Airlines are a terrible business. The old joke is that the fastest way to become a millionaire is to… start off a billionaire and invest in airline. Warren Buffett once said that “If a far-sighted capitalist had been present at Kitty Hawk, he would have done his successors a huge favor by shooting Orville down.”

While I think that JetBlue should have been allowed to buy Spirit Airlines, I also was clear at the time that it’s almost never a productive use of capital to spend it investing in an airline.

- The acquisition of Spirit was set to cost about $3.8 billion. The S&P 500 is up more than 75% since the deal was agreed to.

- I suggested just investing the money in broad-bsaed stockets. $3.8 billion would be worth $6.56 billion today.

- Instead, JetBlue’s market cap has fallen and is just $2.1 billion.

The basic reason why airlines are so tough is because they’re an expensive capital intensive business, they’re heavily unionized, and outside of a few congested airports there are no moats. If you find a profitable route, another airline can move a plane in to compete on it. Airplanes will literally fly to wherever there’s an opportunity

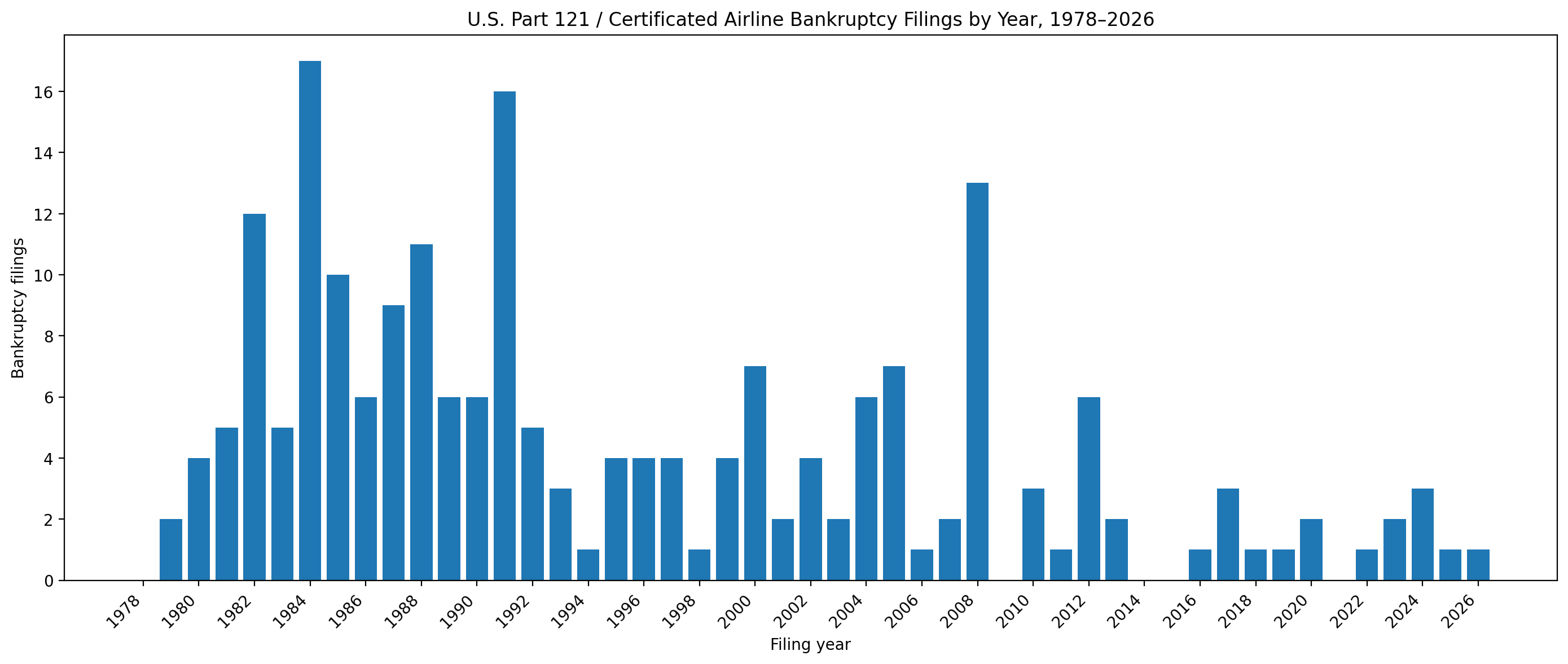

David Oks argues that airlines are doomed to chronic financial instability because they are an “empty core” industry with no stable competitive equilibrium where carriers can all earn adequate returns.

- Airlines have high fixed costs, volatile demand, relatively low marginal costs once a flight is operating, and limited product differentiation.

- If a market can support three-and-a-half daily flights, then three flights leaves money on the table and invites entry. But four flights creates too much capacity, fares fall, and somebody loses money. Eventually someone exits, fares recover, profits return, and then another carrier is tempted back in.

That’s why he says airlines are always going bankrupt.

Competition keeps creating excess capacity, excess capacity destroys fares, and bankruptcy resets costs. And he says airlines survive by avoiding competition.

- Pre-1978, the Civil Aeronautics Board told airlines where they could fly and what prices to charge. They were set at a high enough level to be profitable.

- Airline strategies now are fortress hubs, joint ventures, alliances, loyalty programs, and credit card deals.

This doesn’t quite work. Capacity is lumpy, but the idea that “three flights is too few, four flights is too many” misses because airlines don’t add identical flights. They choose what planes to use on a route. They can add a fourth flight with fewer seats, and even reduce the number of seats on their existing flights too.

Airline capacity is sticky, constrained, and only partially adjustable. A smaller aircraft may fit demand better, but usually has worse unit economics so may not work economically. And the right aircraft may not be available. A flight is also part of a network, with both local traffic and connections. And a flight may appear to lose money flying empty, but be key to a broader deal that’s profitable.

There’s increasingly differentiation between airline products. That wasn’t always true. As recently as the American Airlines 2017 Investor Day, their then-CEO offered that there was no real advantage to be found in better seats because other airlines would match that. But different airlines:

- Have different cultures – Southwest Airlines crew seem to enjoy their jobs more than peers, Delta’s have been marginally friendlier though arguably less so with turnover since the pandemic.

- Have different product philosophies – American ditched seatback entertainment screens starting in 2017, while United subsequently leaned into them.

- Offer different schedules, with non-stops hardly the same as connections.

- Have frequent flyer programs with varying generosity and different paths towards elevated status.

It’s not the case that the industry is profitable or competitive but not both – Delta and United represented nearly all the industry’s profits in 2025.

You’d expect flying to look profitable where it’s protected, such as at slot-controlled airports, but New York JFK, LaGuardia and Washington’s National airport aren’t as profitable on their own as you’d expect. They do dovetail well with high spend consumers feeding lucrative cobrand cards.

But loyalty programs don’t mean, as the piece suggests, that airlines have exited the airline business. On the contrary,

- The programs began as a way to create a differentiated product rather than a commoditized one, generating brand preference and loyalty.

- No one would collect the miles without the flights.

- And the card programs create more flying opportunities. Airlines are willing to offer more flights at lower fars to capture a market’s relevance for the cobrand. Southwest began flying to Hawaii, in part, to give credit card customers a reason to save their points. Delta told investors during their third quarter 2025 earnings call that they were leaning into the Austin market because it was fertile for acquiring cobrand American Express card customers.

The programs are high margin – more so than seat fees and checked bags. But the classic way to attract outsized cardmember spend (and therefore program revenue) is to offer aspirational experiences that a member wouldn’t buy for themselves – premium cabins, long haul, partner airlines. JetBlue would have benefited in its American Airlines tie-up because it was going to join oneworld.

Startup airlines face much greater challenges in loyalty because they lack scale. They can’t be relevant to all of a customer’s flying. A low cost carrier will have a hard time matching without premium experiences to offer. It’s crucial to lean into status experiences to compensate – Frontier does a very good job of working with the assets that they have. Spirit had crafted something of a ‘me-too but less than’ copycat approach. Neither could hit above their weight like Air Canada does with Chase in the U.S. (or Hyatt with Chase).

Ultimately, this is a tough industry because route and capacity decisions are made in large, operationally constrained chunks in an industry where demand is volatile, inventory is perishable, prices are transparent, and competitors can quickly destroy revenue.

That’s why product differentiation – through the overall experience and loyalty program and cobrand offerings – is the clearest path to long-term viability. Contra the American Airlines 2014 – 2024 view, competing primarily with Frontier and Spirit was never going to be a path to profit (especially for an airline with high costs itself, that needs to generate a revenue premium just to cover them).

Even the best-run, differentiated airlines are still exposed to the same structural challenges. United’s Scott Kirby claims airlines just need to raise fares, demand is inelastic, and they fail to do this because government relations and marketing wrongfully conclude it’s too risky a strategy.

However raising fares invites market entry. It signals above-normal profits, and competitors can just hold price (or even lower it) to capture business.

And if they are too capacity-disciplined, they lose network relevance like United did under Jeff Smisek, focusing on international and gutting domestic (this was one of the early changes Kirby implemented).

Deregulation ended an artificial moat that airlines had, protecting them from each other. That’s been great for consumers because of lower fares and more flight options. And it’s forced airlines to try to de-commoditize. But it’s been brutal for airlines, who have had to go in search of other moats.

Excellent analysis, Gary. You’ve correctly identified that the airline industry’s chronic instability stems from a fundamental structural mismatch between supply and demand characteristics. What’s particularly telling is how this creates a bifurcated competitive landscape where legacy carriers with established loyalty ecosystems can cross-subsidize unprofitable routes through their financial services revenue, while new entrants face a classic chicken-and-egg problem: they need scale to build a competitive loyalty program, but need a competitive loyalty program to achieve scale. This creates natural barriers to entry that are more durable than the route-based competition you described.

The critical insight isn’t that airlines are bad businesses, but that the transportation component alone is structurally challenged. The most successful airlines of the next decade won’t be those that operate planes most efficiently, but those that best leverage their customer relationships across the travel value chain. We’re already seeing this with Delta’s stake in LATAM and United’s expansion into MileagePlus businesses beyond flights. The airline industry’s best path forward may be less about transportation and more about becoming vertically integrated travel platforms with transportation as just one component of a broader ecosystem.

Airlines want the best of customers and to do that they need to have a robust schedule. Typically, a business flyer or a high end leisure flyer doesn’t want to spend an entire day going from Boston to Austin. But maintaining robust schedules will mean excess seats.

If you’re airline management you’d far rather fill that empty seat with a money losing fare than nothing at all. Hence, the birth of the BE fare. In theory those seats aren’t about generating profit but generating additional revenue.

That leads to excess capacity which leads to losses. It’s been that way since the 1980s and an after effect of deregulation.

The way around this? Bring back the CAB which will designate routes, pricing, projected profit margins and award routes to airlines. But you’d get CAB style fares which means far fewer people could afford to fly.

So far airline management hasn’t been able to create a stable industry. The temptation to add capacity is just too great.

I think your article from yesterday on antitrust had a lot of good points. I think your article from earlier today about B6 not going bankrupt this year is also accurate. And yet, here we have the elephant in the room and the real barrier to meaningful competition and entry to competition – the credit card programs.

I’m certainly no Dave Ramsey acolyte, but the dangers of credit cards for the average consumer are quite real. That said, in general, spend on airline cobrand cards tends to produce much better quality receivables than spend on non-cobrand cards. For instance, there are specific disclosures in Citi’s credit card securitization trust SEC filings about the adverse impact of removing the AAdvantage cobrand cards from the securitization trust – the tables are interesting to read. Because it tends to be higher quality credit, I have less of a strong feeling about those cobrand cards subsidizing the major airlines (in a way, for these purposes, the cobrand consumers are accredited investors).

Might you see an AA bankruptcy again someday? It’s possible. But is AA going anywhere? Of course not. There’s too much gravy to go around using AA as a cash flow producing vehicle (even if it’s not producing “profit” as shareholders or employees would think of it).

That said, how are any of the remaining LCCs ever really going to be able to “break through” and compete with the majors without a meaningful credit card program? Even if they could have one, it’s going to be smaller in scale, and likely targeting a lower income demographic. Someone like B6 might have a chance on paper given where they have hubs, but even then, their new credit card and one “bluehouse lounge” in a terminal that no one wants to spend any time in because it’s gross is likely far too little too late – sure B6 may limp along in perpetuity, but its growth is definitely capped as well.

Where the role of government is in all of this heavily regulated industry, I have no idea, and I’m sure this comment section is smarter than I am. I don’t think either political party has done very well as of late in the aviation sector though.

Gary, airlines go bankrupt because of micro and macro economic mismanagement… Whether it’s 2008 or today, it’s a combination of failed corporate and political leadership. The outliers are 2001 and the pandemic, which were deserving of bailouts in this and other industries, but targeted, and with stipulations to balance the scales between capital, labor, and consumers. Instead, many of these bozos privatized years of record profits through buybacks while socializing their losses through bailouts. If airlines focused on operational redundancy and fair pricing instead of financial engineering and credit card schemes, they wouldn’t need a taxpayer-funded safety net every time the economy weakens (or a Republican starts a new war in the Middle East rising energy costs.)

@Peter — From a consumer experience side, on the ground level, you’re 100%. There’s clearly an oligopoly forming with the Big-3. We can compare DL vs. F9 or WN seats all day, but, the reality is that all US-based carriers have become increasingly hostile to the average traveler (including ‘elites’ who rarely get complimentary upgrades anymore; devaluations to frequent flyer programs and redemptions, like Delta’s SkyPesos; and, of course, less MCE, when there should be more…)

Also, I donno about anyone else, but I can’t wait for @Tim Dunn’s ‘white paper’ on RASM/CASM and load factor… (that is, of course, if he doesn’t get distracted by Gary’s jabs… “Have different cultures – Southwest Airlines crew seem to enjoy their jobs more than peers, Delta’s have been marginally friendlier though arguably less so with turnover since the pandemic.”) Less so?! WHAT?? Never!! Not our beloved Delta Air Lines! Bah…

There is no passenger transportation system in the world that really makes money. When I managed a train for Amtrak, I heard the same thing – “our trains are full, how can we be losing money?” All passenger transportation modes are both labor and capital intensive – so when you lose money on each passenger, more passengers equal losing money faster.

@1990- You used to get something complimentary for the flying. Then it changed to complimentary for direct spending. Now it’s becoming more of a theoretical complimentary with the possibility of complimentary enhanced by having a credit card. “But you’re saying there’s a chance…” says an average American.

So the consumers continue to get squeezed (just ask a SW flyer how they feel about finally being monetized). Ironically this is where being a free agent shines. Many would be better off with want first buy first frames of mind versus a hamster wheel.

And, further ironically, the lack of a competitive balance between Citi Strata Elite versus AA cards is helpful to AA. I would think that Chase can take a harder line with United because it has the CSR/CSP to bulk up its credit card securitization program.

So if Mike H is correct about the way he framed the barrier to entry (reasonable enough) how does government protect the consumer against vertically integrated travel platforms, if indeed that should be a role for government to play in an industry that is already heavily regulated?

Folks are taking big bets on this stuff (look no further than Amex GBT being bought this week for over $6bb in a big bet on AI travel). I for one think that travel economics in 2040 may be radically different than today’s basic economy versus main cabin squabbles.

@Peter — Bah! “So you’re telling me there’s a chance”… Classic… Lloyd Christmas (Jim Carrey).

Yup, the ‘credit cards with wings’ financialization of this (and other) industries is the name of the game these days. You’re right that, unless everyone balks on the CSR, United needs Chase more than Chase needs United; whereas, American has Citi by the… let’s say… nuts.com (I saw you at LALF recently).

The Long Lake Management deal is concerning. Those AI agents won’t just shoehorn us into preferred options; they’ll likely use our own spending data to determine the maximum price we’re willing to pay in real-time. And, when we don’t comply… they’ll scour our email for blackmail! …yikes.

Governments can protect consumers (EU, CA, and a few others may try), but this current government in the US won’t. I’d start with price transparency (show the full cost; enough junk fees; include less expensive, not just the preferred options), continue with actually regulating the corporate pseudo-currencies to prevent random devaluations without adequate notice, and, ultimately, anti-trust on the tech.

Yes, individually, gonna be more free-agents, less loyal customers, closing some of these co-branded cards, and weathering the storm. It’s been fun while it lasted.

Yet all the complaining and 90% of domestic fares LOSE money for the airlines. @1990 Name me one line of business in which 90% of sales lose money for the enterprise. I’m waiting.

Yes, we could go back to the days of regulations and the CAB. Back then almost every fare had to have a positive ROI. Meaning take the revenue from the fare, strip out taxes, airport fees, direct costs such as crew and ground labor and fuel, and indirect costs such as corporate marketing and finance overhead and the resulting number must be positive. Want to guess what would happen to fares?

I’d personally be very happy with that arrangement. I’m sure so would airline executives.

none of the comments are wrong but the reality is that the US airline industry is still very competitive and there is little incentive NOT to add a bit more capacity in hopes of getting a bit more revenue while pushing down unit costs just a bit more.

and, yes, the US industry is very close to losing overall competitive traits which is all the more why talk about consolidation involving the big 4 – even asset transfers – should raise all kinds of red flags.

Kirby, to no surprise, pushes the narrative even further talking about wanting to take out competitors and how every other business model except his doesn’t work but he also realizes that UA simply made some bad strategic decisions over the past 20 years that are harming their ability to reach DL’s levels of profitability – so he wants to just eliminate the competition so he has a straight shot to higher profits.

and the bigger point to this article is that no US airlines were allowed to go bankrupt for much of this century because of government aid esp after 9/11 and covid. If you continue to support failing businesses, then the problem just keeps getting kicked down the road. The reality is that some airlines should have been allowed to fail over the past 25 years and the industry would be stronger now.

The government doesn’t care about a stronger industry, though. They only want to see lots of competition.

but let’s also be clear that there are airlines that are making decent profits by airline industry standards and are attracting capital – so the notion that all airlines are univestable and money-losing is just not reality.

@Mike Hunt:

As long as the costly & failed attempt to create a vertically integrated travel company (ultimately renamed Allegris) from 1979-87 offering flights, rental cars & hotels by United Airlines under then CEO, Richard J. Ferris, is kept in mind.

Gary, you fail to address the issue of stock buybacks which should be illegal. That money should be used to pay down debt and buy new planes and sign contracts when they become amenable, not years later damaging employ morale. That money could also help during the hard times of recession and inflation. I’d like to see a lengthy post about this issue.

@Joe United:

Hear, hear!

Lots of good econ here, but US airlines could differentiate themselves w/ good inflight and on ground customer service instead of taking the MBA view that the customer is my enemy.

@jack the ladd, @Joe United — PREACH!!

@George Nathan Romey — Easy. Retail banking (see ‘free’ checking accounts). Lots of loss-leaders in film, supermarkets, and other industries, too. C’mon, less strawmen on here, please.

@Tim Dunn — I knew this would either inspire a ‘Delta is best’ or a ‘United is worse’ retort. Bah!

Interesting that the DOJ has seldom opposed a merger of two bankrupt airlines (DAL+NWA) due to concerns over reduced capacity, competition and higher fares, only when a couple of money-losing second and third tier players attempt to join forces…

Capt

DL and NW were about as perfect of an end on end merger as any Us mergers has been; they had very little direct overlap except on hub to hub routes.

and neither DL nor NW was in chapter 11 when they proposed to or actually did merge.

1990,

my comment is a statement about execs trying to talk the competition out of existence; AA, WN and other carriers have not done it either – it is just UA’s current exec team that does it.

@Tim Dunn — “execs trying to talk the competition out of existence”… well, not just United execs, Tim… I mean, I think you’d take top-prize in that! *wink*

A lot of what makes the airlines volatile is that the passengers search for the lowest price tickets as one of their main parameters. After all, who wants to pay an extra $100 for essentially the same flight. This results in the airline companies racing to the bottom to create the cheapest coach seat possible for competition. A sure path toward bankruptcy that visits even companies that were making a lot of money only a few years ago. The companies cannot get off of the merry-go-round. Yes, companies make their profit off of the expensive seats, but only if most of the coach seats are filled.

I don’t lead any airline – or even work at one – and only “command” my keyboard.

but, perhaps you can post some of the smack talk that has come from AA, DL and WN – or just about any other airline except for UA – while entire encyclopedias could be written about the trash talking that UA execs have made about other airlines.

The sad thing – from an irony standpoint – is that the feds have done more to restrict UA’s growth in its own hubs because of excessive and aggressive growth that overwhelms airports and ATC while none of those other airlines have been singled out.

Maybe, just maybe other airlines can compete effectively in the marketplace and people esp. regulators really don’t want to hear large companies – esp. ones that love to tout their size – talking about their plans to become even larger at someone else’s expense.

Maybe if you take out the trash talking about B6 and salivating over their assets, they aren’t doing so bad after all, you think?

@Tim Dunn — Wait until @DesertGhost hears about this… he’s always asking, “And you’ve been CEO of how many airlines?” (As if that gatekeeping is necessary to have or share opinions on here or elsewhere.) You can confidently tell him that you haven’t. Progress!

@Joe United – stock buybacks should not be illegal, that is silly, so the share count of a public company should only ever be allowed to increase?

It never ceases to amaze me how most travelers pick the absolute lowest fare, even with more stops, worse times, crappier terms and tinier seats. I’ve never seen another product where this is so much the case. Then those people will spend the difference on drinks on the first night without blinking.

I remember back in the day when AA was the only airline with extra legroom in coach. I actually flew them intentionally then because of that. Didn’t last long.

Don’t the airport gates limit competition? Delta has 75% of the flights in/out of Atlanta and Detroit, and many at DFW. How are they not making money?

If the business is so capital intensive, how are these low cost, start up airlines, which won’t make it, continue to pop up?

If it is as bad as you write, and will never get better, we should go back to limited regulation to protect the airline executives from putting each other out of business.

I personally think the business is fine, its just the business model these short term leaders try to perpetuate to look good for the next 90 days to Wall Street.

Also, the real reason is that flying used to be special and wasn’t catering to joe sixpack, college kids, and families that in reality can’t afford to go to Florida or Cancun. Raise the prices!!!

David,

the FAA, thankfully, requires that US airports that are federally funded – which is nearly all of them – have to make gates available for new entrants – specifically so that the incumbent airlines can’t make it impossible to block the competition.

the real issue regarding startups is that labor costs are now so high that low cost and ultra low cost carriers cannot cover labor costs and the high cost of getting an airline started -including high aircraft costs.

People love to blame airlines but it is the whole aviation ecosystem that incudes the number of pilots and mechanics to the production capacity that Airbus and Boeing have not just for the US market but for the whole world.

Aviation has settled into an industry built on scarcity which makes it hard for smaller and lower revenue carriers to survive while startups face a very uphill battle

Nice analysis.

My JetBlue stock is suffering, looking for a jumping-off point. Meanwhile, my Spirit miles aren’t worth as much as they were a short time ago, sigh. I know better.

@DaninMCI — “Won’t somebody please think of the (shareholders)!” — Helen Lovejoy

Oh my gosh, the anti-stock-buyback lunacy reappears. If you know anything about the underlying logic, a stock buyback is just another (typically smarter) form of a dividend. When a firm pays me a dividend, it gets automatically reinvested. I go from owning X% of the company to the slightly higher Y% (more shares for me, same # outstanding). If the company spends the same amount in a buyback, I go from owning X% to the exact same Y% above (same # shares for me, less # shares outstanding). In a world without taxes the effect is identical. In a world with current US taxes, I pay $Z in taxes on the dividend or $Z on the gain when I sell it in the future. The delayed taxes makes me better off. How in the world should companies be allowed to issue a dividend that costs them $100 million but not buyback $100 million in their own stock?

@This comes to mind — Psh. The lunacy is allowing taxpayer funds to go towards corporate stock buybacks; the lunacy is not opposition to such buybacks. Classic example of socializing losses; and privatizing gains. Enough of this 2nd Gilded Age nonsense. Check yo self, Ohio.

During the last round of bailouts, the CARES Act, $50b to airlines, had no real ‘teeth’ or other enforcement, because it was mostly a ‘grant,’ not a loan… so, we relied on the good faith of these companies to retain their employees (not force retirements, but they did so anyway, basically), all so that when the pandemic was over, and demand roared back (inevitably), the airlines would be ready… Instead, they didn’t prepare for that, and just took all those billions to do the stock buybacks, which raised the stock prices, and made the C-Suite look great, leading to excessive executive compensation, while everyone else (workers, consumers, taxpayers) got a raw deal.

Gosh, this is very telling. JetBlue was willing to spend $3.8 billion then and have half that in cash (&equiv.) now.

@This comes to mind — Change it up a little… maybe throw in a ‘garsh’…