has captured the valuable demographic, why did the Wells Fargo deal go bust so fast? Wells aim was to capture customers in the young demographic. So if Bilt has these customers, what gives?

This company has been a solid points play for sure, but pretending it is a disrupter is intellectually dishonest. Bilt has lived on PE money and the current model isn’t sustainable.

Keep the charade going as you wash away your credibility

@Desperado – “If the setup of the biz is so genius and Bilt has captured the valuable demographic, why did the Wells Fargo deal go bust so fast?”

(1) the deal made sense for wells when they were investing in a cobrand business, they made unprofitable deals with expedia and choice also but this one turned out to be bigger – that was intentional strategy as they were positioning themselves for bigger plays like bidding on major airline business. if they’d continued down that path the losses here wouldn’t have mattered. they went in knowing they were overpaying, they weren’t unsophisticated. (2) wells pivoted, the losses no longer made sense, and they were losses because wells was paying for the points but not earning interchange on rent, people don’t really revolve rent, and with the 1.0 card people weren’t spending that much outside of rent.

but it makes no sense to say ‘bilt isn’t bigger than the credit card because the economics of the credit card didn’t work for their previous issuer’ – do you see the lack of logic there?

The only lack of logic I see is you stating Wells “knew they were overpaying” while also stating “they weren’t unsophisticated”..

Sophisticated businesses don’t knowingly overpay.